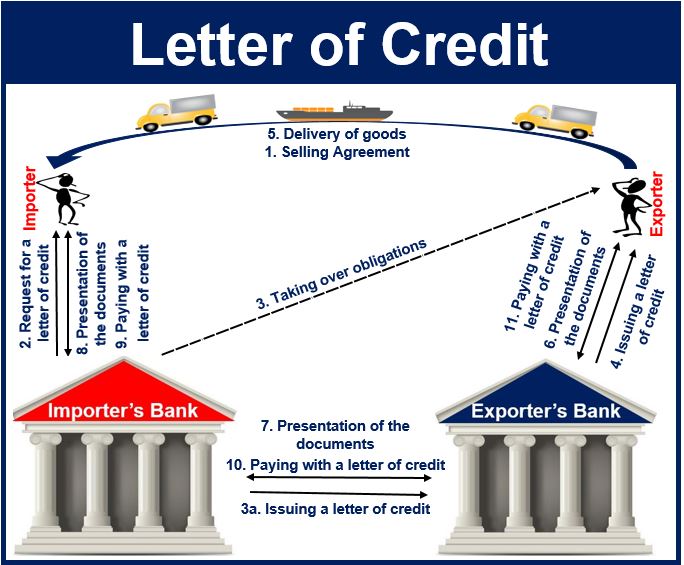

A Letter of Credit is a vital financial instrument in international trade that ensures the seller is paid upon fulfilling contractual obligations.

Also known as Documentary Credit, it is a document from a bank that guarantees payment as long as the seller meets a list of pre-agreed delivery conditions. If the buyer fails to make the payment, the bank will cover the amount due.

In return for the guarantee of payment, the bank will insist on strict terms being met. It will need to receive certain documents, such as shipping confirmation as proof of delivery, before releasing the money.

If the document can be canceled by the customer or the bank, it is called a revocable letter of credit. If it cannot be canceled it is an irrevocable letter of credit, i.e. as soon as the document is formalized, there is no turning back.

According to the United States Government:

“Letters of credit (LCs) are one of the most versatile and secure instruments available to international traders. An LC is a commitment by a bank on behalf of the importer (foreign buyer) that payment will be made to the beneficiary (exporter) provided that the terms and conditions stated in the LC have been met, as evidenced by the presentation of specified documents.”

Origin of the term

The English term ‘letter of credit’ derives from the French word ‘accréditation’ (a power to do something), which comes from ‘accreditivus’, which in Latin means trust.

Letter of credit in Spanish and Portuguese is carta de crédito, French – lettre de crédit, Italian – lettera di credito, German – Akkreditiv, Russian – аккредитив, Japanese – 信用状, and Chinese – 信用证.

Reducing risk

International trade generally involves more risk than buying and selling within the domestic market. Exporters face the possibility of never getting paid for goods, while importers may risk paying and then receiving nothing or the wrong merchandise (in this context, ‘merchandise’ refers to ‘goods’)

As importing and exporting involves greater distances and different legal systems, resolving disputes may be difficult.

Using a letter of credit is one way of reducing the risks. The document can offer a guarantee to the seller that payment will come, while the purchaser can be sure that payment will not be made until the goods are received. Thus, a letter of credit acts as a bridge of trust, securing transactions across global trade landscapes.

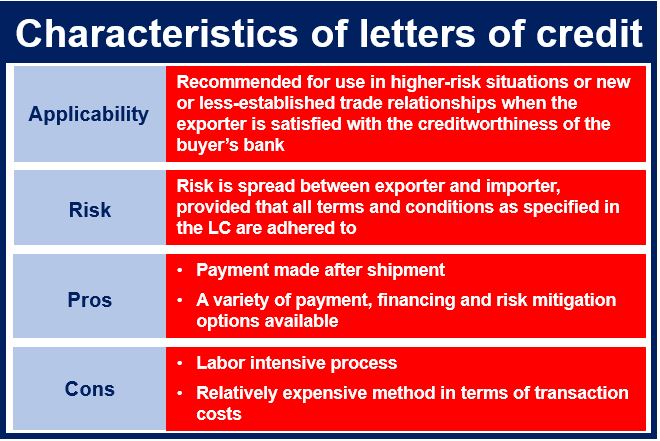

Letter of credit – advantages for the seller and buyer

Advantages for sellers: by requesting an appropriate letter of credit, sellers know they will receive payment in full and on time.

As long as exporters meet all the terms and conditions, a letter of credit is one of the most secure methods of payment for them.

Advantages for buyers: with the document, buyers are certain that sellers will honor their side of the deal and provide documentation proving this.

Things to consider

Before deciding whether you want to use a letter of credit, you should check what the costs are. Banks charge for providing these documents, so you should weigh up the additional costs against the security benefits.

Exporters must remember that they will only be paid if they adhere to the strict terms of the document.

Sellers need to provide documentary proof that they have delivered exactly what they were contracted to supply.

Using a letter of credit may sometimes slow things down, and also bring other administrative problems.

Compare the pros and cons of a letter of credit with alternative arrangements, such as export factoring, cash in advance terms, or credit insurance.

Most governments advise exporters to avoid using a letter of credit because of their costs, and the chances of expensive delays and tedious bureaucracy.

The British government says on its website:

“As a general rule you should probably only consider opening a letter of credit as an importer if your supplier insists on it, or national exchange controls require it.”

The US Government says a letter of credit is useful when it is difficult to get reliable credit information about the foreign buyer, or if the foreign buyer’s credit rating is unacceptable, but the seller is satisfied with the buyer’s bank’s creditworthiness.

Different types of letter of credit

The most commonly used types of letter of credit are:

-

Revocable

It can be changed/cancelled by the bank for any reason and at any time.

-

Irrevocable

It cannot be changed/cancelled unless all the parties involved agree. This type of document provides more security than a revocable one.

-

Confirmed & Unconfirmed

The seller may require that the document be ‘confirmed’ by the bank that checks it. By doing so, the second bank agrees to guarantee payment in case the issuing bank fails to do so. A confirmed letter of credit provides more security than an unconfirmed document.

-

Transferable

The document can be passed from one beneficiary to others. This type of document is more commonly used when intermediaries are involved.

-

Standby

A document issued by the bank providing assurance that the buyer is able to pay the exporter. The exporter does not intend to draw on the document to get paid.

-

Revolving

This type of document can cover a number of different transactions between the exporter and importer.

-

Back-to-Back

This one is used when an intermediary is involved, but a transferable letter of credit is not suitable.

Video – What is a Letter of Credit?

This video presentation, from our YouTube partner channel – Marketing Business Network, explains what a ‘Niche Market’ is using simple and easy-to-understand language and examples.