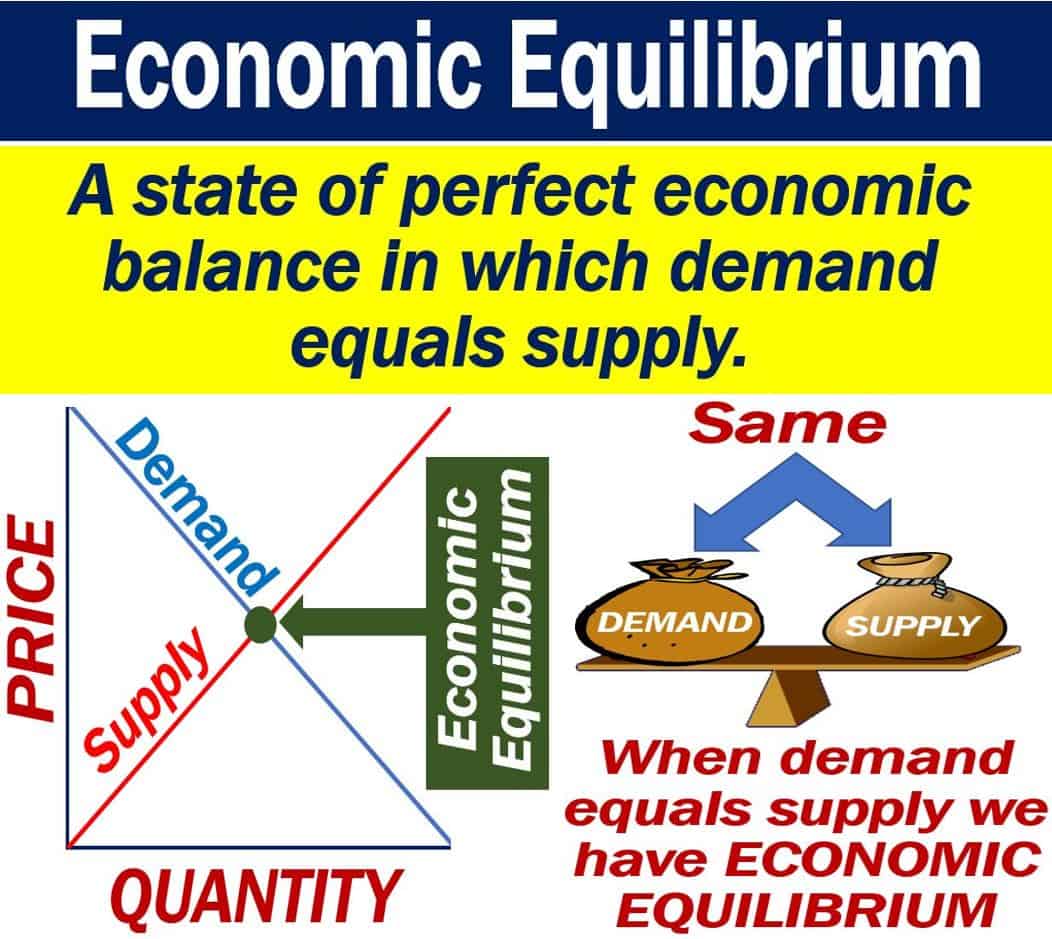

Economic Equilibrium is a state in which economic forces, i.e., market forces, are in perfect balance. It is a state of balance and serenity in economic conditions when no outside forces are causing disruption. People often use the term ‘equilibrium‘ with the same meaning.

In this context, ‘market forces’ refers to the forces of supply and demand. The forces of supply and demand determine the price of goods. When demand grows faster than supply, prices rise. When supply rises faster than demand, prices drop. If you push up prices, demand drops, and if you reduce prices, demand rises.

Economists often use the terms ‘general equilibrium‘ or ‘Walrasian general equilibrium‘ with the same meaning as economic equilibrium.

When supply equals demand

Economists also define economic equilibrium as the point at which the supply and demand of a single product are identical. The equilibrium price, therefore, exists where the hypothetical demand and supply curves meet.

Economics Online has the following definition of the term:

“Equilibrium is a state of balance in an economy, and can be applied in a number of contexts. In micro-economics, market equilibrium price is the price that equates demand and supply.”

“In macro-economics, national income is in equilibrium when aggregate demand (AD) equals aggregate supply (AS).”

Macroeconomics is a branch of economics that examines large-scale economic factors, such as GDP, interest rates, or inflation. Unemployment is also a macroeconomic factor. Macroeconomics contrasts with microeconomics, which focuses on the behavior of individual companies, households, and markets.

Economic equilibrium – many variables

We can talk about economic equilibrium at product, industry, market, or national level, i.e., the whole economy level. In other words, at microeconomic or macroeconomic levels.

We can apply it to variables that affect banking and finance, unemployment, or even international trade. In fact, we can observe it in any part of the economy where entities buy and sell things.

When a country has achieved perfect equilibrium, supply and demand are equal. This is also the standard textbook description of perfect competition.

When demand is not the same as supply, we say that there is economic disequilibrium.

Economic equilibrium – example

Let’s imagine we are in Littleland, a tiny fictitious country of just 2,000 people. We are standing in its main market square. It is the only place in Littleland where you can buy and sell groceries.

Potato sellers price a bag of potatoes at $5. However, nobody comes and buys any bags of potatoes. Therefore, demand is way below supply. There is economic disequilibrium.

The sellers subsequently reduce their price to $1 per bag. They all sell within minutes. Even after all the potatoes have gone, people continue coming wanting to buy potatoes. Now demand is way above supply. In this scenario, there is also economic disequilibrium.

On the next day, the potato sellers price a bag at $2.50. The bags sell little by little as the day progresses. By 4.50pm, ten minutes before market closing time, they sell their last bag. It appears that demand is about equal to supply. Now, we have economic equilibrium.

-

Perfect competition

Proponents of a free-market system say that economic equilibrium is only possible if there is perfect competition.

Perfect competition exists when there are many purchasers and sellers. None of them can individually influence prices or access to supply because there are so many of them.

They all seek to maximize their income and are free to enter or leave the marketplace.

In this context, the word ‘marketplace‘ means the same as ‘market‘ in its abstract sense.

Understanding “Economic Equilibrium” Across Different Scenarios

The term “economic equilibrium” can be applied to various scales and scenarios, from microeconomic transactions to global markets. Here are seven sentences that demonstrate the diverse usage of the term in different economic contexts:

- “The agricultural market reached an economic equilibrium when the supply of produce met consumer demand, stabilizing prices for the season.”

- “After the central bank’s intervention, the foreign exchange market returned to a state of economic equilibrium, easing the volatility of currency values.”

- “In the housing market, economic equilibrium is achieved when the number of properties for sale is equal to the quantity that buyers are willing to purchase.”

- “The concept of economic equilibrium is critical in environmental economics when assessing the sustainable extraction rates of natural resources.”

- “Economic equilibrium in the labor market is influenced by the minimum wage, which can set a floor for salaries if it’s above the equilibrium wage rate.”

- “Tech startups often disrupt economic equilibrium in traditional markets by introducing innovative products that change consumer behavior and demand patterns.”

- “During the economic equilibrium of the automotive industry, manufacturers adjust production levels to prevent excess inventory and maintain stable prices.”