What is FICO Score? Definition and meaning

A FICO Score is a number that banks and other financial institutions use to measure the creditworthiness of a borrower or loan applicant. FICO stands for Fair, Isaac and Company, a data analytics firm with headquarters in San Jose, California. It focuses on credit rating services. Bill Fair and Earl Isaac founded the company in 1956.

The methodology behind the FICO Score involves complex statistical analysis, which is continually updated to reflect changes in consumer behavior and lending practices.

The FICO Score, a measure of consumer credit risk, has become the standard score in the United States for consumer lending. US lenders use this score when deciding whether to lend you money.

The score is based on a number of factors, including the person’s length of credit history, and total amount owed. The person’s payment history is also a factor.

The approximate makeup of the FICO Score used by U.S. banks and other lenders.

The approximate makeup of the FICO Score used by U.S. banks and other lenders.

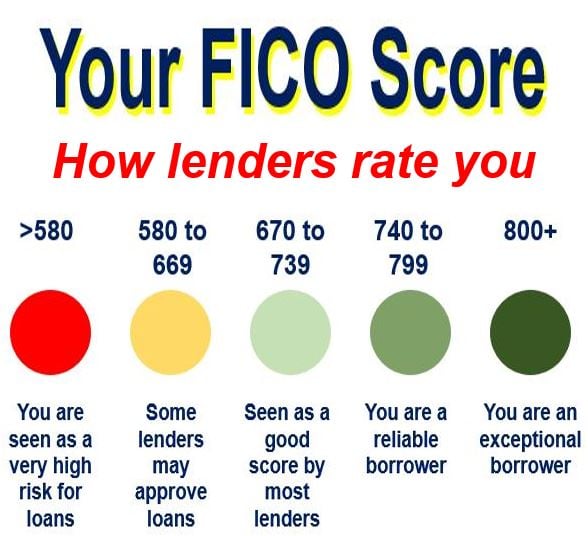

FICO Score range

A FICO Score ranges from 300 to 850. The higher your score the better your creditworthiness is estimated to be. Somebody with a high score would, therefore, likely get more favorable loan terms than a person with a low score.

Loan applicants with a score of less than 620 may find it difficult to get a loan at a favorable interest rate. Some younger applicants, in fact, may even find it hard to get a loan.

“Your FICO Scores consider both positive and negative information in your credit report. Late payments will lower your FICO Scores, but establishing or re-establishing a good track record of making payments on time will raise your score.”

FICO score categories

People’s FICO Scores are calculated according to five categories:

-

Payment History – 35%

This lists how well or badly the person has been in paying off bills. It includes details on debt repayments, bankruptcies, charge offs, repossessions, foreclosures, late payments, liens, judgments, and settlements.

More than 90% of all banks and lenders in the United States use the FICO Scores when deciding whether to approve a loan.

More than 90% of all banks and lenders in the United States use the FICO Scores when deciding whether to approve a loan.

-

Amounts Owed – 30%

This includes six different metrics in the debt category, such as the number of accounts with balances, debt to limit ratio, and amount owed across different kinds of accounts. It also has details on how much was paid down on installment loans.

-

Length of Credit History – 15%

We also call it the Time in File. As a person’s credit history spans a longer period, his or her FICO score may improve. This metric takes into account the average age of the person’s accounts and the age of his or her oldest account.

-

Credit Mix – 10%

This category is all about the types of credit used, such as revolving, consumer finance, mortgage and installment.

Consumers who have a history of managing different kinds of credit, for example, will have a better score.

-

Recent Credit Searches – 10%

This includes hard credit inquiries and recent searches for credit. These occur when applicants apply for a loan or credit card. Too many searches can harm your credit score.

Importance of each category varies

Your FICO Score is calculated based on these five categories. The importance of each one may vary, depending on a number of factors. The system factors people who have been using credit for a long time differently from those with a short credit history.

How important a particular factor is in a person’s credit score calculation depends on the overall data on their credit report. For some consumers, one factor may have a greater impact than it might for somebody else with a very different credit history.

