Bank capital is a storage of cash and safe assets that banks hold as a buffer. Bank capital is like the airbags in vehicles. It is there to protect banks’ creditors in case they have to liquidate their assets. In most countries, regulators make banks have a minimum capital adequacy ratio.

From an accountant’s viewpoint, bank capital is the bank’s total assets minus liabilities. In other words, the difference between the value of what it has and what it owes.

A bank’s assets include cash, interest-earning loans like inter-bank loans, letters of credit, and mortgages. Bank assets also include government securities.

A bank’s liabilities comprise any debt it owes plus loan-loss reserves.

According to the Bank of England’s document Bank capital and liquidity, a bank’s capital can be viewed as its “own funds,” distinguishing it from borrowed money like deposits. These own funds typically include items such as retained earnings and share capital; in other words, borrowed money that must eventually be repaid is not considered “own funds.” Taken as a whole, these own funds are equivalent to the difference between a bank’s total assets and its liabilities.

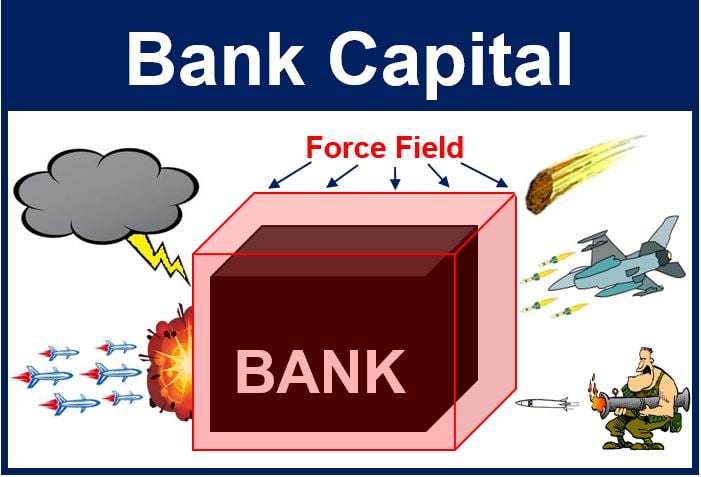

Bank capital acts as a cushion (force field) so that the financial institution can absorb the shocks from financial crises.

Since the 2007/8 global financial crisis, banks, the media, and regulators have been talking a lot about bank capital. After 2014, many jurisdictions further tightened capital and liquidity requirements under Basel III, including the introduction (and subsequent full phase-in by 2019) of the Liquidity Coverage Ratio (LCR) and, by 2021 in major economies, the Net Stable Funding Ratio (NSFR). These measures built on earlier post-crisis reforms to require higher and better-quality capital across the banking industry.

According to the Federal Reserve Bank of San Francisco, bank capital provides a strong incentive for prudent management because owners’ equity is at risk if the bank fails. As a result, capital plays a critical role in ensuring the safety and soundness of both individual banks and the banking system as a whole.

Difference between bank capital and bank liquidity

Although there is a close relationship between a bank’s capital and liquidity, they are quite different.

Liquidity is a measure of how easily one can convert assets into cash. We can convert liquid assets into cash immediately if we have to meet financial obligations.

Examples of liquid assets include cash, government debt, and central bank reserves. For a financial institution to remain viable, it must have enough liquid assets to meet short-term obligations. The term ‘viable,’ in this context, means capable of making a profit year after year.

For example, it must have enough liquidity to deal with withdrawals by account holders.

Capital acts as a financial buffer which can absorb unexpected losses. It is the difference between a bank’s assets and liabilities.

For a bank to remain solvent, its assets must be greater than its liabilities.

More banks fail or need government help during a financial crisis because they don’t have enough capital or liquidity. Sometimes banks have a combination of both problems.

US Federal Reserve requirements today

The US Federal Reserve Bank has worked to increase the levels of both capital and liquidity in financial organizations. The Federal Reserve Bank (Fed) is the central bank of the United States.

Regulators across the world also implemented The Basel III Capital Standards. Large firms must hold enough capital to absorb losses in severely adverse environments. During crises, they must also continue lending to businesses and households.

The Basel III Liquidity Coverage Ratio came into force in September 2014 and was fully phased in by 2019 in most jurisdictions. Regulators across the world got together and formulated the Basel III Liquidity Coverage Ratio. It requires large institutions to hold levels of liquid assets “sufficient to protect against constraints on their funding during times of financial turmoil.”

The Fed said that from 2008 to 2012, the country’s largest banks doubled the amount of high-quality capital they held. Subsequently, additional regulatory measures introduced after 2014 have spurred even further increases in capital. In fact, by 2024, the largest U.S. banking firms had more than tripled their Common Equity Tier 1 capital compared to 2009 levels, reflecting an ongoing emphasis on building stronger loss-absorbing buffers.