Cash accounting is a bookkeeping system. In the system, you only enter payments going out and coming in when they occur, rather than when people place the orders. With accrual accounting, on the other hand, income is recorded when a company earns the revenue (e.g., the product or service is delivered, fulfilling the performance obligation), and expenses are recorded when they are incurred (when the cost is owed or the service/goods are received), regardless of when the payment actually occurs.

Small enterprises tend to use cash accounting. They prefer it because it is straightforward and easy to understand. However, it can sometimes make profits appear to fluctuate wildly when, in fact, they are not.

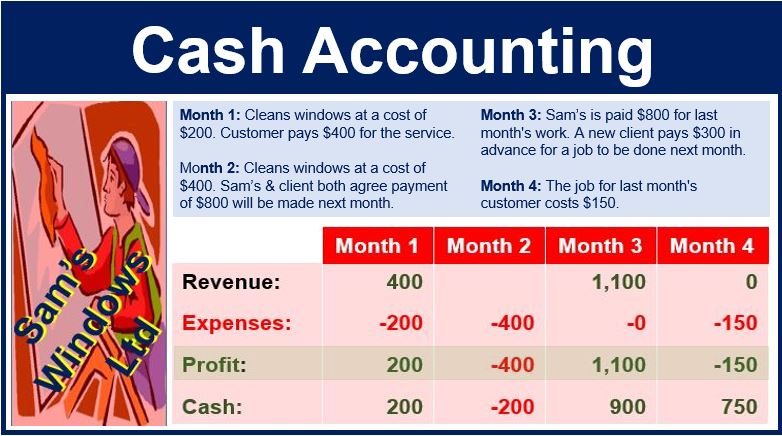

With the cash accounting method, Sam’s Windows Ltd’s 3rd month was its best. However, he did not do any work in that month. The method can make profits appear to fluctuate sharply.

Large companies have to comply with Generally Accepted Accounting Principles (GAAP). In other words, large corporations must use the accrual accounting method. Small businesses under certain revenue thresholds (varying by jurisdiction) might choose the cash method for simplicity. However, some countries require any business with inventory or exceeding specific annual revenue limits to use accrual accounting.

Cash accounting vs. accrual accounting

Accrual accounting also follows what is known as the ‘matching principle.’ This means that expenses are matched to the revenue they help generate in the same accounting period, giving a more accurate picture of a company’s financial performance.

Imagine Mowers Ltd. receives an order for ten lawn mowers from ZZZ Golf Club. The lawn mowers sold at $100 each (total $1,000). The company got the order on January 5th and received payment on February 5th.

In a cash accounting system, the bookkeeper would record the sale as having occurred on February 5th. However, in an accrual accounting system, the bookkeeper would make the entry for January 5th.

In some cases, customers may pay a deposit or partial payment before the goods are delivered. Under accrual accounting, the business typically recognizes revenue for the portion of the work completed (or goods delivered) and records any unearned portion as a liability (known as ‘unearned revenue’ or ‘deferred revenue’

Let’s suppose Technicians Forever sent an expert down for the day to service all Mower Ltd’s machinery on January 1st. Mowers Ltd. paid the invoice of $300 for this service on February 1st. The bookkeeper would register the expense as having occurred on February 1st using the cash accounting method. With the accrual accounting method, however, the entry would be for January 1st.

Cash accounting – disadvantages

Sometimes a business may seem more cash rich than it really is.

Imagine that several payments are due on April 3rd. The company may seem overly cash rich when presenting its first quarter accounts.

It had not paid the invoices it received during that quarter for orders it had placed in that quarter. Therefore, it would appear that the company has loads of money.

In an accrual accounting system, the bookkeeper would have entered those deductions already in the first quarter.

Conversely, the company that used the cash accounting method would appear worse off than it was. Especially if it had landed a giant order and the customer had not paid for it yet.

What would happen if it paid its bills on time, but the client was late? The company’s expenses to meet the large order would appear on the books, but not the large receipt.

Because cash accounting can misrepresent short-term profitability or liquidity, businesses that need loans or investors may find it hard to present a stable financial track record without accrual-based statements. Lenders and investors typically prefer accrual-based financials because they offer a more realistic snapshot of a company’s ongoing business.