There isn’t a business or industry on the planet that hasn’t been impacted – significantly – by the major changes in the world of technology over the last 20 years.

Most every aspect of our day-to-day lives has been heavily influenced by our easy access to incredible technologies that existed only in the wildest dreams of science-fiction authors even just 50 or 60 years ago.

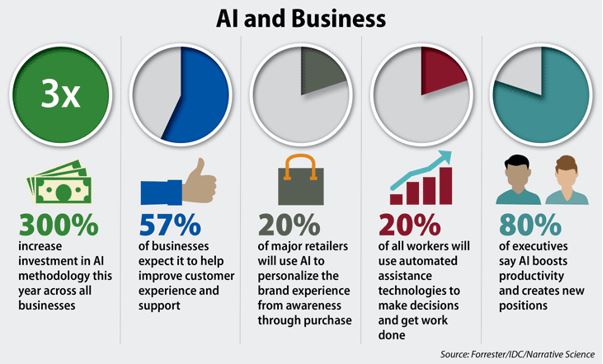

Artificial intelligence (also known as “AI”) is rapidly transforming things from top to bottom, impacting industries large and small, and none maybe more so than the world of finance.

Lending organizations all over the world (traditional and nontraditional) are taking advantage of all that AI has to offer. As lending products and term loans diversify, companies are using AI to overhaul their business process, capitalizing on Big Data and machine learning, and using the technology to not only improve the offers they make available to clients but to boost their bottom line as well.

According to Yanis Mendoza, an expert blogger in the title loan industry, some of the title loan lenders on her list are now exploring the possibility of incorporating AI into their loan decision process. Below we dig a little deeper into how AI is helping to increase the bottom line for lenders all over the world.

Big Data Changes Everything

Never before has so much granular data been available for complex decisions, particularly when it comes to their financial behavior. This Big Data is being leveraged by lenders globally to offer better services, better solutions, and more “risk proof” offers than at any other point in human history.

The fact that AI can compile a detailed “behavioral chart” that accurately predicts the viability of each loan based on the data accumulated — and do so in a split second — speeds up the loan application timeline, but it also adds a lot more security to the lending process — read more here from Deloitte.

Risk Reduction Across the Board

Artificial intelligence, when used properly, can reduce risk reduction across the board, particularly when AI systems are used during the loan origination process.

AI systems can streamline the origination process, eliminating a lot of the potential human errors that occur when loans are being underwritten. AI won’t overlook critical factors that may point to red flags, it won’t allow things to “fall between the cracks”, and will play a huge role in detecting specific patterns of behavior for those who may be a higher default risk.

This is not to suggest that AI is picture-perfect or infallible. But it does take a lot of the human element out of the system by analyzing data patterns and providing unbiased judgments.

All of this does a lot to minimize risk for lenders in general but it also does quite a bit to democratize the actual lending process at the same time. AI systems are built to be data-driven only, which means they are always looking out for the best interests of the lending institution itself (and their bottom line).

How AI Is Used to Determine Credit Worthiness

At the end of the day, lenders are always looking to ink smarter loans and offer smarter financial packages — and all of this hinges on their ability to find people that are most likely to not only pay back the principal of these loans but also to pay back the interest as well.

In the past, lenders traditionally looked at only a handful of key metrics to determine the creditworthiness of potential clients — mostly because they just didn’t have the “bandwidth” or ability to number crunch the multitude of different data points available.

With AI handling the heavy lifting, all of this data can be analyzed in a split second. AI can number crunch and look at a variety of different factors that traditional lenders wouldn’t have even considered in the past delivering a favorability rating faster than human loan originators ever could.

AI isn’t just going to speed things up (helping you to provide more loans and to get more deal flow in your funnel), but it’s also going to help you offer smarter loans. And smarter loans mean a bigger profit.

At the end of the day, we are still in the infancy of artificial intelligence, and things are only going to get more exciting (and more advanced) as time goes on.

Video – Artificial Intelligence

Interesting related article: “What is Machine Learning?“