Over time, as your credit report changes, so does the importance of any factor in determining your creditworthiness.

It is therefore not possible to accurately measure the precise impact of a single factor in how a credit score is calculated without looking at the whole report.

Access to your credit report

As a result of the FACT Act (Fair and Accurate Credit Transactions Act) of 2003, every US legal resident is entitled to receive a free copy of his or her credit report from each credit agency – Transunion, Experian and Equifax – once a year.

The credit reports have no details on individuals’ credit scores from any of the three agencies.

Experian, Equifax and Transunion run a website where users can obtain their free credit reports.

Non-FICO credit scores are available as an add-on feature for a fee of (usually) $7.95.

Beware of ‘imposter’ websites. The Federal Trade Commission has the following warning:

“Only one website is authorized to fill orders for the free annual credit report you are entitled to under law — annualcreditreport.com. Other websites that claim to offer ‘free credit reports’, ‘free credit scores’, or ‘free credit monitoring’ are not part of the legally mandated free annual credit report program.”

It is advisable to regularly review your credit report for inaccuracies or fraudulent activity, as these can affect your FICO Score and your ability to obtain credit

-

FICO Scores don’t include:

Your credit score does not have information regarding your:

- Marital status, religion, national origin, sex, color or race.

- Age (other types of scores might – not FICO).

- Occupation, employment history, title, employer or salary.

- Address.

- Current interest rates on any type of loan, credit card or account.

- Data on child or family support obligations.

Your FICO Score does not count requests that you personally have made for your credit report.

Improving your FICO Score

It is possible to improve your score, but it can take time – there is no ‘quick fix’. Financial advisors warn that many quick-fix efforts have a high risk of backfiring. You should treat any claims that firms and agencies make regarding quick-fix solutions with extreme caution.

In order to improve your credit score you need to show over time that you are able to manage your finances responsibly. The first thing to do is get a credit report from one of the three agencies.

-

Some tips

Below are some tips on improving your FICO Score:

- Dispute errors; mistakes can happen. If you think there is a mistake in your credit report, you should contact TransUnion, Experian or Equifax online.

- Keep balances as low as possible on credit cards and other revolving credits.

- Do not move debt around; pay it off.

- As a short-term measure to raise your score, do not close unused credit cards.

- Do not apply for a number of new credits cards that you have no need for, just to raise the amount of available credit. This approach might actually harm your FICO Score.

- Do not open credit accounts just to widen your credit mix; it is unlikely to improve your credit score. In other words, only apply for new credit if you need it.

- Having credit cards and installment loans is fine, as long as you make timely repayments.

- Make sure the credit agencies know about court judgments that you have resolved, i.e., to the satisfaction of the lender.

-

Time is your ally

Experian.com makes the following comment regarding improving your credit score:

“If you have negative information on your credit report, such as late payments, a public record item (e.g., bankruptcy) or too many inquiries, you may want to pay your bills and wait. Time is your ally in improving your credit scores. There is no quick fix for bad credit scores.”

“FICO Score” Usage

Below, you can see some sentences containing the term “FICO score,” illustrating how the term is used in context:

- “I checked my FICO score last week, and it’s higher than I expected, which is great news for the mortgage application I’m about to submit.”

- “When I started monitoring my FICO score, I became more conscious of my spending and credit habits.”

- “Many people don’t realize that their FICO scores can be affected by their credit card utilization rate.”

- “A common misconception is that checking your own FICO score will negatively impact it, but this is not the case with soft inquiries.”

- “Financial advisors suggest checking your FICO score annually to ensure there are no errors or fraudulent activities on your account.”

- “She was thrilled to see her FICO score had improved over the past year due to her diligent payment history and reduced debt levels.”

Two Educational Videos

These two interesting video presentations, from our sister YouTube channel – Marketing Business Network, explain what ‘FICO Score’ and ‘Credit Score’ are using simple, straightforward, and easy-to-understand language and examples.

-

What is a FICO Score?

-

What is a Credit Score?