Productivity refers to the rate of output per unit of labor, capital or equipment (input). We can measure it in different ways. We can measure the productivity of a factory according to how long it takes to produce a specific good. In the services sector, on the other hand, where units of goods do not exist, it is harder to measure. Some service companies base their measurement on how much revenue each worker generates. They then divide that amount by their salary.

In a factory, you can measure productivity by dividing the total output by the number of workers. Imagine a table factory that employs 100 people producing 2000 tables per day. The productivity of each employee is:

2000 (tables) ÷ 100 (workers) = 20 tables per worker per day

Historically, we have used technology to boost productivity in the world of business and agriculture.

What is efficiency?

If we can increase output per worker from 20 to 30 tables per day, without increasing costs, the factory has improved efficiency. It will have lower unit costs. The lower unit costs will generate higher profits.

Although we often cite the two terms together. However, they do not have the same meaning.

Productivity focuses on getting the maximum production per worker or unit of machine per minute, hour, day, or week, etc. Efficiency, on the other hand, looks more at eliminating waste and maximizing quality.

Factors that determine productivity

It is the result of several factors, including the quality of machines available and workers’ skills. Speed of delivery and effective management are also important factors.

A company can improve output per worker by investing in better equipment, training its staff, and improving the management of workers.

Also, if workers know there is concern for their well-being, output per head can improve significantly. We call this the Hawthorne effect.

The company will be initially spending money in the short term if it aims to boost productivity. However, over the long term, it will be worth it when production per unit of input per day rises.

