Open market operations, also known as OMOs, refers to the buying and selling of securities in the open market by a country’s central bank.

OMOs are a key tool used by the US Federal Reserve, the Bank of England, the European Central Bank, and other central banks across the world in the implementation of monetary policy.

These central bank interventions manipulate liquidity levels. When they purchase securities they inject liquidity into the country’s economy, when they sell them, they soak up the liquidity.

The aim in the short-term of open market operations in the United States is specified by FOMC (Federal Open Market Committee).

In the US, OMOs are performed by the Trading Desk at the Federal Reserve bank of New York. The Federal Reserve (Fed) is only authorized to buy and sell a limited range of securities.

The central banks of most advanced economies are not allowed to lend money without requiring suitable assets as collateral. Therefore, central banks describe which assets may be bought and sold in open market operations.

Technically, the country’s central bank lends a certain amount of money and simultaneously takes the same amount of an eligible asset which the borrowing commercial bank supplies.

Open Market Operations occur when the central bank purchases or sells securities in the open market – it is the main method for implementing monetary policy. They either pump money into the economy to kick-start it, or suck money out to reduce inflation.

OMOs may also directly target money supply growth – however this is extremely rare. The vast majority of central banks directly target interest rates, which are adjusted to meet annual inflation targets.

The Federal Open Market Committee (FOMC), part of the US Federal Reserve, has traditionally sold and bought securities, mainly US Treasury securities and federal agency securities, either through repurchase agreements or outright purchases, in the open market through primary dealers

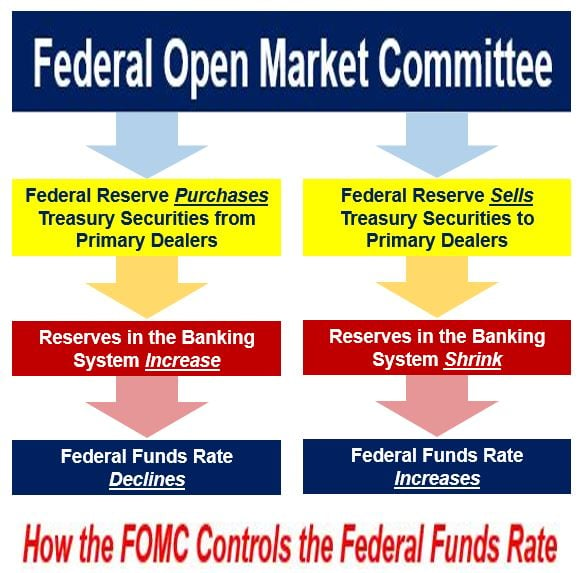

. According to the Office of the Inspector General of the Federal Reserve: “By adjusting the level of reserve balances, the Federal Reserve influences the federal funds rate as shown by the diagram above.” (Image: adapted from oig.federalreserve.gov)

. According to the Office of the Inspector General of the Federal Reserve: “By adjusting the level of reserve balances, the Federal Reserve influences the federal funds rate as shown by the diagram above.” (Image: adapted from oig.federalreserve.gov)

According to the Reserve Bank of Australia, the country’s central bank:

“Open market operations are conducted almost every business day at 9.30 am and occasionally at 5.10 pm (AEST/AEDT). From time to time, the Reserve Bank may decide not to conduct open market operations on a given day if it judges that the banking system has the appropriate amount of liquidity.”

Open market operations – a tool

Open market operations are one of three basic tools that central banks use to reach their monetary policy goals. The other two are: 1. Changing the terms and conditions for borrowing at the discount window. 2. Altering the required reserve requirement ratios.

The execution of open market operations in the ‘open market’ – often called the secondary market for securities purchases – is a central bank’s most flexible means of seeing through its objectives.

According to the Federal Reserve Bank of New York:

“By adjusting the level of reserve balances in the banking system through open market operations, the Fed can offset or support permanent, seasonal or cyclical shifts in the supply of reserve balances and thereby affect short-term interest rates and by extension other interest rates.”

The European Central Bank says the following regarding open market operations: “It is an important tool for managing interest rates, market liquidity, and signaling the next policy movement.” (Image: Adapted from image.slidesharecdn.com)

The European Central Bank says the following regarding open market operations: “It is an important tool for managing interest rates, market liquidity, and signaling the next policy movement.” (Image: Adapted from image.slidesharecdn.com)

Two types of open market operations

In the US, open market operations are divided into two types:

– Permanent: – these involve the outright buying or selling of securities for SOMA (System Open Market Account), the Fed’s portfolio.

Permanent OMO’s are traditionally used to accommodate long-term factors driving the expansion of the Fed’s balance sheet – primarily, the trend growth in the amount of money in circulation.

When the global financial crisis struck, and for a period afterwards, open market operations were used to adjust the Fed’s holdings in securities, the aim being to put downward pressure on longer-term interest rates, as well as making financial conditions more accommodative.

– Temporary: these OMOs are mostly used to deal with reserve needs that the central bank deems to be transitory in nature. These operations are either Repos (repurchase agreements) or RRPs (reverse purchase agreements or reverse repos).

Under a reverse repo, the agreement is that the central bank sells a security and repurchases it at a later date. A reverse repo is the economic equivalent of collateralized borrowing by the central bank.

The US Federal Reserve has been conducting open market operations since the 1920s through the Open Market Desk at the Federal Reserve Bank of New York.

The European Central Bank (ECB) says that the Eurosystem’s regular open market operations consist of:

– Main Refinancing Operations: also known as MROs. These are one-week liquidity-providing operations in euros. They serve to steer interest rates over the short term, to signal the monetary policy stance in the euro zone, and to manage the liquidity situation.

– Longer-Term Refinancing Operations: also known as LTROs. These are three-month liquidity-providing operations in euros. They serve to provide additional financing to the financial sector over the long term.

In an article published online by the International Monetary Fund – Transformations to Open Market Operations [PDF] – Stephen H. Axilrod writes:

“By buying or selling bonds, bills, and other financial instruments in the open market, a central bank can expand or contract the amount of reserves in the banking system and can ultimately influence the country’s money supply. When the central bank sells such instruments it absorbs money from the system.”

“Conversely, when it buys it injects money into the system. This method of trading in the market to control the money supply is called open market operations.”

OMOs – Advanced and emerging economies

Open market operations are a key instrument of monetary manipulation in the advanced economies (rich nations), and are rapidly becoming major tools in the emerging and developing countries too.

OMOs allow central banks significant flexibility in the volume and timing of monetary operations at their own initiative, encourage a business-like and impersonal relationship with the players in the marketplace, and provide a useful alternative to direct controls.

Direct controls tend to have less of an impact as economies expand – markets by their nature eventually find a way to circumvent them, especially in today’s global economy.

In the same IMF article quoted above, Mr. Axilrod wrote:

“With more countries seeking to deregulate and unleash the potential of market forces, many policymakers and central bankers are grappling with ways to realize the full benefits of open market operations.”