Economic assumptions are assumptions that a company makes about the general market environment. Specifically, the environment it plans to operate in during the period of its financial plan. Companies make economic assumptions regarding the upcoming state of the economy, i.e., the marketplace. Businesses try to predict what the business environment will be like and how it will affect their ability to generate profits.

Economists also make economic assumptions when they build economic models. Sometimes they make economic assumptions regarding levels of competition or marketing. They may also make assumptions about substitute goods.

Many economic models assume that the players in the marketplace have perfect information regarding their choices. Others may even assume that we can measure subjective human values quantitatively.

In this context, the word ‘marketplace‘ refers to ‘market‘ in its abstract sense.

Without economic assumptions, economists would not be able to produce quantitative economic models with meaningful conclusions.

Economic assumptions – two definitions

Below are two definitions of the term; one from a company’s and the other from an economist’s point of view:

Company’s viewpoint

This definition, from BusinessEnglish.com, explains economic assumptions from a company’s viewpoint:

“The set of assumptions that a firm will make about the upcoming economic situation.”

Economist’s viewpoint

This definition, which Mike Moffatt writes in ThoughtCo.com, explains the meaning of the term from an economist’s viewpoint:

“A basic assumption of economics begins with the combination of unlimited wants and limited resources.”

“All of economics, including microeconomics and macroeconomics, comes back to this basic assumption that we have limited resources to satisfy our preferences and unlimited wants.”

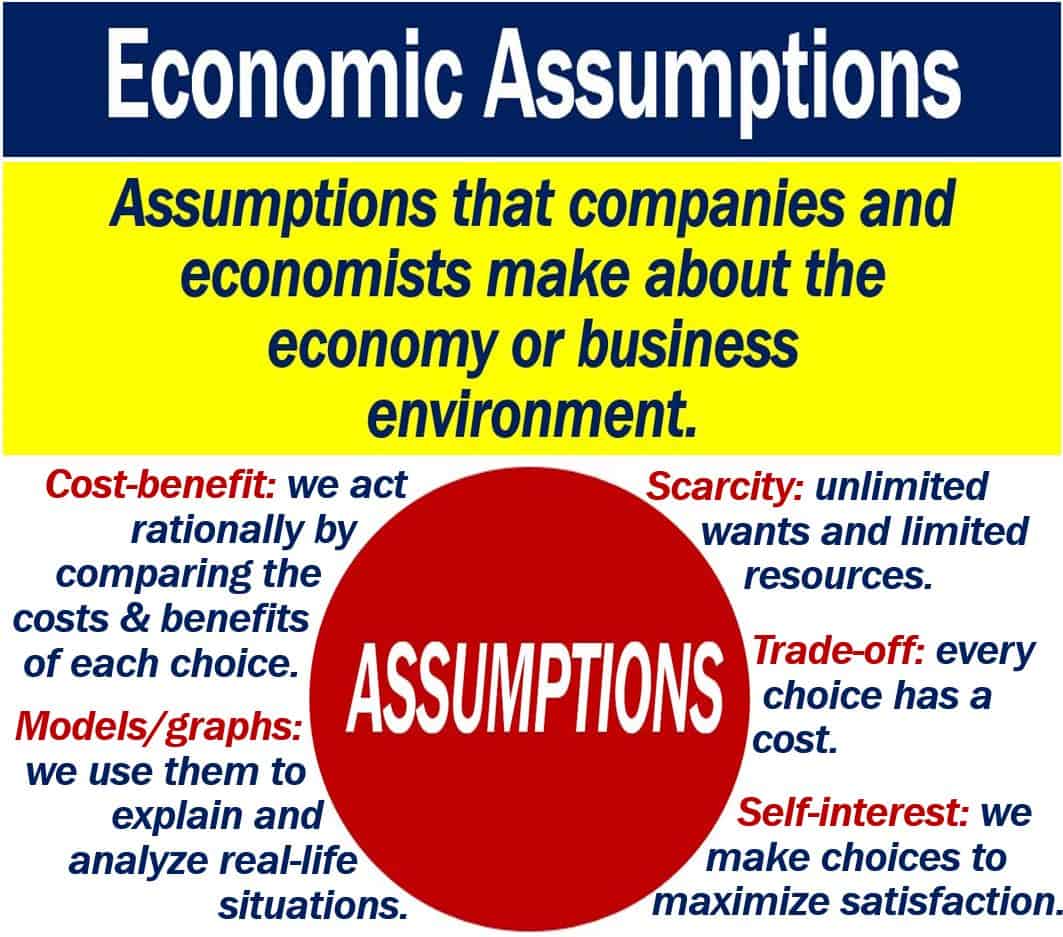

Five economic assumptions

According to economists, there are five basic assumptions that we make regarding economics: 1. Scarcity. 2. Trade-offs. 3. Self-interest. 4. Cost and benefits. 5. Models and graphs.

Scarcity

Scarcity or paucity refers to limitation. Raw materials, components, goods, and other supplies are limited. However, we exist in an environment with unlimited human wants.

This is one of economics’ fundamental problems, i.e., having limitless human wants in a market where resources that are not limitless.

Trade-off

If our wants are limitless but scarcity exists, we cannot satisfy all our wants. Therefore, we must make choices. When we chose one thing, we are subsequently trading it for something else.

In other words, every choice has a cost, i.e., a trade-off.

When we chose something, we also wonder what we will have to give up. We call this determining what the opportunity cost is.

In other words, first, we ask ourselves: “If I choose this, what will I have to give up?” Then, we can determine whether we are better off with our choice.

Self-interest

Our goal is to make a choice that maximizes our satisfaction. In other words, we all act in our own self-interest.

Costs and benefits

We all make decisions by comparing the cost and benefits of things. Whenever we make a choice, we compare the choice’s marginal costs against its marginal benefits.

In other words, we perform a cost-benefit analysis or benefit-cost analysis. This analysis is a type of economic analysis.

Models and graphs

Economists explain real-life situations through simplified graphs and models. They also use them to analyze real-life situations.