General Equilibrium in economics is a perfect state when demand and supply are equal to each other. In other words, supply and demand are in balance, i.e., in perfect harmony. We also use the term Walrasian General Equilibrium. Economists say that general equilibrium in its pure sense does not exist. The best we can hope for is to get as close to it as possible.

Striving for this equilibrium guides policy and market strategies, aiming to bridge gaps between theoretical models and real-world economic dynamics.

The term economic equilibrium means the same as general equilibrium.

Leon Walras (1834-1910), a French mathematical economist and Georgist, developed the theory. In 1874 and 1877 Walras published Éléments d’économie politique pure. William Jaffé published an English version – Elements of Pure Economics – in 1954.

Georgists believe that we should own all things that we create ourselves, except for economic value derived from land, including natural resources. Those things should belong equally to all the community’s residents.

Walras developed the theory to solve a controversy among economists. Most economic analyses had demonstrated only partial equilibrium in individual markets.

Nobody had shown that general equilibrium could exist, i.e., in all markets simultaneously, until Walras came onto the scene.

General equilibrium is a goal

Even though it is a Utopian state in the world of economics, one that we will never completely achieve, economists believe that total harmony in demand and supply is something we should aspire to.

Although markets never reach total equilibrium, in the long run, they tend towards it. In 1889, Walras wrote:

“The market is like a lake agitated by the wind, where the water is incessantly seeking its level without ever reaching it.”

When demand for all products is more or less equal to supply, prices are stable. People can make long-term plans because it is easier for them to predict their future finances. Subsequently, sustainable GDP (gross domestic product) growth is more likely to occur.

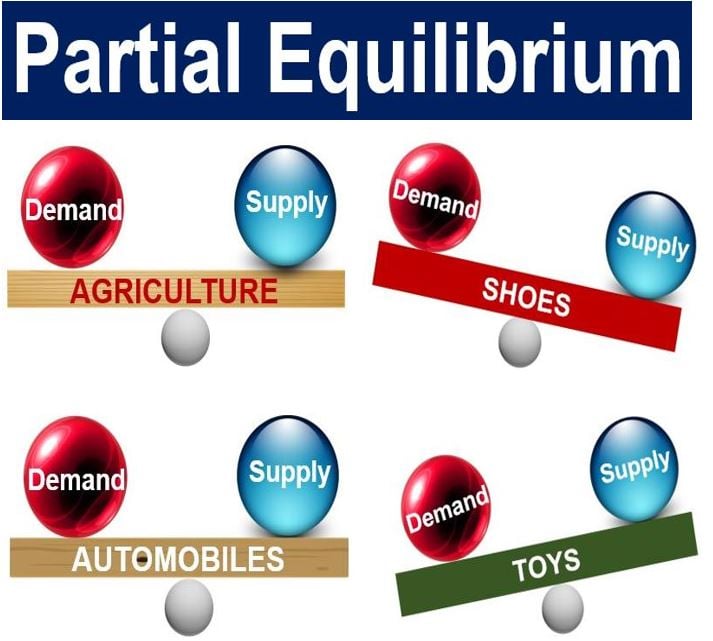

Partial equilibrium

Partial equilibrium is a condition of economic equilibrium which only occurs in part of the the economy. For example, in this image, we have attained equilibrium in the demand and supply of automobiles and agriculture, but not the toys or shoes markets.

Partial vs. general equilibrium

While general equilibrium refers to the whole economy, where demand is equal to the supply of every single good and service in every market, partial equilibrium takes into consideration only a part of the market.

Partial equilibrium analysis treats one particular sector of the economy as functioning in isolation from all the other sectors.

George Stigler (1911-1991), an American economist who received the Nobel Memorial Prize in Economic Sciences in 1982, wrote:

“A partial equilibrium is one which is based on only a restricted range of data, a standard example is price of a single product, the prices of all other products being held fixed during the analysis.”

General equilibrium analysis

General equilibrium analysis is a comprehensive study of several economic variables – their interdependences and interrelations for understanding how the economic system as a whole functions.

It brings together the cause and effect sequences of changes in the quantities and prices of goods and services in relation to the whole economy.

An economy is only in general equilibrium when every consumer, every company, every industry and every factor-service is in equilibrium at the same time.

We reach general equilibrium when every single price is in equilibrium. Consumers spend their earned income in a way that yields maximum satisfaction. Also, every company in each industry sector is in equilibrium at all prices and outputs. Additionally, the supply and demand for factors of production are the same as equilibrium prices.

General equilibrium analysis is based on nine assumptions:

- Perfect competition exists in the goods, services, and factor markets.

- Consumers’ tastes and habits are given and constant.

- Consumers’ incomes are given and constant.

- Factors of production are perfectly mobile between different places and occupations.

- Returns to scale are constant.

- All companies do business under the same cost conditions.

- All units of a productive service are the same.

- Techniques of production do not change.

- There is full employment of all resources, including labor.

Given these nine assumptions, we attain general equilibrium when demand for every single product is equal to their supply. The equilibrium also includes all services.

Consumers’ decisions regarding each product and producers’ decisions for the production of each item operate in a state of total harmony.

This equilibrium fosters a predictable economic environment, encouraging investment and innovation across all sectors.

Moreover, it optimizes resource allocation, minimizing waste and enhancing overall economic efficiency.