The Law of Increasing Opportunity Cost states that when a company continues raising production its opportunity cost increases. Specifically, if it raises the production of one product, the opportunity cost of making the next unit rises. This occurs because the producer reallocates resources to make that product. However, using those resources for the original good was more profitable for the company.

Every business tries to use its resources to maximum capacity, i.e., efficiently. None of us has unlimited resources. Therefore, it is critical that we make the right choices regarding what we do have.

Our opportunity costs influence our decisions, economists say.

Every time we commit more of our company’s resources in a particular direction, we will run into the law of increasing opportunity costs.

What is opportunity cost?

Opportunity cost is the value of the best alternative choice when you pursue a certain action. In other words, the difference between what you have chosen to do and what you could have chosen.

Let’s imagine you ask yourself this question: “If I do this, what will I have to give up?” The opportunity cost is the difference between what you had to give up and what you chose to do.

When we consider costs, we tend to think in terms of monetary costs, i.e., money we spent on something. For example, if your company spent $20,000 on vehicles, then the monetary cost was $20,000.

However, an opportunity cost came with that purchase. By purchasing all those vehicles, your company gave up the opportunity to do something else with that money.

Finding the lowest opportunity cost

That something else is the opportunity cost. Determining the best way to use money is frequently an exercise in finding the choice with the lowest opportunity cost.

Opportunity costs also exist when we don’t spend any money. If I tell one of my workers to clean the warehouse floor rather than answer the phone, I might lose some sales.

Some missed phone calls might have ended up as sales if that employee had been answering the phone.

However, if that employee had answered the phones, the warehouse floor would have remained a mess, and workers may have worked more slowly trying to move around. Subsequently, the company would also have lost business.

Law of increasing opportunity cost

If we continue pouring more and more of a limited resource into an activity, our opportunity cost grows for each additional unit of that resource. That is what the law of increasing opportunity cost says.

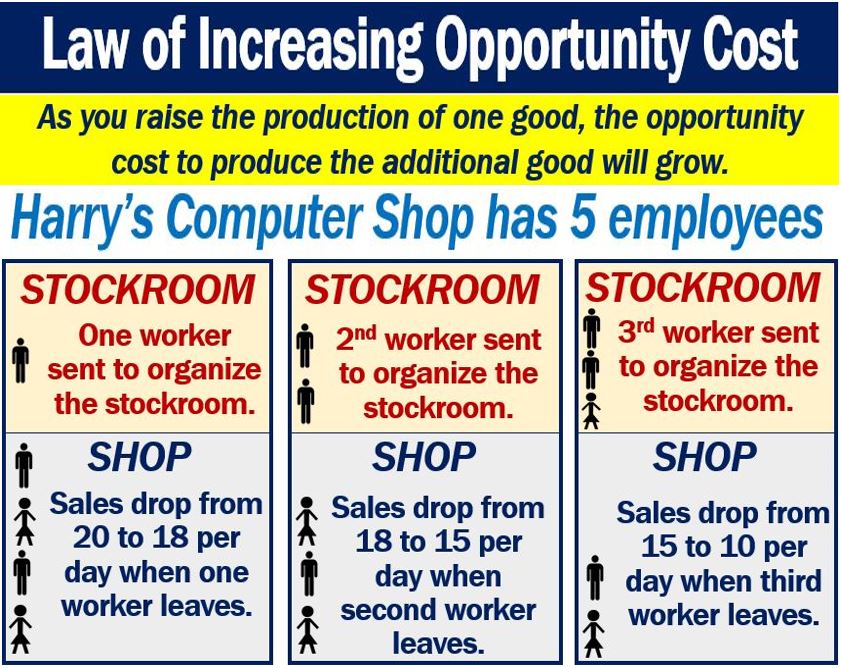

Let’s imagine you own a shop that sells computers. You have five employees. What happens if you send one of them to the back to organize the stockroom?

You would have one less employee working in the shop helping customers. In other words, fewer people trying to persuade customers to buy. You could subsequently lose sales.

What would happen if you sent a second employee to the back, also to organize the stockroom?

You would lose even more sales, especially if the shop suddenly filled up with customers. You would lose even more sales with the second worker you sent to the stockroom than with the first.

Put simply; your employees are limited, i.e., labor is a limited resource. The fourth worker you sent to the back would result in a bigger loss of sales than sending the third. The third employee you sent to the back would represent a larger loss than the second, etc.

Why the law of increasing opportunity cost matters

Bear in mind the law of increasing opportunity cost when taking stock of the resources that you have at your disposal.

Make sure you deploy those resources with the smallest opportunity cost, i.e., with the greatest return.

Cam Merritt explains in an online Chron article that opportunity cost is not a constant.

Regarding opportunity cost, Merritt writes:

“It rises – slowly at first, but more rapidly later on as you apply resources to tasks for which they’re ill-suited and leave other areas neglected.”

Thus, it is imperative to periodically reassess allocation strategies to ensure that the escalation of opportunity costs aligns with long-term business goals

Two Educational Videos

These two interesting video presentations, from our sister YouTube channel – Marketing Business Network, explain what ‘Increasing Opportunity Cost’ and ‘Cost’ are using simple, straightforward, and easy-to-understand language and examples.

-

What is Increasing Opportunity Cost?

-

What is a Cost?