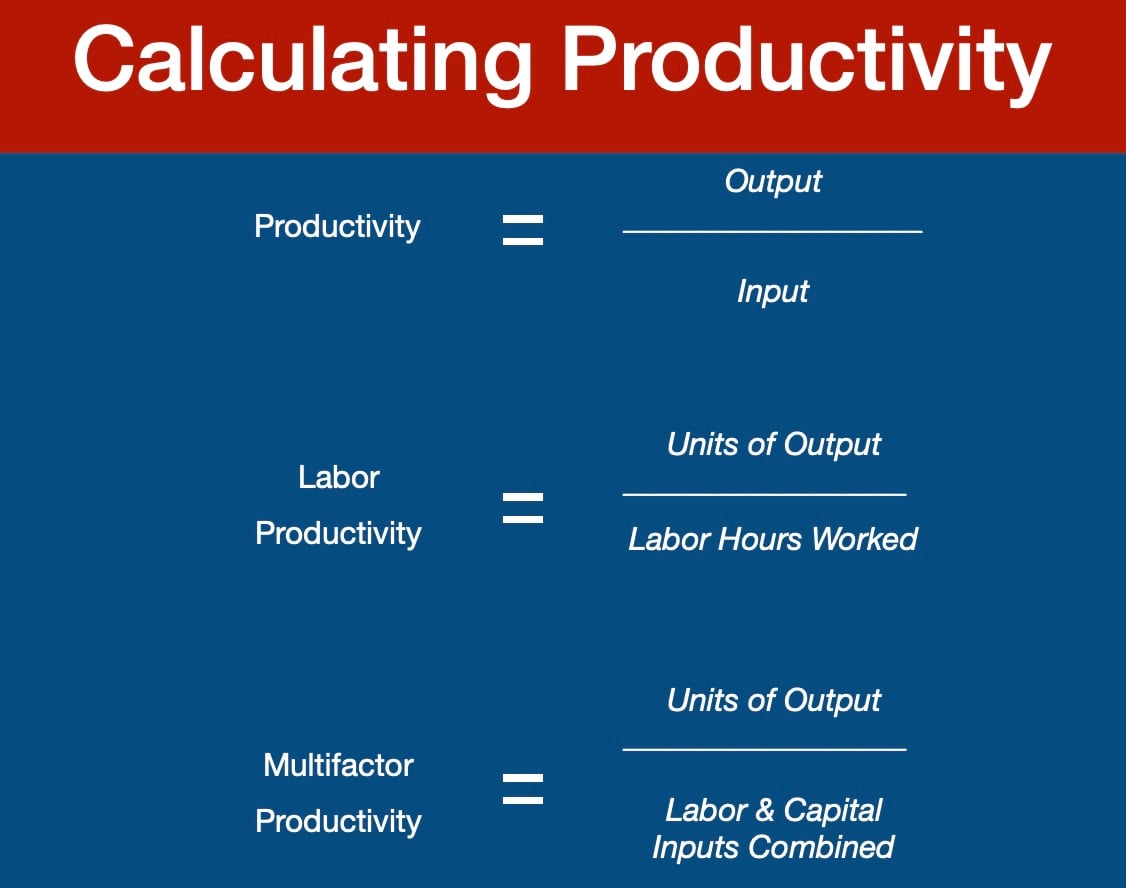

We can express productivity as the ratio of output to inputs we use in the process of production minus output per unit of *input.

* Input is something that we put into a system to achieve output. For example, power to drive a machine and the machines themselves are items of input. Input also includes the workers.

Idle time, time during which workers or machines are not producing, can significantly reduce a company’s rate of production.

Output value minus input value

The value of outputs minus the value of inputs is a measure of the income that a company generates. Specifically, the income it generates in the production process.

It is a measure of the production process’ total efficiency. Therefore, we try to maximize the production process.

Partial productivities are measurements that use one or more factors (inputs) of production, but not all factors. Labor productivity, which we usually express as output per hour, is a common example in economics.

At the company level, typical partial productivity levels include energy per unit of production and worker hours. We also include materials.

The approach in **macroeconomics is quite different. Macroeconomists want to examine an entity of several production processes. They sum up the value-added created in the single processes.

** Macroeconomics focuses on large-scale or general economic factors such as GDP growth, inflation, etc.

It is important when summing up all the factors that there is no doubling up of intermediate inputs. Value-added is obtained by subtracting the intermediate inputs from total outputs.

The most common measure of value-added is the gross domestic product (GDP). We commonly used it to measure the economic growth of industries and whole countries. GDP is the income available for paying labor compensation, capital costs, taxes, and profits.

For a single input, this means the ratio of value-added output to input. When we consider multiple inputs, such as capital and labor, it means the unaccounted-for level of output compared to the level of inputs.

In macroeconomics, we call this measure TFP (Total Factor Productivity) or MFP (Multi Factor Productivity).

Productivity is what matters

It is what really matters when looking at the production performance of nations and companies. When output per worker, for example, rises so do living standards.

Living standards rise because a greater level of real income improves individuals’ ability to buy goods and services.

With more income people, can enjoy better leisure, education, housing, and contribute to social and environmental programs.

In addition to individual benefits, high productivity levels can foster economic resilience, enabling societies to better withstand economic downturns and global challenges.

As far as businesses are concerned, greater output with the same inputs helps them become more profitable.

Advancements in technology and process optimization continue to be pivotal in driving productivity growth across all sectors of the economy.

Why is productivity important?

Productivity gains are crucial for an economy because they allow people to achieve more with less. It also allows them to achieve more with the same available resources.

Two vital resources in the production process are scarce – labor and capital. Therefore, maximizing their impact will always be a core concern of businesses.

Economists measure and track productivity because it provides an important clue to predicting future GDP growth levels.

