The Bank of England (BoE) has several options to address the Brexit quake – which has triggered a plunging pound sterling, a raft of negative business and economic data, and a serious loss of confidence that has emerged since 23rd June, when Britons voted to leave the European Union.

The BoE can:

– reduce interest rates.

– purchase more government debt.

– cut interest rates plus purchase government debt.

– come up with something totally original that nobody could have expected.

– sit on its hands, do nothing, and attempt a bit of watchful waiting.

If Martin Weale, the ultra-anti-rate-cut MPC member hinted that the bank rate might go down, then it most definitely will, analysts say. (Image: twitter.com/montysblog)

If Martin Weale, the ultra-anti-rate-cut MPC member hinted that the bank rate might go down, then it most definitely will, analysts say. (Image: twitter.com/montysblog)

Most bets are on a definite reduction in interest rates, and a likely purchase of government debt. Reducing interest rates will set the pound sterling – which has already declined by over 11% since the Brexit vote – falling further still.

The term Brexit is a blend of two words – Britain and Exit. It means the UK leaving the European Union.

Everybody warned that voting to leave the EU would hurt the pound. Even George Soros, the Hungarian-American business magnate who made a $1 billion profit in 1992 during the Black Wednesday UK currency crisis, warned that Brexit would result in a 15% devaluation of the pound by the end of 2016.

Leave campaigners accused the Remain camp and their allies of scaremongering and assured the electorate that nothing of the kind would occur if they opted for Brexit. It has become evidently clear that they were wrong – either they had no idea what they were talking about or they simply lied.

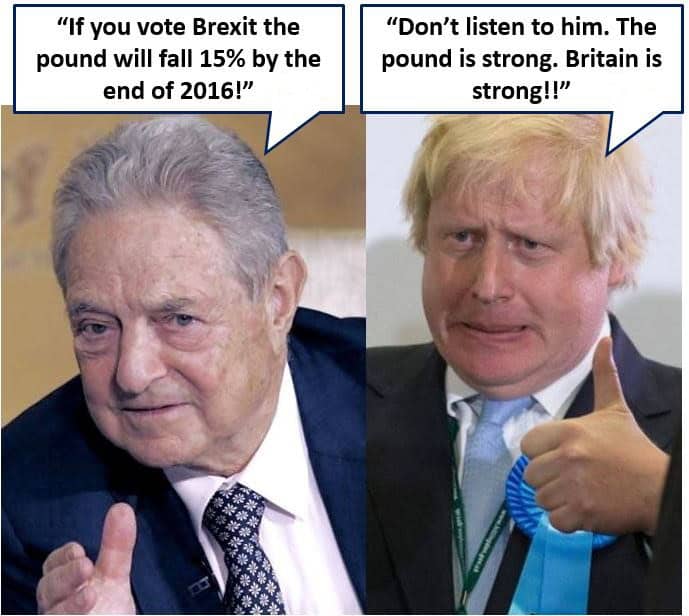

George Soros and dozens of other business leaders warned that Brexit would be bad for the pound. Boris Johnson said they were scaremongers and that the pound was strong and would be fine. Mr. Johnson was clearly completely wrong. (Image: georgesoros.com)

George Soros and dozens of other business leaders warned that Brexit would be bad for the pound. Boris Johnson said they were scaremongers and that the pound was strong and would be fine. Mr. Johnson was clearly completely wrong. (Image: georgesoros.com)

Britain’s outlook is bleak

Economic and business data has started to emerge since the referendum – most of it points to a bleak future for the UK’s economy; at least over the short term. All signs warn of a significant slowdown in GDP (gross domestic product) growth, and even the possibility of a looming recession.

The Bank of England is aware of these signs that warn of bad things to come, and knows it is expected to address the threat. Virtually all economists, investors, bankers and analysts in London are certain that the central bank will at least reduce interest rates, and will probably also start buying government debt.

When a central bank moves interest rates, it usually has an effect on both the value of the country’s currency as well as share prices.

When rates go down, the currency slides too, especially if economic indicators don’t look good. Falling interest rates are generally followed by an increase in the stock market – investors move their money from bank accounts and financial instruments, which are earning less, into more productive things, including shares.

When interest rates rise the opposite tends to happen, the currency appreciates and the stock market goes down (not always).

Andy Haldane said: “I would rather run the risk of taking a sledgehammer to crack a nut than taking a miniature rock hammer to tunnel my way out of prison – like another Andy, the one in the Shawshank Redemption. And yes I know Andy did eventually escape. But it did take him 20 years. The MPC does not have that same ‘luxury’.” (Image: bankofengland.co.uk)

Andy Haldane said: “I would rather run the risk of taking a sledgehammer to crack a nut than taking a miniature rock hammer to tunnel my way out of prison – like another Andy, the one in the Shawshank Redemption. And yes I know Andy did eventually escape. But it did take him 20 years. The MPC does not have that same ‘luxury’.” (Image: bankofengland.co.uk)

MPC meets next week

Interest rates in the UK are determined by the Bank of England Monetary Policy Committee (MPC), which consists of nine experts who meet twelve times a year. Their next meeting is on 4th August.

