Blockchain technology allows companies to record information and track assets in a way that cannot be tampered with, changed, or hacked. Fundamentally, a blockchain is a digital or electronic ledger of transactions that is copied and dispersed across a network of operating systems on the blockchain.

Jason Simons with ICS in Austin, TX shares what you should know about blockchain tech and what it can do for your business.

The Fundamentals of Blockchain

Essentially, any item with value can be exchanged and tracked on a blockchain network. These are called assets, which can be either tangible or intangible. Tangible assets tend to be things like real property or cash, while intangible assets aren’t material and include things like trademarks, copyrights, and intellectual property. Using blockchain technology helps to reduce costs and risks for your business and other involved parties.

Elements of Blockchain

There are three key elements of blockchain technology:

-

Immutable Transaction Data

Once a transaction has been recorded in the blockchain, the data cannot be changed or altered. Any errors must be adjusted by creating a new transaction that reverses the error, and both ledger entries will be visible to all authorized parties that have access to the blockchain network.

-

Smart Contracts

Smart contracts are predetermined sets of rules that are applied automatically to transactions and stored in the blockchain. For example, the terms and conditions of a particular transaction can be stored in the network and when any matching transactions are entered, that data is then applied to the transaction. Smart contracts can be tailored at a granular level to meet the unique needs of your organization.

-

Secure Shared Ledgers

A shared ledger ensures that transactions are recorded only once and the potential for duplicated entries is eliminated. This saves time and ensures that all authorized parties on the network have access to the same up-to-date information for a transaction.

Types of Blockchain

Guy Baroan from Baroan Technologies in New Jersey introduces us to three different types of blockchain:

-

Private Blockchains

A private blockchain is the type of blockchain described above, where permission must be granted for users to gain access to the network. Private blockchains are more centralized than public networks, and transactions are private. Consortium blockchains are a type of private blockchain controlled by a group versus an individual or single entity.

-

Public Blockchains

Public blockchains are open source and allow any user to add a record. All transactions are fully transparent, discouraging censorship and creating a completely decentralized data source. Public blockchains have a token that rewards users that participate in the network. One of the most well-known public blockchains is Bitcoin.

-

Hybrid Blockchains

Hybrid blockchains offer the security and authorized-access-only of a private blockchain along with the benefits of the transparency of transactions within a public blockchain. Organizations can select which data they want to remain private and which data is accessible to the public.

Benefits of Blockchain

There are multiple benefits to blockchain tech, including but not limited to:

- Improved security. Each transaction record is immutable, meaning it cannot be changed or altered in any way, not even by the system administrator. Blockchain networks are members-only, making them inherently more secure than other types of networks.

- Greater efficiency. Duplication of transaction recording and the need for record reconciliations aren’t an issue with blockchain technology. Automated rules can be applied to transactions, further increasing the speed at which transactions can be recorded.

- Better trust. Only authorized parties are allowed on a blockchain network, ensuring confidentiality and privacy. Your company’s data will only be shared with members of your network that you have whitelisted, or specifically authorized access.

How Blockchain Technology Works

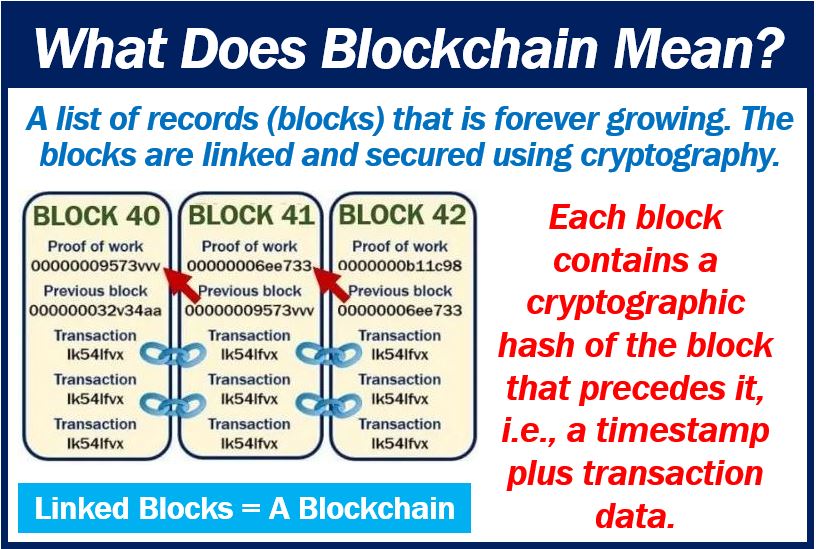

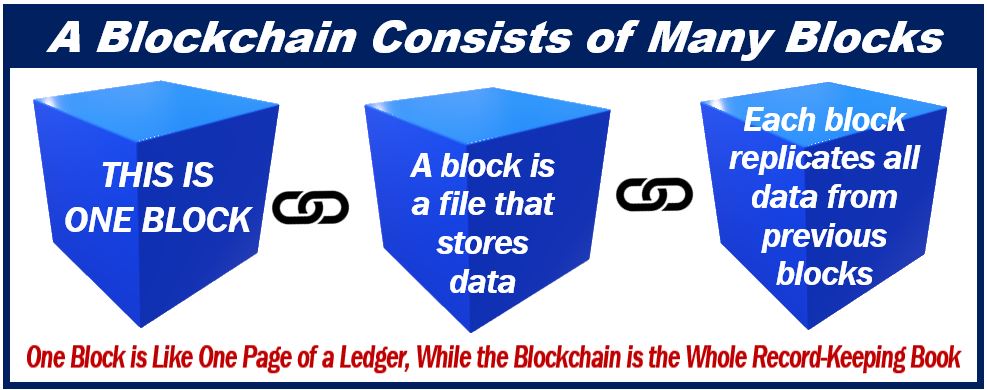

Each transaction that is recorded is done so as a “block” of information or data. Related blocks are connected to form a data chain that can change ownership and move across the network. Each block of data is time-stamped and the chain is sequenced and securely linked, preventing anyone block of information from being tampered with in any way or another data block being inserted in between two existing blocks.

Applications for Blockchain Technology

There are numerous applications for blockchain, such as:

- Monitoring supply chains

- Processing payments

- Tracking digital identification

- Electronic voting

- Property and land transfers

- Tax and regulation compliance

- Medical recordkeeping

- Managing networks connected to the Internet of Things (IoT)

- Trading equity

- Tracking and managing prescription drugs