What is stability? Definition and meaning

Stability is a term used by economists to describe a country’s financial system that displays only tiny output growth fluctuations and has a long track record of low inflation. All the advanced economy’s central banks, and those of most of the rest of the world, see economic stability as a desirable state.

Several factors contribute to a nation’s economic stability, including geographical location, human capital, weather, technology development, infrastructure levels, natural resources, commodity prices, and its political system.

For some economies, a lack of natural resources has not prevented them from being among the most stable in the world. Japan, a very-densely populated group of islands with relatively very few natural resources, has an extremely stable economy.

Countries that enjoy stability have continuously improving efficiencies, greater productivity, and low levels of unemployment.

Over the past 100 years, growing international trade and advances in telecommunications technology have made the world a much smaller place and countries considerably more interdependent. Today, the economic stability of one country or region means the economic stability of another, and often of the rest of the world as well.

Over the past 100 years, growing international trade and advances in telecommunications technology have made the world a much smaller place and countries considerably more interdependent. Today, the economic stability of one country or region means the economic stability of another, and often of the rest of the world as well.

Nations that are economically unstable tend to share a number of features, such as long periods of recession, frequent crises, increasing inflation, over-dependence on commodity prices, and a volatile currency.

Economic instability undermines economic growth, reduces consumer confidence, and discourages foreigners from investing in the country.

According to BusinessDictionary.com, economic stability is:

“A term used to describe the financial system of a nation that displays only minor fluctuations in output growth and exhibits a consistently low inflation rate. Economic stability is usually seen as a desirable state for a developed country that is often encouraged by the policies and actions of its central bank.”

Stability and international trade

The expansion of international trade has helped boost GDP growth in the world’s economies. However, it also means that today the state of the economy of one nation affects the stability of others.

When one economy today becomes unstable, the inflows of capital – international investments and spending from abroad – can decline considerably.

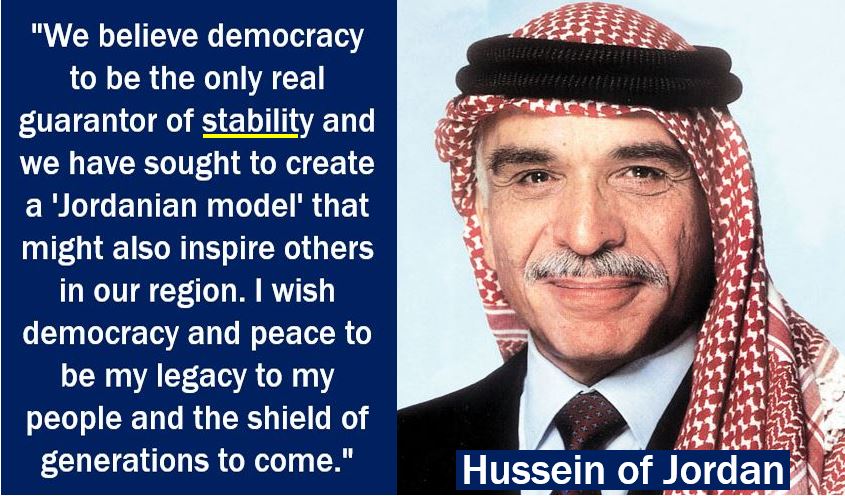

Hussein bin Talal (Arabic: حسين بن طلال, 1935-1999), known as Hussein of Jordan, was King of Jordan from 1952 to 1999. In 1994, he became the second Arab head of state to recognize Israel (after Egypt’s Anwar Sadat in 1978/79). He had begun negotiating a treaty of peace with Israel in the 1960s in secret. Hussein of Jordan was a strong believer in parliamentary democracy.

Hussein bin Talal (Arabic: حسين بن طلال, 1935-1999), known as Hussein of Jordan, was King of Jordan from 1952 to 1999. In 1994, he became the second Arab head of state to recognize Israel (after Egypt’s Anwar Sadat in 1978/79). He had begun negotiating a treaty of peace with Israel in the 1960s in secret. Hussein of Jordan was a strong believer in parliamentary democracy.

Companies, individuals and the government of one country can suffer if the economy of another nation becomes unstable. The value of their investments may either decline or disappear completely, and suppliers with customers in the country that is in trouble may lose sales.

Economic stability and business cycles

Business cycles, also referred to as boom-bust cycles, are alternating periods of recession and recovery caused by changes in production and trade in a market economy.

A business cycle consists of:

- A depression

- A recession

- A recovery

- A peak stage

Countries that have very large differences between their depression and peak stages are usually seen as economically unstable.

A country that is stuck in long periods of recession or depression also lacks economic stability.

All countries’ economies experience periods of instability as they enter the business cycle’s recession or depression stages. The last time this happened to all the advanced economies at the same time was during the 2007/8 global financial crisis, which triggered the Great Recession.

In 2009, as the world was trying to recover from the Global Recession, Dominique Straus-Kahn, who was then Managing Director of the International Monetary Fund (IMF), wrote:

“It is my abiding belief that they are intimately entwined. If you lose one, you are likely to lose the other. Peace is a necessary precondition for trade, sustained economic growth, and prosperity. In turn, economic stability, and a rising prosperity that is broadly shared—both within and among countries – can foster peace.”

“This is most likely to happen in an atmosphere of economic cooperation, of openness, of a multilateral approach to economic and political problems.”

Video – Economic stability and the government’s role

This video explains what happened in North America, Europe and Asia during the last global financial crisis. It talks about the government’s role in maintaining economic stability.