The German economic machine has ground to a halt. The country is so dependent on exports and its economy is primarily driven by its sales to the rest of the world. So, when the world economy slows down, so does the German economy.

Some analysts say that Germany has created a false economy by cutting government and private sector investment.

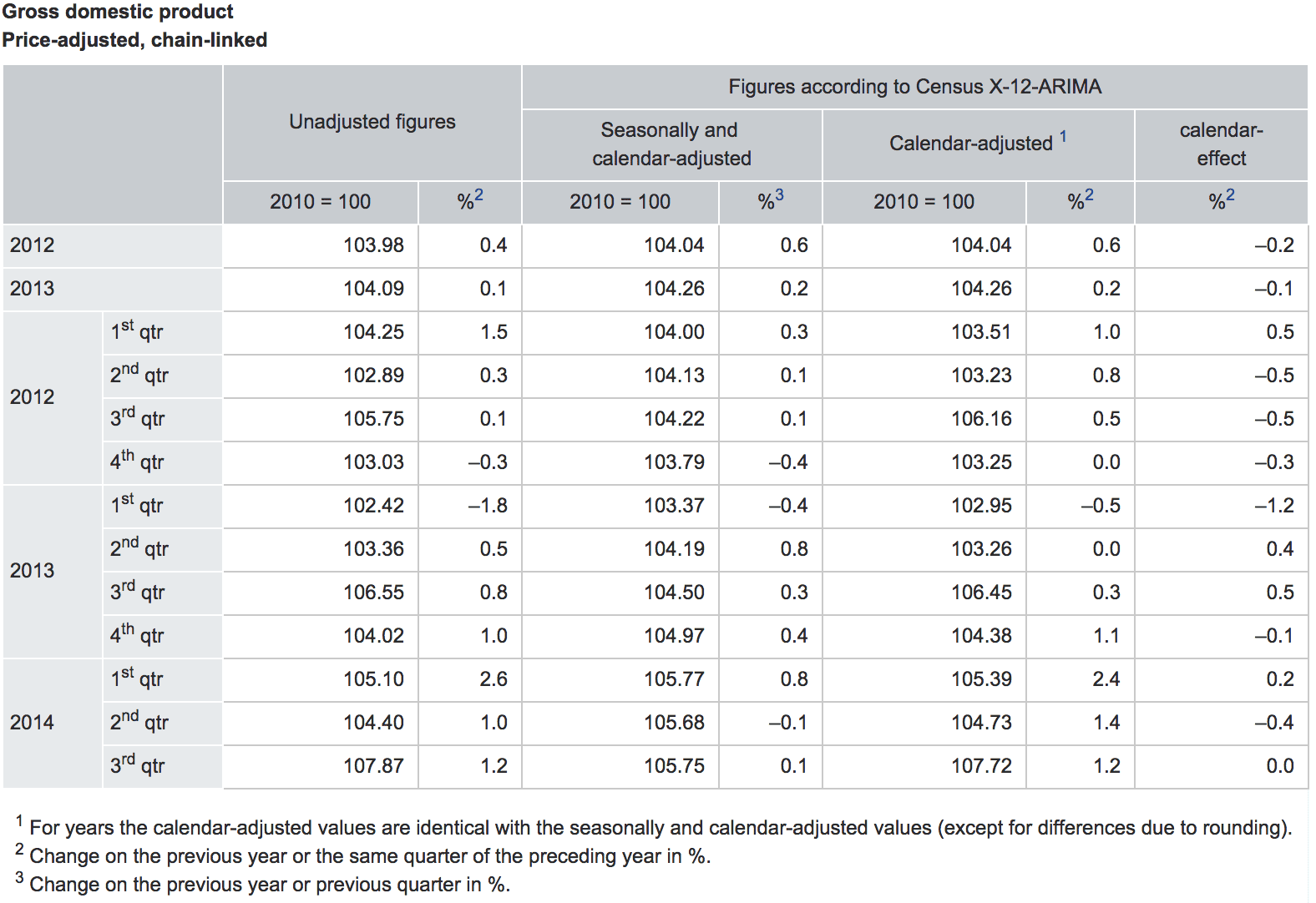

Germany is losing momentum, nearly falling into a triple-dip recession, growing by only 0.1% this quarter, with the impact of Russian sanctions and lack of business investment being the most cited reasons.

A press release issued by Statistisches Bundesamt, said:

“The German economy turned out to be stable in a difficult global economic environment. In the third quarter of 2014, the gross domestic product (GDP) rose 0.1% on the second quarter of 2014 after adjustment for price, seasonal and calendar variations; this is reported by the Federal Statistical Office (Destatis). According to the most recent calculations, the GDP had slightly decreased (–0.1%) in the second quarter of 2014 after the German economy had started the year with much momentum (+0.8% in the first quarter of 2014).”

The German government has plans in the pipeline, but it needs to act and encourage business investment, by making it easier to start a business, pay taxes, and opening up protected professions.

The eurozone grew by more than expected, but only by a modest 0.2% – beating expectations of 0.1% growth.

Other countries such as Poland (0.9%), Latvia (0.4%), Lithuania (0.4%) and Czech Republic (0.3%) showed positive growth, despite their significant exposures to the Russian economy.