Bloomberg asked 46 economists to predict what will happen. Forty-four forecast that the MPC would vote to cut rates, while only two said it wouldn’t.

At 0.5%, the current bank rate is at a record low. Most bets are on a 25-basis point cut, i.e. reducing the 0.5% to 0.25%.

Even Dr. Martin Robert Weale CBE, an MPC member and director at the National Institute of Economic and Social Research – known as the Committee’s hawk – has gone dovish. Experts say that if Dr. Weale has gone soft, then a cut in interest rates is no longer a probability – it is a definite certainty. Swaps signaled a 100% probability of a rate cut next week.

Bank of England rewriting script

All the signs are that the vote to leave the EU has let to a total rewrite of the Bank of England’s script. Had Britons voted to remain, the Old Lady of Threadneedle Street (BoE) would have been doing everything the other way – preparing to raise interest rates in order to control a rising pound.

The central bank is now tasked with shoring up confidence and growth in an all-action move. We are all on the edge of our seats – anticipation ahead of the MCP’s next meeting has rarely been higher. The Bank of England cannot afford to underwhelm markets like the Bank of Japan did on Friday.

It had been a near certainty that the Bank rate would never go below 0.5%, where it has remained ever since early 2009, when the country’s economy, and much of the rest of the world, was in a deep recession. After the Brexit vote all gloves are off – there is now an expected rate cut to 0.25%.

MPC member, Andy Haldane, BoE’s chief economist, has talked of the need for a ‘sledgehammer’, suggesting that just reducing interest rates is unlikely to be enough. So, what else can it do?

– It could reduce rates even further, perhaps right down to 0.1%.

– It could use forward guidance, telling everybody that super-low rates are here to stay for a very long time.

– It could purchase more government debt (quantitative easing), adding to the £375 billion of bonds it purchased between 2009 and 2012.

– The BoE could widen the quantitative easing programme to include corporate bonds.

– Its Funding for Lending programme could be expanded.

– There is a chance it might come up with something completely original – totally unexpected. Sometimes taking the audience by surprise has benefits.

Markit PMI falls dramatically

The Markit PMI (Purchasing Manager’s Index), a strong indicator of the state of the economy, has declined considerably since the Brexit vote. It fell to 47.7 points in July, its lowest level since 2009.

The PMI figure suggests that the manufacturing and services sectors, i.e. business activity, is contracting and is likely to shrink in the months to come.

The PMI is based on five key indicators – supplier deliveries, the environment for jobs, new orders, production and inventory levels.

Any PMI reading above fifty points suggests that business activity is doing well (expanding), while a reading below 50 means that it is contracting.

The PMI figures for July show that both the service and manufacturing sectors have experienced a decline in orders and output.

British consumers losing confidence

British consumers are losing confidence, says the latest GfK Consumer Confidence Index, which showed a steep decline of 11 points.

Immediately after the Brexit vote, consumer confidence nosedived, and then continued sliding slowly during the whole of July.

GfK says that UK consumers are very worried about the future of the economy, their personal finance, and employment status.

Reuters quoted Chris Turner, a currency strategist at ING, who said:

“All the confidence surveys have been dire, but they’ve already been priced in. So we need something new now, and that is probably the Bank of England response,” said ING currency strategist Chris Turner.”

“We think they will go large and early, and sterling will weaken to $1.27-1.28 towards the end of next week on the back of that.”

Mr. Turner predicts a 25-basis point rate cut, as well as a fresh round of government debt purchases.

In an interview with Stock News US, Neil Jones, head of hedge-fund sales at Mizuho Bank, said that the BoE will probably need to do more than what the market is predicting, to really have an affect on the market. He believes there might be a 50-basis-point cut (from 0.5% to 0.0%), plus the purchase of about 50 billion of government debt.

Mr. Jones thinks that such an aggressive move would take the market beyond the expected result and provide the ingredients for a strong boost to the economy. He cautioned, however, that this would be in the ‘upper limits’ of what is expected.

Video – Brexit not good move for UK

In this Fox Business video, Greg Fleming, who used to be President of Wealth Management at Morgan Stanley, explains why chosing to leave the EU was a bad move for the UK long-term. (One of the presenters makes an error when he says “with Britain voting to leave the UK..” he should have said “with Britain voting to leave the EU”).