In finance and accounting, an asset refers to anything of economic value that we own. In fact, it is anything that a person finds useful or valuable.

Anything that we can convert to cash is probably an asset. Assets are items that people, companies, or even a country owns or controls. We also expect that assets will provide future benefit.

Additionally, companies see assets as items that they can use to meet debts, legacies, or commitments.

We record the value of assets in a company’s balance sheet. In other words, the items represent what companies own. Furthermore, assets include the money or other valuables that an individual or business owns.

Other uses of “asset”

We can also use the term when talking about a person, skill, or quality. Look at the sentence below:

“She has been a great asset to the team.” In this context, “asset” means a benefit or positive contribution.

Here are more sentences using “asset” to describe a skill or quality:

- “His ability to negotiate tough deals has been an undeniable asset to the sales department.”

- “Her fluency in multiple languages is a valuable asset in our international company.”

- “The engineer’s expertise in sustainable design has become a critical asset to our green initiatives.”

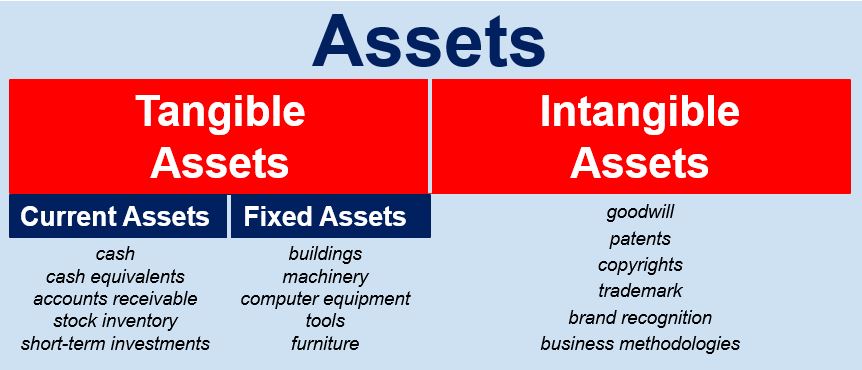

Tangible Assets

In business, we divide tangible assets into two subcategories:

- Current Assets and

- Fixed Assets.

For example, inventory consists of current assets. Buildings, on the other hand, are fixed assets.

Current assets: We expect to sell or use a current asset during a business’s fiscal year. Examples of current assets include cash, cash equivalents, accounts receivable (money owed by customers), stock inventory. Short-term investments are also current assets.

Fixed assets: We also call fixed assets PPE. PPE stands for property, plant, and equipment. We only use fixed assets for the long-term rather than the short-term.

Examples of fixed assets include buildings, machinery, and tools. Computers and furniture are also fixed assets. We also write off fixed assets against profits over their lives by charging depreciation expenses.

Intangible assets

Intangible assets include all nonphysical resources and rights that a company owns. In other words, intangible assets are abstract things, rather than things we can touch.

An example of an intangible asset is goodwill. Trademarks and patents are also intangible assets.

International Accounting Standards Board standard 38 (IAS 38) defines an intangible asset as: “An identifiable non-monetary asset without physical substance.”

US GAAP classifies intangible assets into:

- Purchased vs. Internally Created Intangibles, and

- Limited-Life vs. Indefinite-Life Intangibles.

Accountants typically expense these assets relative to their respective life expectancy.

We amortize assets with an identifiable useful life over their economic or legal life. The amount by which we amortize the asset equals its cost minus any residual value. Examples of intangibles assets with a finite useful life are patents and copyrights.

We reassess intangible assets with an indefinite life every year for impairments.

The Accounting Equation

Assets are an important component of the accounting equation because they structure a balance sheet:

Assets = Liabilities + Capital

Liabilities = Assets – Capital

Capital = Assets – Liabilities

Etymology of ‘asset’

Etymology means the study of the history of words and how they have evolved. Etymologists believe that the modern English word ‘asset’ came from the Old French assez (11 century). ‘Assez’ means “compensation, satisfaction, sufficiency”. The Latin ad satis means “to sufficiency”.

‘Asset’ started as a legal term in English, meaning “sufficient estate”, i.e. to satisfy legacies and debts. Its meaning in the 1500s included “any property that we can theoretically convert into cash.”

Looking after other people’s assets is known as asset management. In fact, asset management is a giant industry that globally exceeds $53 billion.

Strategic asset management also involves assessing the liquidity of assets, which is the ease with which they can be converted into cash without affecting their market value.