What is producer surplus? Definition and meaning

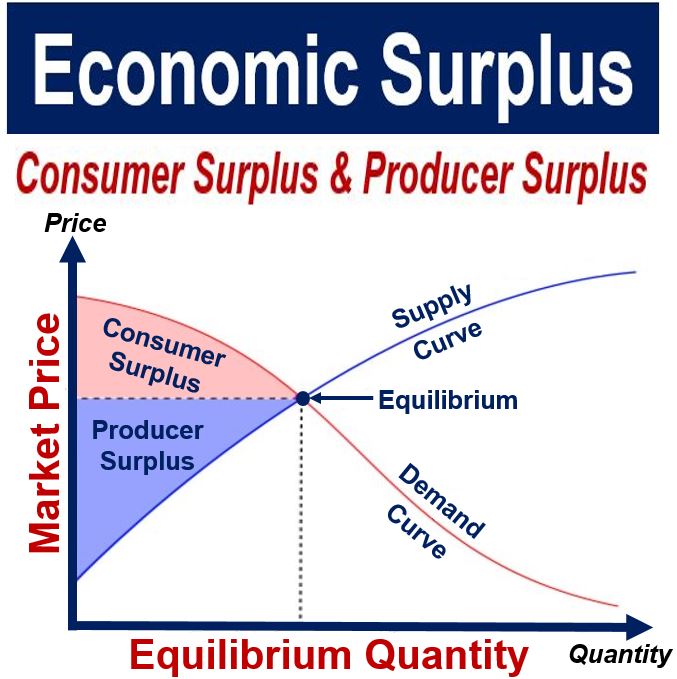

Producer surplus, in economics, is the difference between how much a supplier sells a good or service for, and the lowest amount that he or she would be willing to sell it for. It is the benefit the producer obtains from a sale – the bigger the difference between the two amounts, the greater the benefit. It is a measure of producer welfare, which in a graph is shown as the area below the equilibrium price.

Instinctively, suppliers are always trying to maximize their producer surplus by trying to sell as much as they can at higher prices.

However, there is a limit to how high prices can go – if they go too high, demand declines and eventually disappears completely. There is only so much that consumers will continue buying a can of Coke for – if prices were set at, say $100 per can, demand would fall to zero.

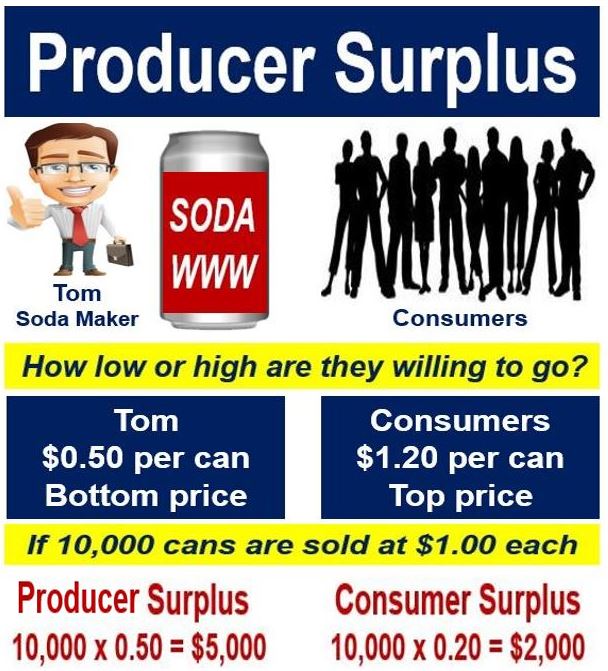

In this image, Tom sold higher than his bottom price, and the consumers bought lower than their top price – they both had surpluses. In a free market, the consumer surplus and producer surplus are constantly changing, because competitors alter their prices to gain market share and consumers are always shopping around for good deals.

According to BusinessDictionary.com, to define producer surplus is:

“In economics, the difference between the amount that a producer receives from the sale of a good and the lowest amount that producer is willing to accept for that good. The greater the difference between the two prices, the greater the benefit to the producer.”

Consumer vs. producer surplus

In mainstream economics, the term economic surplus, also called the Marshallian surplus or total welfare, refers to Consumer Surplus and Producer Surplus.

– Consumer Surplus: the difference between how much a consumer paid for a good or service and how much he or she was willing to pay – the highest price he/she would be willing to accept.

– Producer Surplus: the same thing, but from the producer’s point of view. It refers to the difference between the producer’s sale price and how much he or she was willing to sell it for – how low he would go. The amount is roughly equal to the producer’s profit, since he or she would not normally be willing to sell goods or services at a loss.

The two terms were first proposed by Arsène Jules Étienne Juvenel Dupuit (1804-1866), an Italian-born civil engineer and economist, and brought into mainstream economics language by British economist Alfred Marshall (1842-1924), probably the most influential economist of his time. He first used the terms publicly in his 1980 book – Principles of Economics.

Consumer surplus combined with producer surplus is the overall economic benefit or surplus provided by consumers and producers who interact in a market economy, as opposed to a command economy (communism) or one with quotas and price controls.

Most producers aim to charge each consumer the maximum price he or she is willing to pay. If this is achieved, the producer has captured the whole economic surplus – the producer surplus would be equal to the overall economic surplus.

Example of producer surplus

Imagine you produce and sell cans of Soda WWW, a popular fizzy drink like Coke or Pepsi. You are willing to sell 1,000 cans for the minimum price of $0.50 each, while consumers are willing to pay $1.20.

If you sold 1,000 cans and received the amount that consumers were willing to pay, you would get 1.20 x 1,000 = $1,200.

To calculate your producer surplus, subtract how much you received by the minimum you were willing to accept. The calculation would be as follows:

How much they were sold for – minus – how low you would have sold them for

$1,200 – $500 = $700

Your producer surplus is $700

Your surplus, as a producer, is rarely constant. In a market economy, prices go up and down all the time.