The term Cost has several meanings. In accounting, retail, research, and production, it is the value of money that we use up to create something. That money is therefore not available for use anymore.

The term, in business, may refer to the amount of money spent to acquire something. In such cases, it is the input that has gone into acquiring the thing.

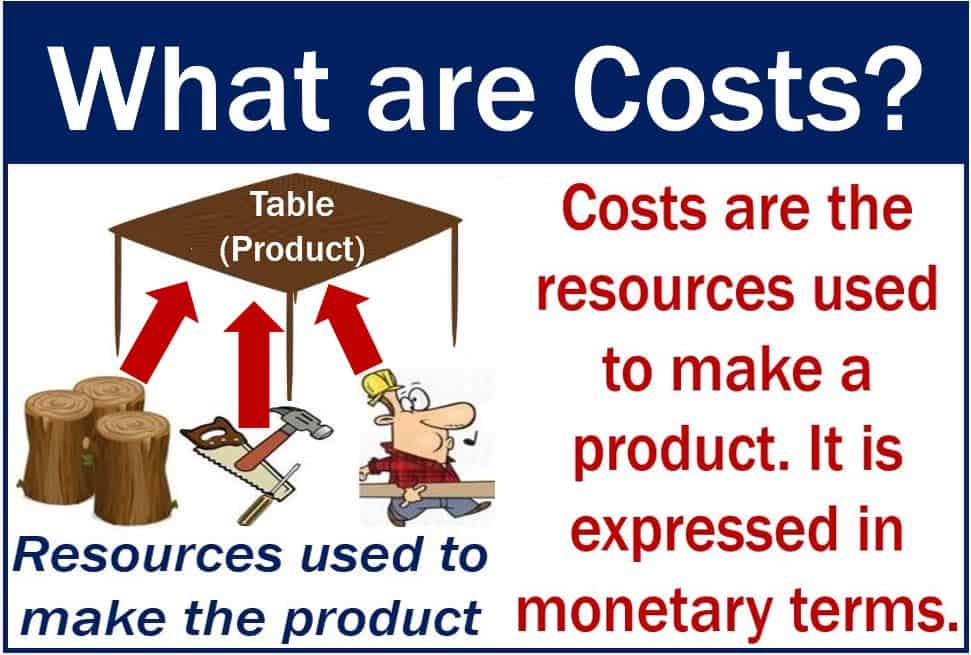

Put simply; ‘cost’ is the amount that we must give up or pay to get something.

In business, we typically give cost a monetary value to represent the following:

- the effort we made

- what material we used

- which resources we applied

- how much time and what utilities we consumed

- the risks we incurred

- other opportunities we had to forgo

Costs denote how much money a company spends on the production or creation of goods or services. It does not include profit or markup. Markup is the difference between the wholesale and retail price.

For sellers, costs are how much money they spend producing a good. If they sold their products at the price of production, their costs and income would be the same. In other words, they would break even – they would neither make a profit nor a loss.

For buyers, a product’s cost is also the price. It is the amount the seller charges them for a product. It includes the production costs as well as the markup, which the seller adds to make a profit.

Costs in accounting

In accounting, ‘costs’ refers to the monetary value of spending on equipment, supplies, and raw materials. It also refers to how much the company spends on labor, products, and services.

Accountants post the amounts as expenses in bookkeeping records. Bookkeeping involves recording a company’s day-to-day financial transactions.

Cost vs. Price

The two terms do not have the same meaning. Cost is the expense a company incurs in creating a product. It also includes how much the company spent bringing the product to the market.

The price, on the other hand, is the amount the customer pays for it. In other words, how much it sold it for.

The difference between a product’s cost and price is the profit a business makes. We call this the product’s markup or margin.

For example, imagine you buy an item for $25. It cost the vendor $10 to create and bring it to the market. The vendor subsequently makes a $15 profit.

Types of costs

There are several different types of costs for a commercial enterprise, the most relevant ones are:

-

Variable costs

These costs vary, depending on levels of business activity. They come about as a result of shipping, ordering, and handling raw materials.

