What is a reverse mortgage?

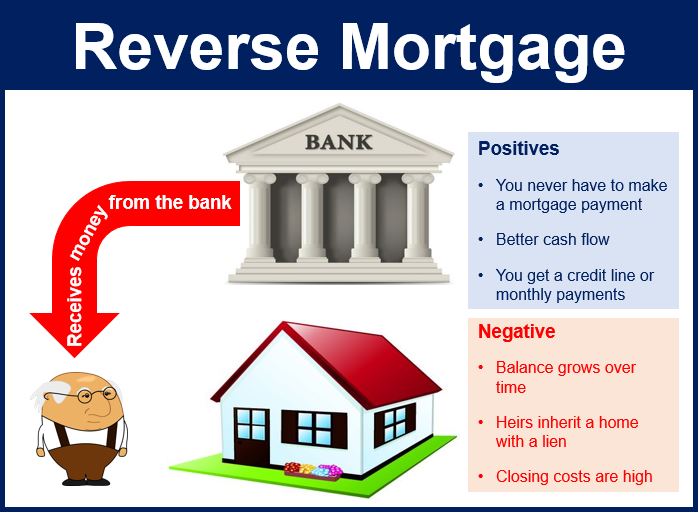

A reverse mortgage, also called a Home Equity Conversion Mortgage (HECM), is a type of loan that works in the opposite direction to other mortgages – instead of the homeowner paying monthly installments to the lender, the lender pays monthly installments to the homeowner, or opens up a credit line.

Reverse mortgages are available to homeowners aged at least 62 years. It allows people to convert part of the equity of their property into cash.

This type of mortgage was set up as a way to help retired individuals with low incomes use the wealth they had hidden in their homes to cover basic monthly living expenses, as well as to pay for health care costs.

In a reverse mortgage the homeowner can spend the money in any way he or she likes – there are no restrictions.

Homeowners need to weigh up the pros and cons before deciding whether to obtain a reverse mortgage.

Homeowners need to weigh up the pros and cons before deciding whether to obtain a reverse mortgage.

The borrower does not have to pay back the loan until the property is sold or otherwise vacated. As long as they live in the home, they do not have to make monthly repayments to pay back the loan.

When the homeowner dies the property is sold and the loan is repaid. In some cases, such as when property prices decline, the loan balance at time of death may be higher than the value of the house. The lender usually has to accept the loss and nobody is required to make up the difference.

The borrower also needs to be up-to-date with his or her current property taxes, homeowners insurance, and if applicable, condominium fees. The property must be the borrower’s primary residence, and he or she should have paid off some, or all, of their traditional mortgage.

The US Department of Housing and Urban Development defines a reverse mortgage as follows:

“A reverse mortgage is a special type of home loan that lets you convert a portion of the equity in your home into cash. The equity that you built up over years of making mortgage payments can be paid to you.”

Beware of reverse mortgage dangers, says CFPB

In February, the US Consumer Financial Protection Bureau (CFPB) published a report highlighting the many complaints about reverse mortgages. American consumers reported frustration with their loan terms, servicer runarounds, and problems with foreclosures.

Richard Cordray, CFPB Director, said:

“Consumer complaints tell us that the complex terms of reverse mortgages continue to be misunderstood.”

“As more **baby boomers choose reverse mortgages to tap into their home equity, they need to understand the unique terms and features of this product. Our advisory can help those who have already chosen reverse mortgages to plan ahead for loved ones.”

** Baby boomers are people who were born between 1946 and about 1964.

Recent studies have estimated that 41% of Americans aged between 55 and 64 years have no retirement savings account (Baby Boomer magazine quotes an even lower figure), but 74% of them own their homes and have accumulated good equity.

Consumers access this home equity either by refinancing their original mortgage, getting a reverse mortgage, selling their property and downsizing, or taking out a home equity loan (also known as a second mortgage).

The CFPB says there is currently a mismatch between consumer expectations and the way reverse mortgages function. For example, many struggle to understand how rapidly their loan balance shoots up and their home equity declines.

According to the CFPB, the main complaints regarding reverse mortgages are:

Adding new borrowers to a loan: heirs, spouses and dependents are not allowed to take over the loan. Banks say this is because the loan amount is partly calculated using the borrower’s age – loan repayment is triggered when the last borrower either moves out or dies.

Runaround problems when trying to pay off the debt: after the borrower dies, hairs can sell the property, repay the loan balance, or pay 95% of the property’s appraised value. There have been many complaints that loan services are unclear about how consumers can settle the debt. There is a lot of frustration regarding appraisal delays, badly-performed appraisals, inflated home values, and unanswered telephone calls and written requests.

Foreclosure problems: the borrower is responsible for property taxes and homeowner’s insurance. About 10% of homeowners are at risk of losing their properties early because they have failed to keep their payments up to date. CFPB received reports of loan services companies determining incorrectly that homeowners’ taxes were overdue.

CFPB has issued an advisory to help reverse mortgage borrowers.