What is microeconomics? Definition and meaning

Microeconomics is a social science; it is the study of individual, isolated units of an economy – those individual pieces, when put together, make up the whole economy. Each person, household, company or industry is a unit of the economy. It is the part of economics that is concerned with single factors and the effects of individual decisions.

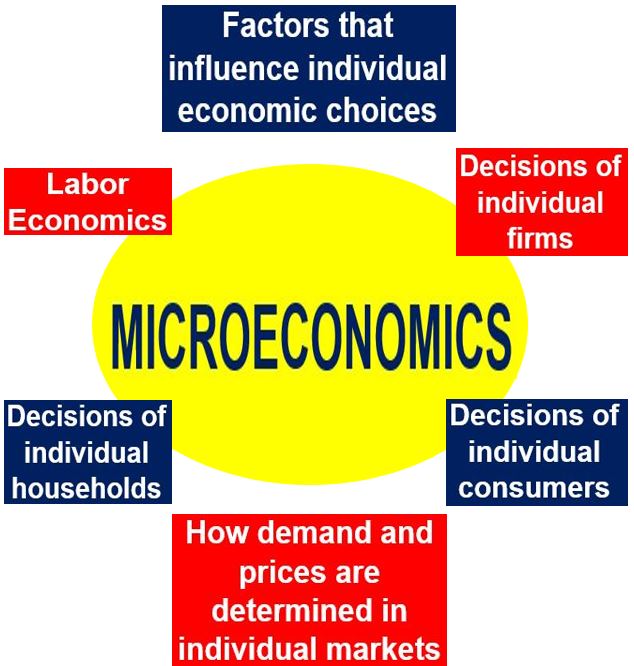

Microeconomics is mainly focused on the factors that influence individual economic choices, the effect of changes that occur in these factors on each decision-maker, and how demand and prices are determined in individual markets.

Microeconomics contrasts with macroeconomics, which is the study of phenomena that span the whole economy, such as unemployment, GDP (gross domestic product) growth or decline, and inflation.

Economics is a social science that covers a vast field, which can be broken down into scores of different divisions. Its two principal branches are microeconomics and macroeconomics.

One of microeconomics’ goals is to analyze the market mechanisms that determine the relative prices of products and services, and allocated limited resources among alternative potential uses. It shows conditions under which free markets eventually lead to desirable allocations.

Put simply, is the the study of how humans make decisions because we are aware that our money and time to purchase things and do everything are limited.

Microeconomics also analyzes how and why markets fail to produce effective and efficient results – market failure.

According to the Financial Times’ dictionary of business terms, microeconomics by definition is:

“The study of trends that pertain to the different elements (companies, industries, consumers, etc.) that make up the economy.”

Microeconomics – uses

A microeconomist studies economic tendencies – what will probably occur when individuals make certain choices or when there are changes in the factors of production. Factors of production include labor, land, capital and entrepreneurship.

Individual units of the economy are commonly broken down into microeconomic subgroups, including business owners, sellers and buyers.

Microeconomics does not attempt to explain what should happen in an economy, but rather it tells us what we should expect if certain conditions change.

If a smartphone maker raises its prices, according to microeconomic theory consumers will buy fewer of its mobile phones. If the whole of the Saudi oil industry went on strike for a month, the price of oil would go up steeply due to a significant decline in the global supply.

If you are an investor, microeconomics might help you see why American Airlines’ share price could fall if ticket sales decline. It could also explain why an increase in the minimum wage could force low-paying fast food restaurants to either take on fewer workers or even make some of them redundant.

However, questions regarding the whole of the economy, such as aggregate demand, GDP forecasts, or predictions on the inflation rate are within the spectrum of macroeconomics. Macroeconomics might tell us what may happen to Germany’s GDP in 2025.

Microeconomics covers these topics

Microeconomics covers a wide range of topics. Below are some of the most common ones.

– Supply and Demand: the most fundamental tools of economic analysis. In winter I need more gas to heat my home, and so do all my neighbors. As a result, overall demand for gas is higher, which means that gas companies charge more for the fuel during winter.

A drop in the supply of gas – perhaps because of a war or natural disaster in a key gas-producing region of the world – will make prices rise.

– Elasticity: is used to help economists determine how much people want something – consumer demand – after the price of a product or service changes.

When a product is elastic, demand for it is sensitive to price changes. An inelastic product has virtually the same demand if its price goes up or down. Expensive cruises are extremely elastic, when prices go up or down by a certain percent, demand for them falls or rises by a greater percentage. Tortillas in Mexico, rice in China, or bread in Europe, the USA and Canada is very inelastic; a 5% increase in their price will make virtually no difference to demand.

– Opportunity Cost: the value of the best alternative choice when making a decision to go along with a certain action. Observing and evaluating the option one had to give up when a choice was made. Like asking yourself: “If I make this choice and do this, what will I have to give up?”

Opportunity cost is basically the value of the next-highest-valued alternative use to a resource. If you go to the theater, you spend time watching the play and money buying the ticket. The opportunity cost would be the lost time at home watching TV and the money that might have been spent on something else.

– Theory of Production: or production theory, is the study of production, or the economic process of transforming inputs (raw materials) into outputs (finished products).

When we produce things or deliver services we use resources (commodities) to create them, resources that are suitable for making things.

The management of a company has to decide how much of each commodity is used, how much is produced, as well as how much of its labor and fixed capital it will use.

Production theory defines the relationships between the prices of the raw materials and productive factors on the one hand, and the quantities of these materials and productive factors that are produced on the other hand.

– Monopoly: when a single company has virtually all market share; it is the only supplier of a particular product or service.

– Oligopoly: like a monopoly, but in this case there are at least two suppliers, however, the market is controlled by a very small number of companies.

Microeconomics also includes Economics of Information, Welfare Economics, Labor Economics, Game Theory, Market Structure, Costs of Production, Perfect Competition, and many other topics.

Video – What is microeconomics? – Definition and Meaning

This Investors Trading Academy video explains what microeconomics is, and what it is used for.