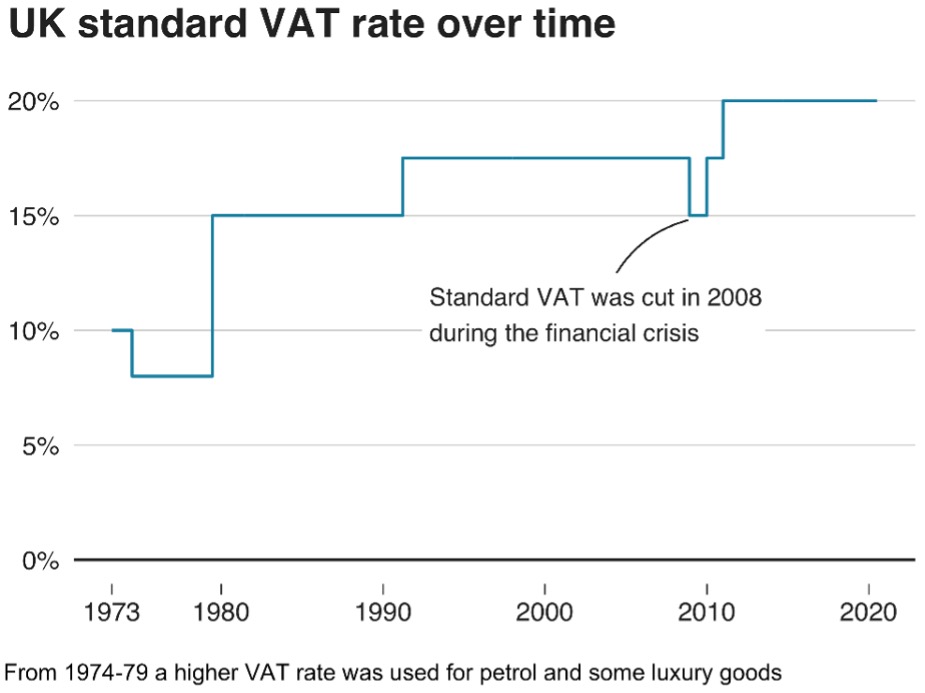

Value Added Tax, or VAT, is the duty you need to pay when you purchase goods and services. The standard pace of VAT in the UK is 20%, with about a large portion of families spend cash on things at this rate. There is a decreased pace of 5%, which applies to certain things like children vehicle seats and home energy.

The lower rate additionally as of now applies to clean items, albeit, in the March 2020 Budget, the public authority declared it would quit charging VAT on these products from 1 January 2021. At the point when you see a cost for something in a shop, any VAT will, as of now, have been added. There are likewise different things for which you don’t need to pay any VAT, like most general store food, youngster’s apparel, papers, and magazines.

How much money does VAT raise?

The Office for Budget Responsibility (OBR) expected in March that VAT would raise £136.6 bn in 2019-20. That is equal to around £4,800 per household and embodies 16.8% of all the money the government receives through taxes. VAT accounts for around 6.2% of GDP, the total value of goods and services produced in the economy.

VAT and VAT Reverse Charge:

“VAT Reverse charge is the phenomenon in which the customer or end-users account for the VAT directly to the HMRC.”

The intermediate supplier or sub-contractors has nothing to do with the collection of tax. The supplier will not deduct the specified VAT from the invoices issued to the customers. The end-users themselves have to submit the dues to HMRC as their responsibility.

Construction industries offer different tasks that are related to amendments in a building or constructing it from the very first brick. No matter what the work actually is, it may carry a specific amount of VAT and VAT Reverse Charge along with it. Both VAT and VAT Reverse Charge are applicable on goods as well as services.

The VAT and VAT Reverse charge, on the whole, may be 5% or 20%. In some goods and services, you have to pay only 5% of the VAT. For some other specified goods and services, you have to pay 20% of the total cost as VAT.

But giving 5% or 20% is not a big issue at all because you can claim back your additional tax through a specified process which is termed as VAT Reverse Charge. The collected VAT and VAT Reverse Charge will be transferred to the main government agency after a certain time. HMRC- Her Majesty Revenue and Customs is the main governmental agency that ultimately collects VAT.

In other words, either the tax is paid as VAT or as VAT reverse charge. It is HMRC who finally receives the taxes.

“The VAT Reverse Charge process has been effective since 1 March 2021″

Can VAT be claimed?

You can guarantee the VAT back. However, you need to go through some significant focuses first. Before you consider claiming the VAT, you should be VAT enlisted! In the event that you are not VAT enrolled, you cannot make a difference in claiming VAT back. You should enlist your business for VAT if your available turnover surpasses £85,000. Or, on the other hand, for another situation, you may enlist yourself in an organization with somebody. In the two cases, you will get an endorsement that conveys a VAT number alongside some different subtleties.

In the event that you are not VAT enlisted, you cannot claim back VAT. Around there, it is prudent to stay underneath the VAT application limit. Once in a while, asserting a VAT claim can be mind-boggling. If you are unsure if your business can claim back VAT, you can ask for advice from financial experts. Legend Financial has a group of experts who can assist you with support VAT.

Reclaiming VAT on procurements done before registration

Goods

On the off chance that you need to recover VAT back on the procurement of things, you need to fill the accompanying conditions. The deal ought to be made four years before your VAT enrollment.

- The items got by you under the same account that is registered for VAT as well.

- The items are still in use.

- You cannot reclaim VAT back on items purchased in the past if the following conditions occur.

- You have consumed your items before your VAT registration

- Items being sold before VAT registration

Services

The following conditions should be entertained if you are trying to reclaim VAT back. It will smear to the services acquired 6 months before VAT registration.

- You had acquired services under the same account that was registered for VAT as well.

- Services were acquired for VAT taxable business specifically.

Services provided in the past cannot help you in reclaiming the VAT. Some circumstances apply to this statement. These are as follows:

- Services related to items that are not in use now

- Services that are exempt from VAT

This article discussed some of the common questions related to VAT that you should be aware of. If you want to learn more about the concept of VAT, you can run through the following articles:

· How Long Can Be Vat Reclaimed Back?

· How Do You Reclaim A Vat Refund?

· What Do I Need To Check Before Reclaiming Vat Back?

· What If Your Invoices Are Mishandled?

· How Can An Accountant Help Me To Reclaim Vat Back?

Interesting Related Article: “Calculating Your UK VAT in a Post-Brexit World“