What is economic surplus? Definition and meaning

In mainstream economics, an Economic Surplus refers to two related quantities:

- Producer Surplus.

- Consumer Surplus.

Mainstream economics means orthodox economics, i.e., what most universities across the world teach and discuss.

Economic surplus is also known as Marshallian surplus, named after the British economist Alfred Marshall (1842-1924) who made the term widely known – economists also use ‘total welfare’ with the same meaning.

This concept highlights the importance of market efficiency, where resources are allocated in a way that maximizes the combined benefit to both producers and consumers.

When there is a significant increase in assets over the amount of liabilities a firm holds, it has an economic surplus. This article focuses on the term when it relates to producer and consumer surpluses.

According to My Accounting Course, economic surplus is the sum of the consumer surplus and the producer surplus in an economy.

“In other words, it’s the benefit obtained by suppliers for selling a good or a service at a higher market price than they would be willing to sell and the benefit obtained by consumers for paying a lower price for a good or service than the price they would be willing to pay.”

Economic surplus – 2 quantities

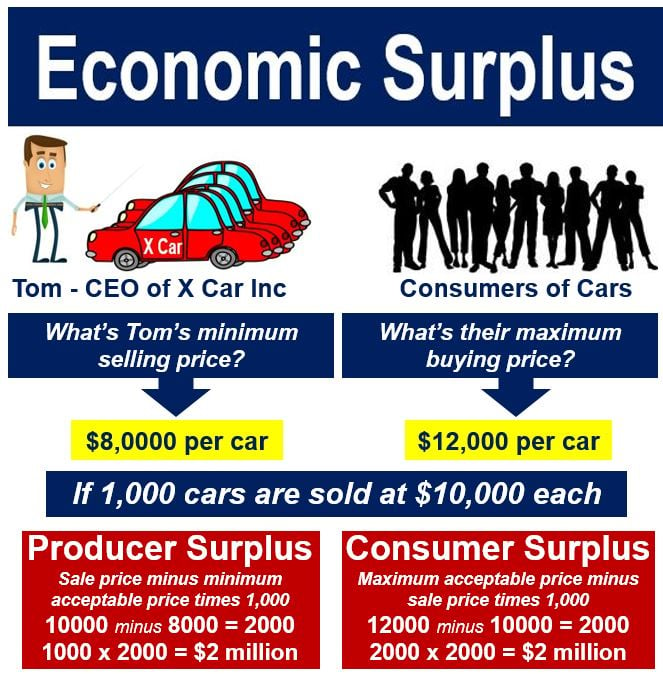

– Producer Surplus: this is the difference between how much a supplier sold something for and how cheaply he or she would have gone (minimum selling price). For example, if I sell 1,000 widgets for $10,000 ($10 each), but I would have gone as low as $6 each, my producer surplus is 10 minus 6 times 1,000 = $4,000.

– Consumer Surplus: this is similar to the one above, but from a consumer’s point of view. It is the difference between how much a consumer purchased an item for, and how high he would have gone – the top price he/she would have accepted.

Let’s use the same widgets example here for consumers – 1,000 of them were sold for $10,000, i.e. $10 each. Consumers would have accepted spending up to $13 for each item. Therefore, the consumer surplus is 13 minus 10 times 1,000 = $3,000.

Term emerged in 19th century

Arsène Jules Étienne Juvenel Dupuit (1804-1866), an Italian-born French civil engineer and economist, first proposed the concept of an economic surplus in the mid-19th century.

However, it was Alfred Marshall, one of the most influential economists of the late 19th and early 20th centuries, who brought the term to the forefront of mainstream economics in his 1890 book – Principles of Economics.

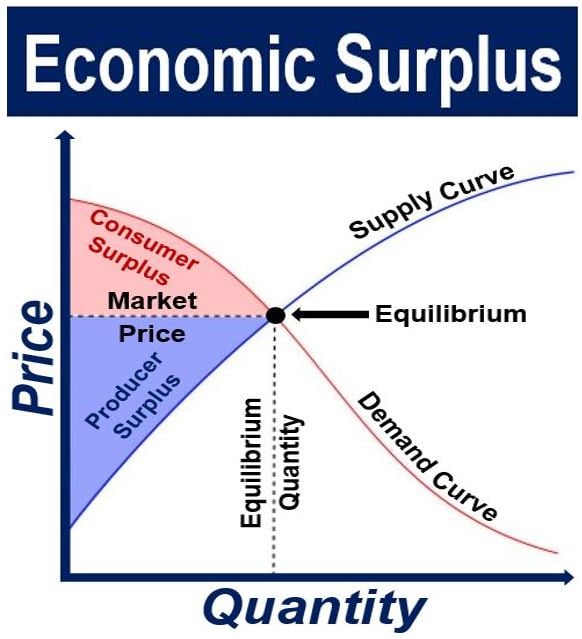

On a standard supply and demand chart, the consumer surplus is the triangular area above the equilibrium price of a product and below the demand curve. This demonstrates that consumers would have been willing to purchase the first unit of the product at a higher price than the equilibrium price, a second unit for less (but still above the equilibrium price), etc. However, they paid, in fact, just the equilibrium price for each unit they purchased.

In the same supply and demand chart, the producer surplus is the area just above the supply curve, below the equilibrium price, which reflects the fact that producers would have accepted a lower-than-equilibrium price for the first unit, a second unit at a higher price but still below the equilibrium price, etc., yet they received, in fact, the equilibrium price for every unit they sold.

What happens when supply grows?

When supply of a product increases, the price goes down and consumer surplus get bigger, assuming the demand curve is sloping downward.

This benefits both the producers and consumers. When market conditions shift to create a surplus, it can signal producers to innovate or improve efficiency to maintain their profit margins. Consumers, who were already willing to purchase at the previous price, benefit from the discount – they may purchase more and receive additional consumer surplus.

Add to this the consumers who did not buy at the previous price but will do so now at the reduced price – they will also receive some consumer surplus.

Surplus – vocabulary and concepts

Apart from economic surplus, there are many other compound nouns in the English language that contain the word “surplus.” A compound noun is a term that consists of at least two words. Here are seven of such terms, their meanings, and an example of their usage in a sentence:

-

Budget Surplus

A situation where income or receipts exceed outlays or expenditures.

Example: “The government managed to maintain a budget surplus for the third consecutive year.”

-

Trade Surplus

Occurs when a country’s export values are greater than its import values.

Example: “This year’s report showed a significant trade surplus, signaling a strong international demand for our products.”

-

Inventory Surplus

An excess amount of inventory that exceeds the demand.

Example: “The unexpected inventory surplus forced the company to hold a clearance sale to reduce stock levels.”

-

Capital Surplus

Equity which is generated by the sale of shares above their par value.

Example: “The newly issued shares resulted in a capital surplus, thereby strengthening the company’s balance sheet.”

-

Resource Surplus

An abundance of resources exceeding the immediate consumption needs.

Example: “The country’s resource surplus in renewable energy has attracted foreign investments.”

-

Production Surplus

A situation where production exceeds the consumption needs.

Example: “The production surplus in wheat this season will likely lead to increased exports.”

-

Revenue Surplus

When actual revenue exceeds the projected or expected revenue.

Example: “The revenue surplus for this quarter will provide us with an opportunity to invest more in research and development.”

Two Educational Videos

These two interesting video presentations, from our sister YouTube channel – Marketing Business Network, explain what an ‘Economic Surplus’ and ‘Surplus’ are using simple, straightforward, and easy-to-understand language and examples.

-

What is an Economic Surplus?

-

What is a Surplus?