A Line of Credit is the maximum amount of credit that a financial institution arranges with a borrower. In most cases, the lender is a bank. The borrower may be an individual, business, or government. A charity or trust may also be a borrower.

In some cases, people may refer to it as a bank line, credit line, or revolving credit agreement. It is a type of flexible loan.

Unlike a traditional loan, in a revolving credit agreement, the customer doesn’t have to use the whole amount in one go. Instead, they can use part of the money.

Likewise, the lender will only charge interest on the money that the borrower used from the facility.

Nevertheless, you can withdraw more than you need to, as long as it is within the credit line limit.

Line of credit – access to cash

The money will be ready to use at any time as long as borrowers do not exceed their credit line. They must also make sure they meet the terms they agreed with the lender. For example, if they agree on monthly payments, borrowers must pay them on time.

Customers can pay back their loans according to their cash flow. In other words, they can pay back all at once or in monthly installments.

This type of credit is similar to a credit card lending arrangement. The credit card company tells you how much you can borrow – that is your credit line.

In fact, some credit card companies refer to the customer’s borrowing limit as the ‘credit line.’

However, a line of credit is usually much cheaper than a credit card loan. Credit line interest rates are much lower.

A revolving loan

This type of credit falls under the revolving account type of lending arrangement. In other words, borrowers can spend their available credit, pay it back, and then use it again.

Let’s suppose you take out a line of credit with your bank. When you repay whatever you used from the loan arrangement, that money becomes available again. In other words, you can borrow it again.

As long as you remain within the credit limit, you can keep paying back and borrowing endlessly.

Lines of credit are great for people who need to borrow regularly. The arrangement also saves them having to submit lots of loan applications.

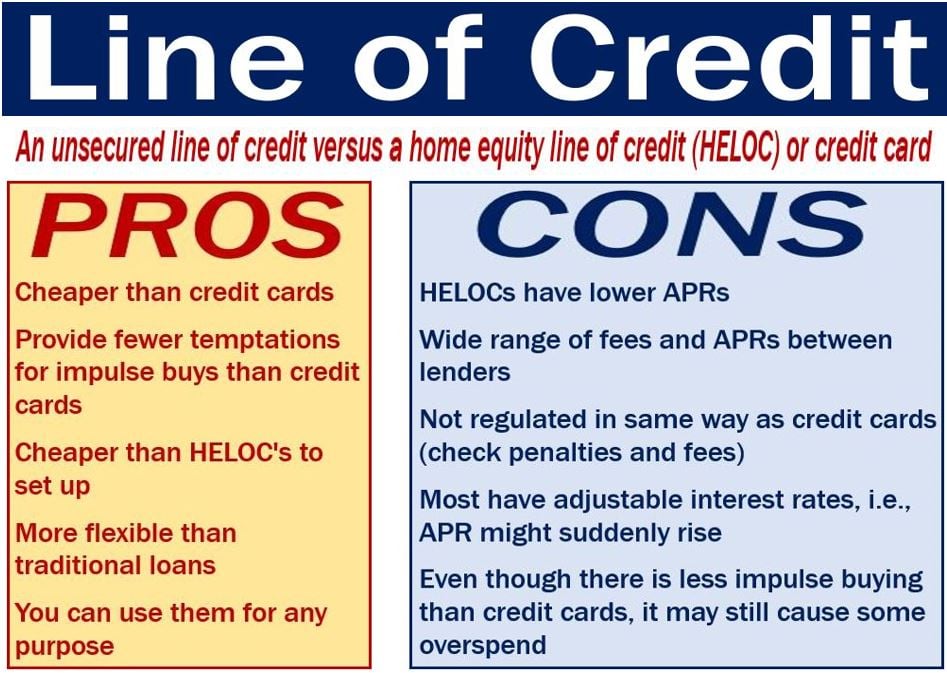

There are two types of credit, unsecured or secured. An unsecured credit line, which applies to most, doesn’t require collateral. In other words, you do not need to offer an asset, such as your or house, as security.

With a secured line of credit, however, the bank can take your house or car if you default on the loan. To default means to fail to pay back a loan. Secured loans are safer for banks and often come with lower interest rates than unsecured loans.