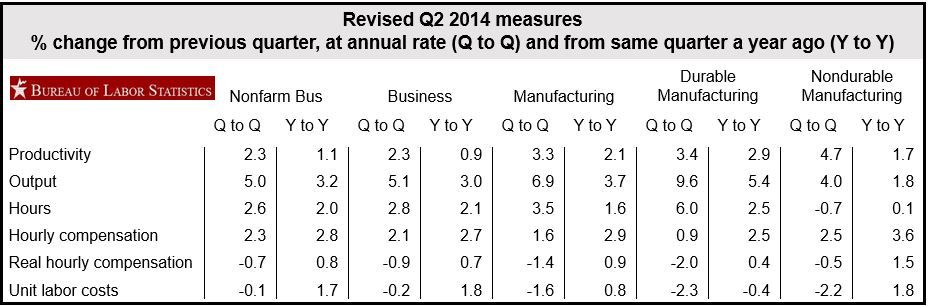

In the second quarter, US labor productivity improved by 2.3%, says the Bureau of Labor Statistics, part of the Department of Labor. Hours worked increased by 2.6% and output grew by 5%.

From Q2 2013 to Q2 2014 productivity grew by 1.2%, as hours worked and output increased by 2% and 3.2% respectively.

In the first quarter, productivity had fallen by 1.7%.

The Bureau calculates labor productivity by dividing real output by hours worked by all persons, including unpaid family workers, proprietors and employees.

Unit labor costs were 0.1% lower in Q2 2014, and rose by 1.7% over the last 12 months.

Improved productivity is a vital component for higher living standards. When productivity goes up, employers can pay more without having to raise prices, which can fuel inflation.

When unemployment fell to 6.1% in June there was a growing feeling that interest rates would rise earlier than expected. With lower-than-expected labor costs, the Federal Reserve has more reason to maintain its accommodative monetary policy stance for some time.

Manufacturing productivity

In the manufacturing sector, productivity rose by 3.3% in Q2 2014, as production increased by 6.9% and total hours worked rose by 3.5%.

The second quarter saw the largest increase since Q2 2010 (11.6%).

In the durable goods sector productivity rose by 3.4%, and increased by 4.7% in the non-durable goods sector.

Over the past 12 months, manufacturing productivity rose by 2.1%, with output rising 3.7% and total hours worked by 1.6%.

Manufacturing unit labor costs fell by 1.6% in Q2 2014, and rose by 0.8% compared to Q2 2013.

(Data source: US Bureau of Labor Statistics)

Non-financial corporate sector

Q2 2014 productivity in the non-financial corporate sector increased by 3.1%, with output and hours increased by 7.8% and 4.5% respectively.

Unit labor costs declined by 1.8%, with hourly pay gaining by 1.8% compared to a 3.1% rise in productivity.

Productivity since 2009

There was a sharp increase in productivity in 2009 and 2010, in the aftermath of the Great Recession. As demand took a nosedive companies trimmed output, but jobs came back rapidly, which drove up productivity as fewer workers produced more.

In 2009, productivity increased by 3.2% and then by 3.3% in 2010.

However, since 2011, productivity has only increased by an average of 0.7% annually – much lower than the United States’ historical average. Many economists started to wonder whether this was just a blip or a new long-term trend.