Managing your money is challenging enough in a normal year. In 2020, it’s become a whole different experience,

This year’s pandemic has created tremendous uncertainty across all aspects of life. Many businesses have shut down and jobs have been lost, either temporarily or for good. In fact, new data from the Pew Research Center shows that half of working Americans who lost their jobs during the pandemic are still unemployed.

At this point in time, there’s little consensus on when life will get back to normal. Maybe your personal finances are hanging in there at the moment. Perhaps you’re really struggling. Whatever your current situation is, here are eight crucial money questions you need to ask yourself — and hopefully answer — in 2020.

1. What should I do if I lose my job or if I already lost it?

If you’re laid off by an employer, you should be able to collect unemployment. While this won’t replace all of your lost income, it can help you until you find another job.

The good news for job seekers in 2020 that companies are still hiring, even if the current unemployment rate doesn’t indicate it. What’s more, COVID-19 has prompted a number of companies to adopt remote working arrangements. This means you can work for a company based hundreds of miles away and not have to relocate.

In addition, opportunities for gig work exist. You can find paying gigs as a freelancer or a driver for a rideshare service, among the many opportunities out there.

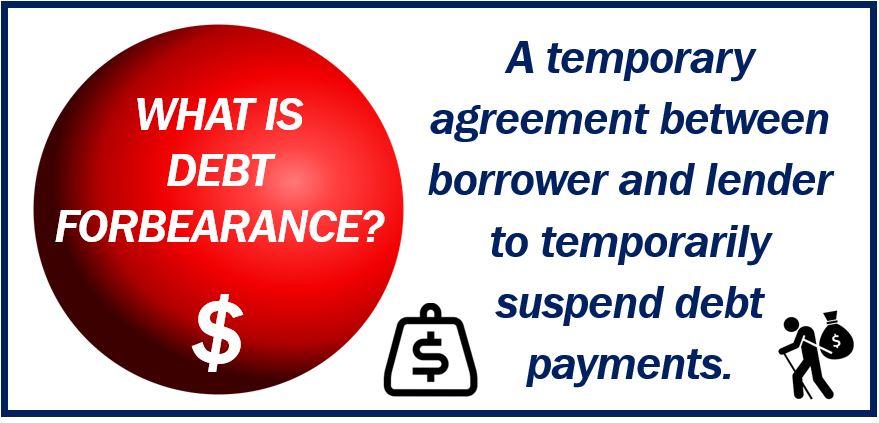

2. Should I take advantage of debt forbearance?

Forbearance is a temporary postponement of loan payments without penalty. Many lenders are offering forbearance on mortgage loans, student loans, and other debt to help people adversely affected by COVID-19. To qualify, borrowers have to demonstrate they are having difficulties making payments because of a financial setback.

Depending on the terms of your forbearance, you may have to pay the interest due during the forbearance period. Also keep in mind that interest may continue to accrue during the time you are not making payments. For mortgage loan forbearance, you will likely have to continue paying the amount that goes into your escrow account to cover taxes and insurance.

3. How can I reduce the amount of debt I have?

The less debt you have, the easier it is to get through a difficult year. So you should ask yourself this year how to minimize your debt.

The best answer is to avoid accumulating more debt this year or beyond. Set a budget, live within your means, and build an emergency fund to cover unexpected expenses.

If you have the means, you should also consider making additional payments to your debt balances to erase them sooner.

Another tactic is consolidating unsecured debt such as personal loans, medical bills, and credit card loans into one loan. You can also potentially lower your interest rate and the amount of money you spend each month on loan payments.

Debt consolidation can be done through:

- Transferring debt from high-interest loans and credit cards to a low-interest credit card

- Taking out a debt consolidation loan and using the loaned funds to pay off the balances on your unsecured debt

- A home equity loan if you have sufficient equity in your home

4. Is now a good time to buy a house?

In between the latest headlines regarding the COVID-19 pandemic, you’ve likely seen several reports on record low mortgage rates. Being able to get a 30-year fixed mortgage at under 3 percent is enticing to renters looking to buy for the first time or current homeowners thinking of upgrading.

How high or low rates are is only one factor in determining whether to buy a home. Here are some other things to consider regarding the current housing market.

- Home prices have risen sharply in many markets because there are more potential buyers than sellers. Therefore, you may be paying a premium on your home purchase.

- Lenders have tightened standards in response to the pandemic, which may make it more difficult to get a loan. This is especially true if your credit score is less than stellar.

- There remains enough economic uncertainty that you should proceed cautiously on major purchases.

6. Should I refinance my mortgage?

If you own a home, low rates make it tempting to refinance your mortgage. Because of how low mortgage rates are, it’s worth investigating whether you can lower your payment or reduce the term period on your loan.