Publishing data

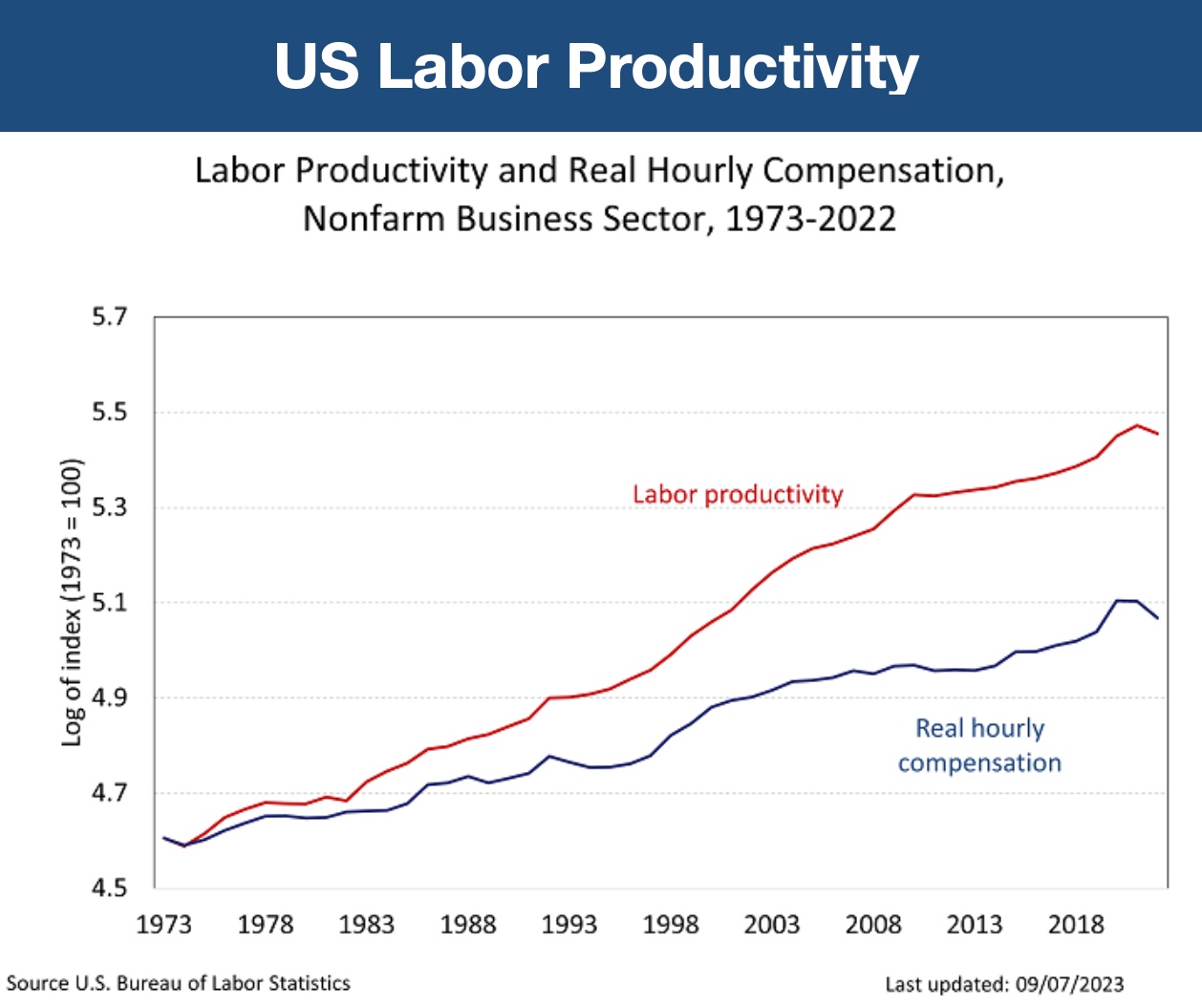

When the media report on the productivity measure of a nation, they are invariably talking about the ratio of GDP to total hours worked across the whole country during a specific period. In the United States, the Bureau of Labor Statistics publishes this measure every quarter.

The UK’s Office for National Statistics reports on a range of measures, including output per job and output per worker. It also reports on output per hour for the whole economy and a range of businesses, and the public sector. There are international comparisons across the G7 nations.

