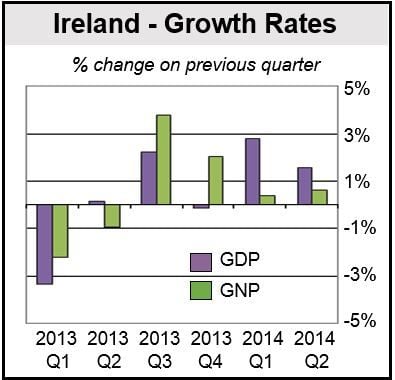

The Irish economic boom is back. The Republic of Ireland posted 1.5% GDP growth for the second quarter of 2014 compared to the previous quarter, and 7.7% up from Q2 2013.

The second quarter growth is the strongest posted in Ireland since the early 2000s. Figures show the country is pulling away from the rest of the Eurozone, which saw GDP flatline in Q2.

Ireland’s Central Statistics Office wrote today:

“Preliminary estimates for the second quarter of 2014 indicate that GDP increased by 1.5 per cent in volume terms on a seasonally adjusted basis compared with the first quarter of 2014 while GNP increased by 0.6 per cent over the same period.” (GNP is everything produced by nationals at home, abroad, plus that country’s companies globally)

Ireland’s government has revised its growth forecasts for the second time in seven days, from 2.1% to 3%, and now to 4.5% for 2014.

Ireland’s Finance Minister, Michael Noonan, said his country’s economy is now in a “catch-up phase” following a devastating recession.

Mr. Noonan said:

“My people advising me tell me that it’s a trend that will continue. We’ll be marking up the growth figures for 2014 and 2015. It’ll settle around 4.5pc in GDP for 2014. We haven’t run the numbers yet, but it will be somewhere around there. Bit less for next year.”

Ireland, along with Portugal, Spain and Greece, was severely damaged during the Great Recession, when unemployment shot up and the housing market crashed.

(Data source: Central Statistics Office)

(Data source: Central Statistics Office)

From boom to bust back to boom

The Irish economy boomed during the first few years of this millennium, followed by a big bust when the global crisis hit, and today the boom is back – the country has turned the full circle.

Now that the economy is racing forward again, Mr. Noonan predicts that the budget deficit will drop to approximately 3.5% of GDP by the end of this year, well below the 4.8% target.

Achieving the deficit target means the planned €2 billion in tax increases plus spending cuts for 2015 are no longer required. Ireland must bring its deficit down to 3% of GDP by the end of 2015.

Regarding the deficit, Mr. Noonan said:

“The figures are due to the policies pursued by Government for the last three years and the sacrifices made by the Irish people. It shows that sticking to the policies is now bearing fruit.”

The Central Statistics Office informed that Industry (incl. building and construction) grew by 4.7% in volume terms in Q2 2014 from the previous quarter. Distribution, software, transport and communication rose by 2.9% over the same period, while Other Services dropped by 0.8%. Defense and Public Administration declined by 0.5%.

Businesses ask for tax cuts

IBEC, the group that represents Irish business, urged the government to introduce tax cuts, now that the economy is growing strongly again. Although Ireland now has the fastest-growing economy in the EU, the wider European economy is still fragile. “Europe is not out of the woods yet and risks remain,” it warned.

Fergal O’Brien, IBEC’s Head of Policy and Chief Economist, said:

“A broad based recovery has firmly taken hold. The economy is re-balancing with domestic demand and net exports contributing to stronger growth. Investment is up 18.5% and personal consumption is up 1.8%, but more can be done to improve this by reducing income and consumer taxes. This would support job creation and ultimately lead to a more stable economy.”