Whole life insurance – definition and meaning

Whole life insurance is a kind of permanent life insurance, i.e. the coverage and possibility of premiums last for the policyholder’s entire life. As long as the insured individuals make the premium payments as agreed, their insurance coverage is valid throughout their lives, and the amount of death benefit is a guaranteed sum.

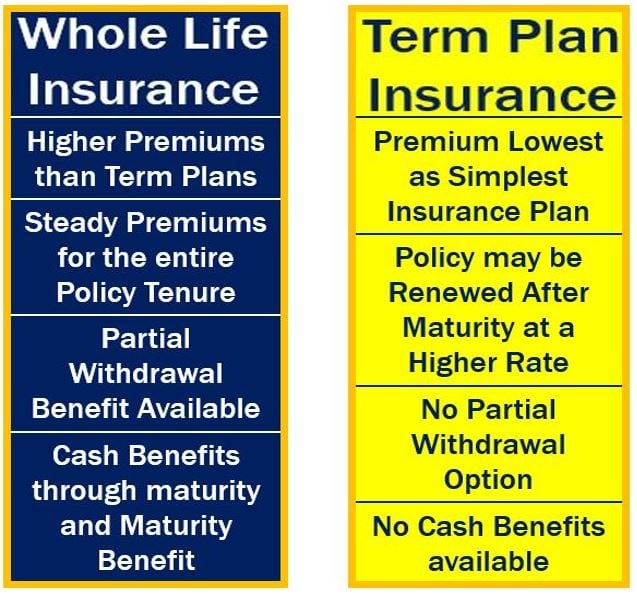

In this type of insurance, premiums are set – they cannot be raised. Policyholders may choose to have smaller premium payments throughout the life of their policy, bigger payments over a reduced period (limited pay whole life), or smaller premiums at the beginning and larger premiums later on.

Whole life insurance dividends are usually paid on whole life contracts and may be used to either reduce the premiums or increase the death benefit.

Whole life insurance has several advantages over other types of insurance coverage. It covers you throughout your lifetime, plus there is a cash value.

Whole life insurance has several advantages over other types of insurance coverage. It covers you throughout your lifetime, plus there is a cash value.

According to Financial-Dictionary.theFreeDictionary.com, whole life insurance is:

“A contract with both insurance and investment components: (1) It pays off a stated amount upon the death of the insured, and (2) it accumulates a cash value that the policyholder can redeem or borrow against.”

Whole life insurance – cash value

When policyholders pay the premiums on their whole life policy, part of each payment builds up as a cash value. The insurer usually invests that cash value, which as long as the policy is in force continues growing tax deferred.

Policyholders can borrow money against that cash value. However, unpaid interest and policy loans will be deducted from the policyholder’s death benefit.

Policyholders can also cancel their policy and get cash. However, if they do this, they will lose their insurance coverage.

Term insurance policies are ideal for some people because they offer higher cover for a lower price than whole life policies. Bear in mind, however, that with term insurance the cover is only valid for a specified number of years, i.e. for a ‘term’, hence the name.

Term insurance policies are ideal for some people because they offer higher cover for a lower price than whole life policies. Bear in mind, however, that with term insurance the cover is only valid for a specified number of years, i.e. for a ‘term’, hence the name.

If the whole life insurance policy is cancelled within the first ten years, the policyholder will get back considerably less than his or her total premiums paid.

Regarding investment returns on this type of insurance policy, Paris-based multinational insurance giant, AXA, writes:

“Investment returns on whole life insurance are typically lower than other types of permanent insurance, because the insurance company invests the cash value in extremely conservative vehicles, such as bond funds.”

“If you are seeking the potential for greater investment returns or want more control over your cash value investment decisions, variable life or variable universal life may be a more appropriate choice.”

Term vs. whole life insurance

Term life insurance has an end date. Most companies offer term life insurance policies extending for up to 30 years maximum, depending on the person’s age.

Term life insurance is considerably easier to understand and costs significantly less than whole life insurance.

Whole life insurance lasts the rest of the policyholder’s life, so his or her beneficiaries are guaranteed money regardless of when death occurs.

Whole life insurance, unlike term life insurance, builds up a cash value as well, which is money the policyholder can access while still alive.

Whole life insurance is one of four main types of life insurance, the other three being universal life insurance, endowments, and limited pay.

Video – Whole Life Insurance Explained

In this America’s Professor video, Prof. Jack Morton explains what a whole life insurance policy is. He begins by saying: “It is life insurance, but it’s more.”