The Lender of Last Resort in each country is its Central Bank. When a bank is in trouble and needs money, and nobody will lend to it, the central bank may intervene and lend, frequently with conditions and strings attached. Sometimes, the central bank will close down the troubled bank, find it a new owner, or take control of it. A lender of last resort is there to prevent a country’s financial system from collapsing.

Confidence in the banking system

The role of the central bank as a lender of last resort makes the creation of credit easier by boosting confidence in the banking system and reducing the risk of a bank run. A bank run is when customers panic and crowds start withdrawing their money.

This fundamental role is crucial, particularly during periods of economic uncertainty, where the central bank’s actions can stabilize the financial sector.

The central bank’s presence reassures customers, specifically depositors, that their money is safe. The International Monetary Fund (IMF) sometimes acts as a lender of last resort, as long as the country in need adopts an economic austerity policy – called IMF’s Austerity Conditionalities.

Put simply, a lender of last resort is usually a country’s central bank that steps in to lend money to banks or financial institutions when they’re in serious trouble and can’t get help anywhere else.

It’s called a “last resort” because it’s only used when all other options have failed. This helps keep the financial system stable and prevents bigger problems, like bank collapses.

Lender of last resort – critics

Central banks have the backing of their governments to make such loans for maintaining public confidence in the financial system.

Critics say that having a lender of last resort may encourage banks to become reckless, because they know that if things go seriously wrong they will be bailed out.

Such claims were validated when large financial institutions were saved following the global financial crisis of 2007/8.

However, proponents argue that the potentially catastrophic consequences of letting everything collapse – having no lender of last resort – is incomparably more dangerous than the reckless behaviors by some banks.

Commercial banks do not like resorting to their central bank for support, and only do so in times of desperate emergencies, because such actions tell everybody that they are in trouble.

The lender of last resort may grant loans not only to banks, but also to any other eligible financial institution, including private firms.

Ambiguous function

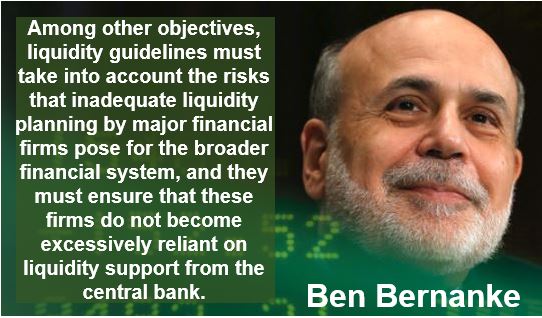

Even the US Federal Reserve acknowledges the ambiguity of the central bank’s role as lender of last resort. In a report in 2014, it wrote:

“The role of lender of last resort is probably the most ambiguous function of a central bank. On the one hand, it is typically regarded as a core responsibility of central banks, given their unique ability to create liquid assets in the form of central bank reserves, their central position within the payment system and their macroeconomic stabilization objective.”

“On the other hand, if the availability of central bank liquidity were certain, individual banks would have reduced incentives to maintain sufficient stocks of liquid assets to cover their liquidity needs.”

“Hence, to limit moral hazard, central banks have in many cases left open how they would respond to liquidity shortages at the level of individual institutions or the market as a whole.”

Central banks have performed the function of lender of last resort several times over the past century.

Lender of last resort – Bank runs

A bank run, or a run on the bank, occurs when a large number of customers withdraw their money from deposit accounts at the same time because they think the financial institution is or may soon become insolvent.

In a fractional-reserve banking system, banks keep only a small percentage of total deposits as cash. A run can very rapidly drain a bank’s liquidity. Customers acting on the worry that their bank may become insolvent can cause that very problem to happen when they panic – a self-fulfilling concern. Virtually every country today has a fractional-reserve banking system.

Following the Wall Street Crash of 1929 that led to the Great Depression, there were many bank runs that caused bank failures. The US government introduced new legislation requiring banks to hold a minimum percentage of their liabilities in the form of cash reserves.

If a bank’s reserves are not enough to deal with a bank run, a lender of last resort intervenes and injects the financial institution with emergency funds so that all customers in the run get paid.

This function helps prevent insolvency and usually takes the wind out of the bank run’s sails – panicked customers eventually calm down and stop taking out their funds.

J. P. Morgan – lender of last resort

There have been times in history when the lender of last resort was a person. At the beginning of the 20th century, John Pierpont Morgan (1837-1913), an American financier and banker who dominated corporate finance and industrial production in the United States in the late 19th and early 20th century, assumed the role.

During the Panic of 1907 in the United States, also known as the Knickerbocker Crisis, the New York Stock Exchange plummeted by nearly 50% from its peak the previous year

A small bank run spread and soon hit virtually every bank across the country. Many of them went bankrupt. This mass panic might have deepened had it not been for the intervention of Mr. Morgan, who pledged huge sums from his own fortune. He managed to convince several wealthy New York bankers to do the same, to shore up the banking system.

Moreover, Morgan’s actions underscored the need for a more formalized and government-backed system to prevent such financial crises.

Subsequently, his influence was instrumental in the establishment of the Federal Reserve System, designed to avoid the necessity of such individual action in the future.