Global economic outlook for the advanced economies remains uncertain, despite recent figures indicating stronger global industrial production, says DEPA (United Nations Department of Economic and Social Affairs).

The US has just managed to avoid a default crisis at the eleventh hour, but come the beginning of 2014 there is the threat of a repeat performance.

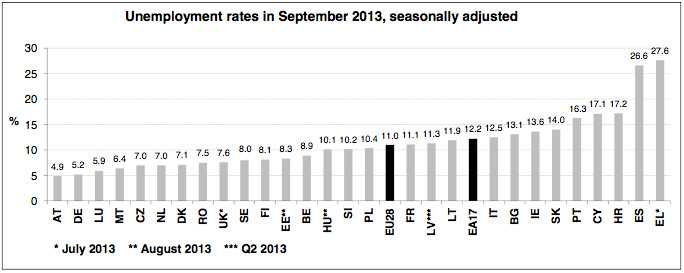

Although the US and Europe are seeing gains in GDP growth, they are not reflected in sizable reductions in unemployment rates. The systemic risks in the Eurozone have receded thanks to a number of policy measures.

Nevertheless, DEPA warns that significant banking and fiscal risks persist, and the southern members of the Eurozone have very fragile economies.

Several emerging economies are susceptible to external shocks “and face bottlenecks in their domestic economies”.

Japan, which seemed to have entered a hopeful period of economic recovery during the first half of this year, slowed down during the third quarter. The consumption tax scheduled for April next year may slow things down even more.

Tapering the stimulus programs that exist in several major economies will be the greatest challenge for monetary authorities in the advanced economies, as their consequences do not only affect them, but also the rest of the world.

Global economic outlook – the advanced economies

United States

The US Government was partially shut down for 16 days in October because lawmakers failed to agree on the federal budget. Hundreds of thousands of federal employees were laid off and several services were either not available or disrupted.

Racing against the clock, lawmakers managed to come to an agreement at the last minute – a temporary solution only.

The federal Government can operate until January 14th 2014 and to maneuver the debt up to February 7th, 2014.

The housing sector, which had been doing well has recently lost steam. Pending home sales dropped for four consecutive months. When the US Federal Reserve announced that it might start tapering the stimulus package, mortgage interest rates rose during the second quarter.

Japan

As from April 2014, consumption tax (sales tax, VAT) will rise from 5% to 8% while the country’s recovery remains fragile.

For the last 2 to 3 decades Japan’s economy has virtually stood still, partly because domestic demand has not picked up, despite several different measures taken by a range of administrations to boost consumer spending.

The government will introduce a stimulus package worth 5 trillion yen to counteract the negative consequences of the consumption tax hike.

Although international trade and industrial production have increased during the last few months, imports have been growing faster than exports, which aggravates the deficit in the balance of merchandise trade.

DEPA says the Japanese labor market has been slower than other segments of the economy. During the first few months of this year very few new jobs were created. September saw an improvement.

However, Japan has the lowest unemployment rate among the major advanced economies. Its seasonally adjusted employment level is now as it was before the March 2011 disasters, but wages are not increasing.

Western Europe

Recovery is underway, albeit a fragile one.

- Industry is growing.

- The retail trade is expanding.

- Consumer confidence is close to its long-term average.

- Confidence in the service sector and construction, however, is below average.

Although capacity utilization is below its long-term average, it is higher (78.4) than it has been recently.

The Markit Eurozone PMI Composite Output Index fell last month, partly due to a drop in services activity, but boosted by industrial activity growth. However, the index is above the neutral line (no expansion or contraction line).

Inflation continues to fall, the consumer price index rose just 1.1% (annualized) in September compared to 1.3% in August – this is well below the European Central Bank’s target of 2%.

Unemployment remains persistently high in the Eurozone, increasing to 12.2% in September. Europe faces the prospect of possibly years of jobless growth.

New European Union Members

Central European countries continued to enjoy improved consumer and business confidence, according to available indicators.

Domestic demand in Poland surged during the third quarter, after a previous quarter of growth. Retail sales volume rose by 3.9% while industrial activity grew by 6.2%, in both cases compared to the same quarter in 2012.

Third quarter growth in Lithuania slipped to 2.2% in the third quarter versus Q3 2012, compared to a 3.8% increase year-on-year in Q2 2013. The Baltic States are preparing the draft budget proposals for next year.

Croatia joined the EU in July 2013 and now has to adhere to the Stability and Growth Pact requirements. The Croatian government has presented a 3-year-fiscal-adjustment plan containing measures to boost revenue and cut spending.

As international liquidity levels are high and inflation is low, monetary easing will probably continue in the region.

The Hungarian National Bank and National Bank of Romania cut their policy rates to 3.4% (October) and 4.25% (September) respectively – record levels for both countries.

Global economic outlook by The Conference Board

The Conference Board sees a difficult 2014 for world economic growth, which it says this year will probably reach a “disappointing” 2.8%. It forecasts global GDP will grow by 3.1% in 2014.

Its global economic outlook for the next five years includes a prediction that growth will average 3.1% per year. During the period 2020-2025 growth might slow down to 2.4% annually “on the basis of the current trend”.

Bart van Ark, Chief Economist of The Conference Board, said:

“Growth in 2013 has fallen below even our cautious projections. Among mature economies, Europe’s worse-than-expected recession was compounded by self-inflicted damage in the U.S., culminating in the government shutdown. Meanwhile, growth in such emerging markets as India, Mexico, and Brazil saw even larger slowdowns than we anticipated.”

“The good news for 2014 and beyond is that the upside growth opportunities present themselves somewhat more clearly and may offset downsides, provided business and governments invest more heavily in the future of their economies and reform agendas are accelerated to reap the benefits from such investments.”

Mr van Ark added that the United States has enormous potential for private sector-driven growth. However, he is concerned about political brinkmanship which undermines the country’s ability to move forward and could become a major obstacle for growth. By postponing serious discussions and solutions on Social Security and Medicare, “current fiscal pressure tends to fall solely on discretionary spending such as infrastructure, education, and research – the very investments needed to spur future growth.”