The production function is a mathematical method of describing the relationship between the quantity of inputs utilized by a company and how much it produces with them (output), i.e. a mathematical way to describe the input-output relationship.

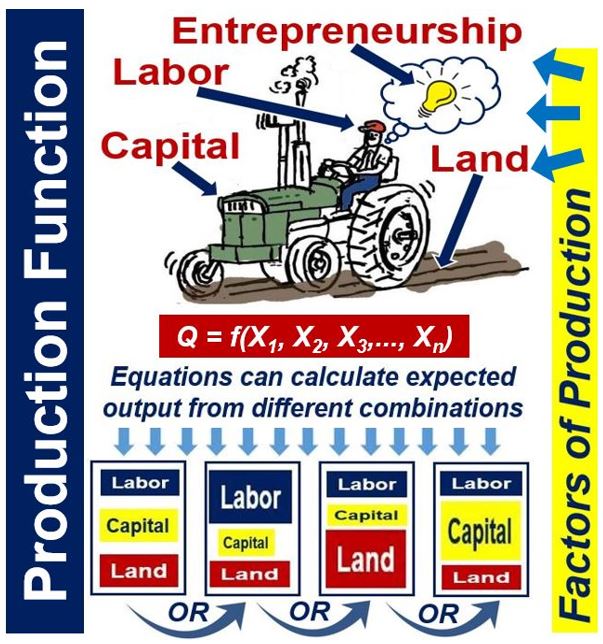

Production is the result of cooperation of 1. Land 2. Labor 3. Capital 4. Entrepreneurship – the four factors of production. Input refers to the factors of production.

If, in order to produce one more unit of an item requires a lower quantity of inputs compared to what was needed to make the last unit, the company is said to be enjoying increasing returns to scale, also known as increasing marginal product.

If, however, the producer requires more inputs to make the next unit than were required for making the previous one, it is facing diminishing returns to scale, also called diminishing marginal product.

Production function is a mathematical method that describes the input-output relationship. Input consists of the four factors of production – land, capital, labor and entrepreneurship. How those four factors are combined, and in which proportions, can affect the output total, as well as productivity.

Production function is a mathematical method that describes the input-output relationship. Input consists of the four factors of production – land, capital, labor and entrepreneurship. How those four factors are combined, and in which proportions, can affect the output total, as well as productivity.

The production function of a commercial enterprise generally focuses on the physical things – it does not take into account the abstract aspects of products, such as prices.

Production function – usage

It is one of the main concepts of mainstream neoclassical theories. Neoclassical economics focuses on the determination of goods, outputs, and income distributions in the economy through supply and demand

Businesses use production function to find out how much output they should get given the market price of a product, and what input combinations they should use to produce something given the price of labor and capital.

American economist, Paul Anthony Samuelson (1915-2009), the first US citizen to be awarded the Nobel Prize for Economics, once said: “The production function is the technical relationship telling the maximum amount of output capable of being produced by each and every set of specified inputs. It is defined for a given set of technical knowledge.”

American economist, Paul Anthony Samuelson (1915-2009), the first US citizen to be awarded the Nobel Prize for Economics, once said: “The production function is the technical relationship telling the maximum amount of output capable of being produced by each and every set of specified inputs. It is defined for a given set of technical knowledge.”

In other words, it can be used to determine the most economical (cheapest) combination of factors of production that can be utilized to make something.

It can answer a range of questions that management needs to answer when planning production and prices. It can measure marginal productivity of a specific factor of production – how output changes from one extra unit of that factor.

Production function reflects how much output we should expect if we have so much of one factor of production, say labor, and so much of another factor, such a capital, and so much of another, etc. It is the indicator of the physical relationship between inputs and output of a producer.

A production function may be expressed with this mathematical equation:

Q = f(X1, X2, X3,…, Xn)

Where Q is the output quantity and X1, X2, X3,…, Xn are the quantities of factor inputs, such as labor, land or raw materials, capital

Production function and technology

The production function of a company depends on the state of its technology. Every time there is a new development in technology, the production function of that company undergoes a change.

This new production function caused by new technology displays either:

– The same output with fewer inputs, or

– The same inputs with greater output.

On some occasions, a new production function slows everything down or undermines efficiency and productivity – it takes more inputs to achieve the same output.

A short-run production is said to exist when one or more of the four factors of production have not changed from their initial value – this is usually land, and sometimes also capital (machinery). Long-run production occurs when all the factors of production have changed. Remember that technically-speaking, the difference between the two is not how long or short the periods are, but rather how many factors have changed.

A short-run production is said to exist when one or more of the four factors of production have not changed from their initial value – this is usually land, and sometimes also capital (machinery). Long-run production occurs when all the factors of production have changed. Remember that technically-speaking, the difference between the two is not how long or short the periods are, but rather how many factors have changed.

Video – Production Function & Total Costs

This video explains what production function is using simple terms and easy-to-understand examples.