Credit score – definition and meaning

If you don’t know your Credit Score, you form part of the 56% of American consumers who also have no idea, according to a survey that the American Bankers Association commissioned. However, even though many people don’t know what it is, we all have a credit score.

Knowing your credit score can determine whether or how you can get credit cards, mortgages, or car loans. It can also determine whether you can rent a property.

Additionally, your credit score may affect your insurance and employment decisions.

A good credit score can often lead to lower security deposits for utilities or housing rentals, reducing upfront costs.

Nessa Feddis, from the American Banker’s Association’s (ABA), said that people might have a shock when they apply for a loan.

They might discover that they have a low credit score. If you have a low score, your application may fail. Even if your application is successful, the interest rate on the loan may be high.

The credit score survey

ABA commissioned Ipsos Public Affairs to carry out the study, which included 1,000 American adults between August 8th and 13th, 2013.

The survey found that:

– 42% of respondents knew their credit score.

– 56% did not know.

– 2% did not provide an answer to the questions.

What is your credit score?

Your credit score represents your creditworthiness. In other words, it is an assessment how you are likely to behave with your debt obligation.

Your credit report contributes toward your credit score. The credit report has details on how punctual you are on paying your bills. It also includes data on how much of your available credit you use. All the credit report data contributes toward your credit score.

You can get your credit scores from major credit bureaus, such as Equifax, TransUnion, and Experian. These companies gather people’s and company’s payment and credit data. They then sell this information to lenders.

When lenders consider potential candidates, they use their credit scores to decide whether to lend. It also helps them determine how much to lend, and at what interest rate.

A person’s credit score may also determine whether the lender decides to ask for additional security on the loan.

People also use credit scores when screening insurance applications and job candidates.

Feddis added that you can take steps to improve a low credit score. However, it is a slow and long-term process. Fast fixes do not exist.

If you make sure you pay your debts and bills on time, your score will gradually improve. Put simply; you need to demonstrate over time to lenders that you are a low risk.

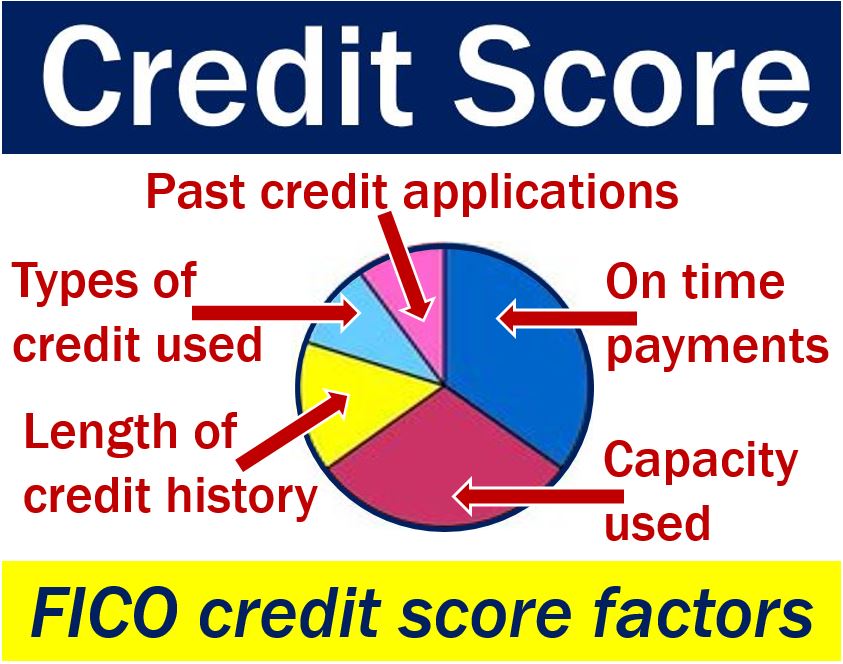

The FICO credit score

In the United States, the FICO score is the most famous credit score model. All the major credit reporting bureaus use it.

Your credit report can contain different data at each of the bureaus. Therefore, FICO scores may vary depending on which bureau has issued the score.

The FICO score is made up of the following components:

Payment history

Payment history represents 35% of the total score. People who are late in paying their bills have a lower score compared to those who pay them on time.

-

Credit utilization

Credit utilization represents thirty percent of the total score. It is the ratio of current revolving debt to the total available revolving credit or credit limit. The more debt you pay off, the higher your score will be here.

-

Credit history length

Credit history makes up fifteen percent of the total. As your credit history gets longer your FICO score usually improves. Unfortunately, very young adults are at a disadvantage, because they do not have a long track record.

-

Types of credit

Ten percent of the total FICO score comes from how well you manage types of credit. For example, how well do you manage consumer finance, your mortgage, installments, etc.?

-

Recent credit searches

Recent credit searchers represent ten percent of the total. If you have applied for many loans and different credit cards recently, you may score badly here.

Tips for a good credit score

-

Do

Order your annual credit report.By law, Equifax, TransUnion, and Experian have to provide you with a free copy of your credit report annually. However, they will only do so if you ask for it.

You can get a free copy of your credit report at AnnualCreditReport.com (Tel: 1-877-322-8228).

Understand the power of credit. Financial institutions view your credit history as data on what your future financial behavior is likely to be. If you use credit wisely and build a good credit history, you are more likely to be a successful loan applicant. You will also benefit from low interest rates on your loans.

People who use credit wisely succeed in renting properties, purchasing a home or car. In fact, you might even have better job prospects.

Read the small print. Before signing any credit contract, read the small print carefully. A credit application is a contract.

Keep up with minimum payments. Make sure you pay at least the minimum due on time. If you have problems making payments contact your creditor immediately.

Notifying the lender helps avoid extra fees and a higher APR. Pay more than the minimum if you want to settle the loan more quickly.

Beware of credit report ‘fixers.’ Be wary of those who say that they can fix your credit report. The only thing that can fix that is a gradual improvement in your payment history. In other words, what they tell you to do you could do on your own anyway.

-

Don’t

Do not overspend. Only spend what you can afford. Remember that you have to pay back loans. You are responsible for managing your debts and making sure you can keep up with your commitments with lenders.

Try not to reach your credit limit, and above all, do not ‘max out’ your cards.

Never pay bills late. If you are late paying your bills, your credit score will suffer. If you think you are going to be late in any payment, contact your creditor.

Don’t ignore credit trouble warning signs. Examples include only always paying the minimum amount, often paying late, and using cash-advances to meet daily living expenses.

To regain control of your finances, consider talking to a non-profit financial counseling organization. For example, the National Foundation for Credit Counseling has helped many people regain control of their finances.

Never share personal details. Do not reveal your credit card or personal data if there is no transaction. Identity theft is big business, and there are many sophisticated phishing scams.

If you believe something may have compromised your identity, let your bank know immediately. You should also file a complaint with the Federal Trade Commission – ”Identity Theft” (Tel: 1-877-438-4338).

Two Educational Videos

These two interesting videos that are featured on our partner YouTube channel, Marketing Business Network, explain the meanings of ‘Credit Score’ and ‘Credit History,’ utilizing easy-to-understand language and examples.

-

What is a Credit Score?

-

What is Credit History?