With a Discount Loan, the lender calculates the interest and other related charges and discounts them from the face amount before lending to the borrower. However, the borrower has to pay back the whole amount – the principal, the related charges, and the interest.

Interest is what the borrower has to pay on top of the principal when he or she takes out a loan. The principal is the original amount of a loan, i.e., the amount before interest and bank charges (administration fees) are added to the total.

Discount loans are typically issued for people who seek a short-term loan.

For the schedule of payments, the lender divides the total by the number of months the arrangement will last. However, in the vast majority of cases, the loan is paid back in one lump sum.

Example of a discount loan

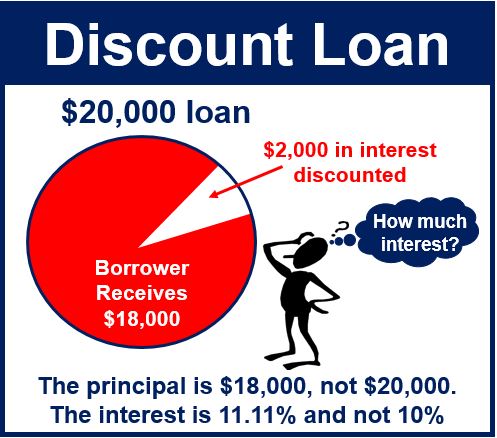

Imagine you wanted to borrow $20,000 and pay back twelve months later. The interest and charges came to $2,000.You would receive $18,000 from the lender. However, you would still have to pay back the whole $20,000.

Interest rates on discount loans tend to be higher than those on other types of loans.

The elevated interest rates on discount loans often reflect the increased risk assumed by lenders, as these loans are usually unsecured and based on the borrower’s creditworthiness.

This type of financing arrangement can be particularly attractive for lenders looking to secure immediate returns on the loans they offer.