When it comes to producing and delivering goods, variable costs have the most financial impact on a commercial enterprise.

-

Direct Costs

We can trace direct costs directly to the production of specific products.

Depreciation, administrative, and other costs are more difficult to assign to a specific product. Therefore, we consider them as indirect costs.

We also need to take indirect costs into account in the final markup stages of the product. They include the amount of time and effort put into creating it.

Manufacturing vs. non-manufacturing costs

-

Manufacturing Costs

These are directly involved in the manufacturing of goods. Examples include the costs of workers and raw materials. We divide manufacturing costs into three broad categories:

– Manufacturing overhead costs.

– Direct labor costs.

– Direct materials costs.

-

Non-manufacturing Costs

Non-manufacturing costs are not directly incurred in manufacturing a product. For example, advertising expenses are non-manufacturing costs. The salaries of sales personnel are also non-manufacturing costs.

We classify these types of costs into two categories:

– Administrative costs.

– Selling and distribution costs.

Cost estimation

When creating a business plan for a business, product, or project, planners usually make cost estimates. They make cost estimates to determine whether the subsequent revenues will cover costs. In other words, they need to know whether it is worth it.

Both governments and businesses do this. It is common for people to underestimate costs. Total spending ends up being considerably greater than the original estimate.

If costs are higher than income, the company will lose money. In fact, if people do not cost things properly, their company could go bankrupt.

List of meanings and examples

Below is a list of different meanings of the word ‘cost’ and examples of the term used in a sentence:

- Require the payment of: as in “The journey cost me $1,000.”

- Cause the loss of: as in “Driving under the influence of alcohol cost him his driving license.”

- To be expensive: as in “If you want your own space it will cost you.”

- Estimate the price: as in “My job is to cost each media campaign and get the estimate approved by management before it goes ahead.”

- An amount that needs to be paid or spent: as in “The bride and groom’s parents were broke, so his uncle covered the cost of the wedding.”

- Sacrifice, loss, or effort needed to obtain or achieve something: as in “The President managed to divert resources away from the issue at considerable cost to his popularity.”

- Court and legal expenses: as in “She had to pay a $10,000 fine plus $2,000 in court costs.”

Menu Costs

‘Menu costs’ are the costs that companies have to face when they change the prices of their goods.

If you raise or lower your prices, you need to redesign your price lists and catalogs. You also need to print new ones. Then you have to re-tag goods on shelves. In some cases, you must pay price consultants.

A comprehensive grasp of cost structures is fundamental for businesses to strategically price their products in a competitive market and ensure long-term sustainability.

Derivatives of the root word “cost”

Below are some derivatives of “cost,” plus their meanings, and an example of how each one is used in a sentence:

-

Cost (verb)

To require the payment of a specified amount of money.

Example: “The new building cost a fortune to construct.”

-

Cost (noun)

The amount of money required to purchase, maintain, produce, or do something.

Example: “The cost of the ticket was fifty dollars.”

-

Costly (adjective)

Expensive or high-priced.

Example: “The jewelry was so costly that few could afford it.”

-

Costliness (noun)

The state of being high in price.

Example: “The costliness of the project made the investors hesitant.”

-

Costless (adjective)

Without cost; free.

Example: “They offered costless delivery with every purchase.”

-

Uncostly (adjective)

Not costly; inexpensive.

Example: “The uncostly repairs were a relief to my budget.”

-

Costing (verb, present participle)

Estimating the price of something.

Example: “The accountant is costing out the new project.”

-

Recost (verb)

To calculate the cost of something again.

Example: “We need to recost the budget after the financial changes.”

-

Outcost (verb)

To exceed in cost.

Example: “The new proposal will outcost all previous ones.”

Video – What is a cost?

In this visual guide presented by our affiliate channel, Marketing Business Network on YouTube, we explain what “Cost” is using straightforward language and easy-to-understand examples.