What is real options theory? Definition and meaning

Real options theory is a modern theory on how to make decisions regarding investments when the future is uncertain. Real options theory draws parallels between the valuation of the financial options available and the real economy. The theory has become a popular theme in most business schools across the world, as well as the boardroom, especially within oil companies.

In the world of business, a ‘real option’ is a choice available to a company regarding an investment opportunity. The term ‘real’ means that it refers to a tangible asset and not a financial instrument.

Examples of real options include determining whether to build a new factory, change the machinery and technology on a production line, decide whether to buy potentially lucrative oil fields and when to start drilling or pumping, etc. They do not include derivative financial instruments such as stocks or bonds.

Real options theory is based on logical financial options in capital investments in the sense that they create a certain level of valuable flexibility. If you have financial options, you then have the freedom to make the best choices and decisions, such as where and when to make a specific capital investment.

Real options theory is based on logical financial options in capital investments in the sense that they create a certain level of valuable flexibility. If you have financial options, you then have the freedom to make the best choices and decisions, such as where and when to make a specific capital investment.

The investment choices we have with tangible assets are similar to those that exist with financial instruments. In theory, tangible assets (real assets) could be valued according to the same methodology.

The Economist’s glossary of terms has the following comment regarding real options theory:

“Traditional investment theory says that when a firm evaluates a proposed project, it should calculate the project’s Net Present Value (NPV) and if it is positive, go ahead.”

“Real options theory assumes that firms also have some choice in when to invest. In other words, the project is like an option: there is an opportunity, but not an obligation, to go ahead with it.”

Real options theory – a new theory

Real options theory is a major new framework in the theory of investment decision-making. It modifies NPV (Net Present Value) theory of investment decisions. NPV theory says that an investment project’s future cash flows are estimated, and if there is doubt regarding those cash flows, the expected value is determined.

The expected cash flows are discounted at the capital cost for the company, and the results are added up. If the NPV is zero, it makes no difference to the company whether the project is approved or turned down. If it is greater than zero, NPV theory tells us to go ahead with the project.

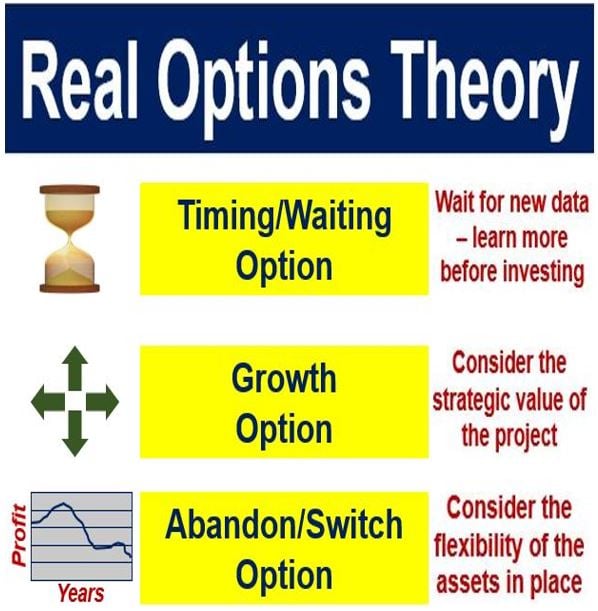

According to Real Options in Petroleum: “In most real investment opportunities there are managerial flexibilities (real options) embedded into the projects. The higher the managerial freedom degree, the higher is the value of the investment opportunity. For most capital investment in petroleum industry, the timing is the main option to be considered. In many cases, for large sunk cost like investment in offshore petroleum fields, is possible to consider only the timing option.”

According to Real Options in Petroleum: “In most real investment opportunities there are managerial flexibilities (real options) embedded into the projects. The higher the managerial freedom degree, the higher is the value of the investment opportunity. For most capital investment in petroleum industry, the timing is the main option to be considered. In many cases, for large sunk cost like investment in offshore petroleum fields, is possible to consider only the timing option.”

In an article on the San Jose University website – Real Options Theory – Thayer Watkins explains that NPV, however, makes no provision for possible modifications to the project once it is underway – real options idea fills that gap in the NPV deficiency.

By not making any provision for this flexibility of the project, NPV consequently does not fully value its potential advantages.

In petroleum exploration contract auctions, it is common for the largest bids to be greater than the net present value calculation. This is because the winning bidder was aware that as soon as some initial drilling was completed, the company could – on the basis of the new information gathered from that initial digging – stop the exploration or expand it.

Real options theory – you have a choice

Real options approach assumes that companies have some choice regarding when to invest – their proposed project is similar to an option; there is an opportunity, which is not an obligation, to approve it and go ahead.

As occurs with financial options, the key question is when to exercise that option: certainly not when the company has no funds (the cost of investing is greater than the benefit).

Investors in financial options should not necessarily invest as soon as they have money, when the benefit of making that choice is greater than the cost – a better option may be to wait until it has lots of money, when the benefits are considerably greater than the cost.

Similarly, firms should not always invest as soon as their project has an NPV equal to or marginally greater than zero – waiting might be better.

In other words:

When the cost of investing exceeds the benefit

Don’t do it, according to both NPV or real options theory

When the cost of investing equals the benefit

Doing it or not doing it would both be a wise option, according to NPV theory

When the cost of investing is slightly less than the benefit

Do it, says NPV concept. Real options theory says you could do it now, but you could also consider waiting until the circumstances are even more favorable.

When the cost of investing is much less than the benefit

Real options theory allows you to wait until you are here before deciding to approve the project

Real options theory – an example

The majority of companies have embedded in them investment opportunities with a range of managerial options.

For example, imagine an oil company whose management thinks it has discovered a new oil field.

However, nobody knows exactly how much oil is in there – neither do they know what the oil price will be when they start pumping that oil.

They have two decisions to make:

– Purchase the lease and start drilling?

– If Oil is Discovered, should they begin pumping?

We know that oil prices can fluctuate significantly. So, it would make more sense to wait until oil prices were considerably higher than an NPV equation of slightly more than or equal to zero before giving the go-ahead.

The Economist’s glossary of terms shows how in the example above, the oil company’s choices are similar to those faced by an investor considering financial instruments:

“In the case of the oil company, for instance, the cost of LAND corresponds to the down-payment on a call (right to buy) option, and the extra investment needed to start production to its strike price (the money that must be paid if the option is exercised).”

“As with financial options, the longer the option lasts before it expires and the more volatile is the price of the underlying asset (in this case, oil) the more the option is worth.”

This is the logic behind the real options theory. In practice, however, valuing real options is extremely difficult, as are pricing the financial options.

Video – What are real options? – Definition and Meaning

This IFT video explains what real options are. It starts by comparing them to financial options.