To qualify, you will typically have to demonstrate that you’ve consistently made payments on time, that you have at least 10 percent equity in your home, have the income to pay the new mortgage payment, and have an adequate credit score.

Also keep in mind that a mortgage refinance often requires many of the same fees and closing costs associated with a purchase mortgage. Therefore, it may not be worth refinancing if you don’t plan to live in the home much longer or if there’s a chance you may have to move in the near future.

7. Am I adequately insured?

COVID-19 has reminded most of us that anything can happen to anyone at any time. But rather than live in constant fear, you can deal with the risks of living by having adequate insurance.

The types of insurance you should strongly consider that can help through the current pandemic and beyond include:

Disability insurance

In the event you can’t work for an extended period due to injury or illness, a personal disability insurance policy can protect you by replacing a portion of your income. There are many misconceptions about this type of coverage, so if you haven’t already, make sure to take some time to learn how disability insurance works and evaluate your coverage options.

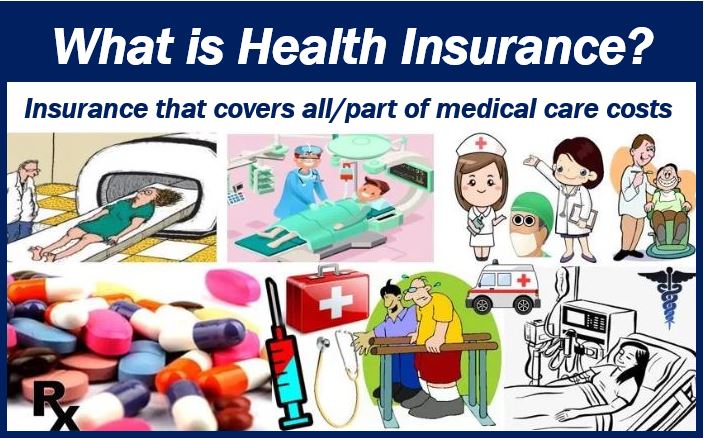

Health insurance

If you are unemployed or self-employed, make sure you have sufficient health insurance coverage. Health insurance helps pay some or all of the cost of doctor visits, prescription drugs, hospital stays and surgical procedures. Premiums you pay for health insurance is a tax deductible expense. If you currently don’t have an employer-sponsored plan, you can shop for individual coverage at HealthCare.gov.

Critical illness insurance

COVID-19 may lead to long-term damage to a person’s vital organs, which can result in critical illnesses later. Treating critical illnesses gets expensive fast and unfortunately health insurance may not cover the entire balance. That’s why getting critical illness insurance may be worth it if you have gaps in coverage to fill . This policy will pay a lump sum benefit if you are diagnosed with a covered illness.

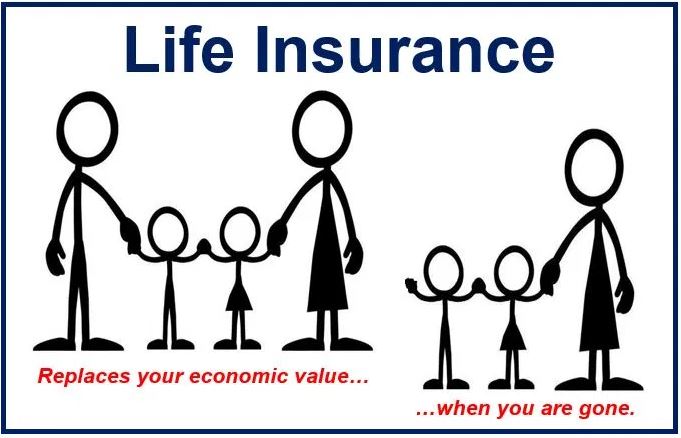

Life insurance

Although the risk of dying for COVID-19 is relatively minimal, it does happen. And there are dozens of other ways you can die unexpectedly. Life insurance can protect your family and loved ones from losing your income by paying a death benefit to those beneficiaries.

7. How do I financially prepare if something like this happens again?

The last twenty years have brought the collapse of technology stocks, a terrorist attack, two wars, a major financial crisis, and now a global pandemic.

The best way to endure financially through tough times is to prepare during periods of prosperity. It’s easy to spend every dollar we earn when the economy is humming. But eventually a point will come where it won’t. If you set aside a little excess during the good times and have the discipline to live below your means, you can better handle the not-so-good times.

No matter how much or how little you earn, you need to save money. Having money in savings helps you deal with emergencies and unbudgeted needs. It also minimizes the need to borrow money and pay interest on credit cards.

If little has changed for you financially in 2020, use it as an opportunity to prepare for the uncertainty of tomorrow rather than indulge in your current good fortune.

Video – What is Personal Finance?

Interesting related article: “What is Insurance?“