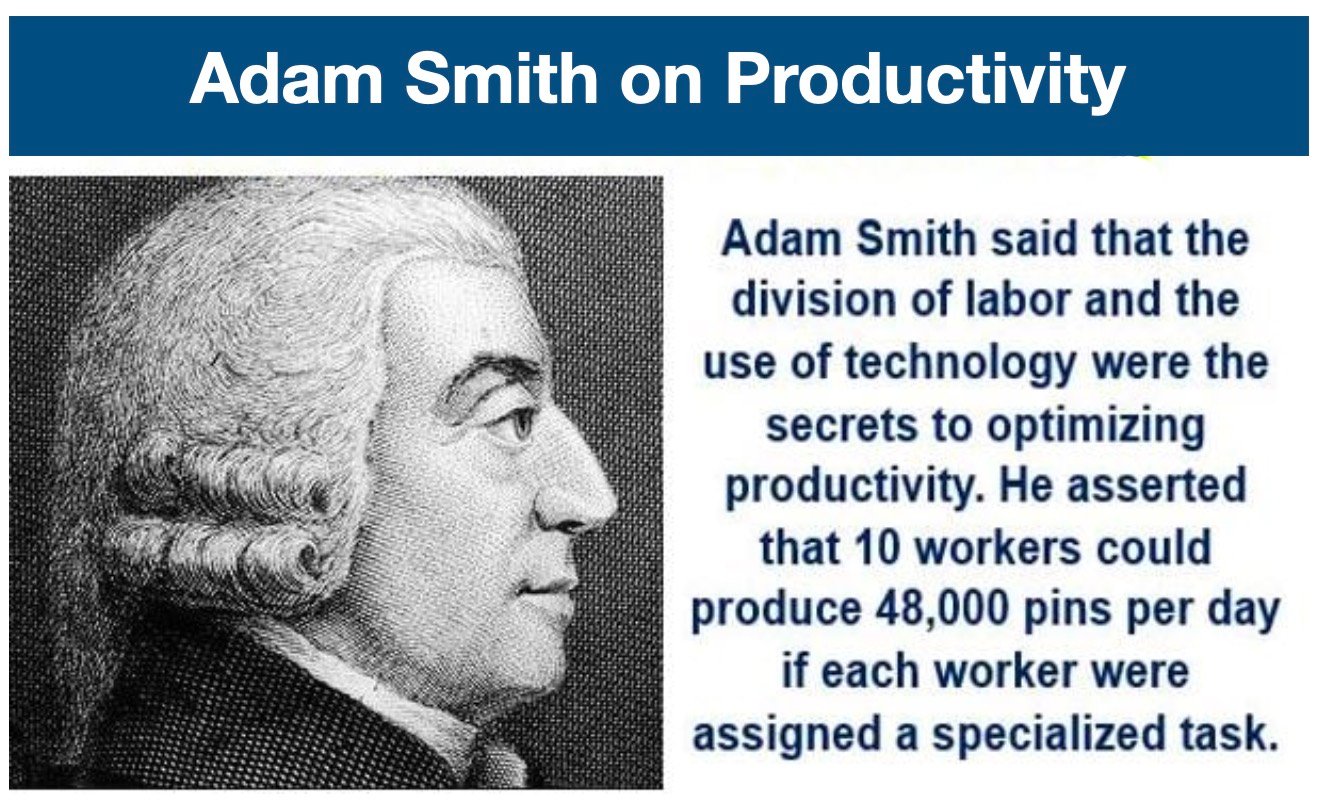

Adam Smith (1723-1790) was a Scottish pioneer of political economy and a moral philosopher. In fact, economists say he was the ‘father of modern economics.’ In several of his works, he wrote about productivity. He also wrote about how the division of labor was crucial in getting more production out of limited inputs. (Image: adamsmith.org)

Labor productivity and costs

According to the US Bureau of Labor Statistics, labor productivity “relates to output to the labor hours used in the production of that output.”

Two Bureau of Labor Statistics programs produce LPC (labor productivity and costs) measures for sectors of the United States’ economy:

– The Major Sector Productivity program: published annually and quarterly. It includes measures of output per hour and unit labor costs for the US business. It covers non-farm business as well as manufacturing sectors. These are the figures that the national media most commonly refer to.

– The Industry Productivity program publishes annual measures of production per hour and unit labor costs for US industries.

The Multifactor Productivity homepage contains output regarding combinations of inputs.

Regarding how they measure it, the US Bureau of Labor Statistics says:

“Productivity is measured by comparing the amount of goods and services produced with the inputs which were used in production. Labor productivity is the ratio of the output of goods and services to the labor hours devoted to the production of that output.”

What are unit labor costs?

We calculate unit labor costs by dividing total labor compensation by real output. We can also calculate it by dividing hourly compensation by productivity. In other words:

Unit Labor Costs = Total Labor Compensation ÷ Real Output

or

Unit Labor Cost = Hourly compensation ÷ productivity = [total labor compensation ÷ hours] ÷ [output / hours]

Therefore, increases in productivity reduce unit labor costs. On the other hand, compensation increases raise labor costs. If both of them move equally, unit labor costs remain the same.

There is a growing tendency globally to increase productivity while reducing damage to the environment at the same time. Companies that pursue this are adopting a management philosophy we call eco-efficiency.