Investors may be giving private-school CEOs the benefit of the doubt.

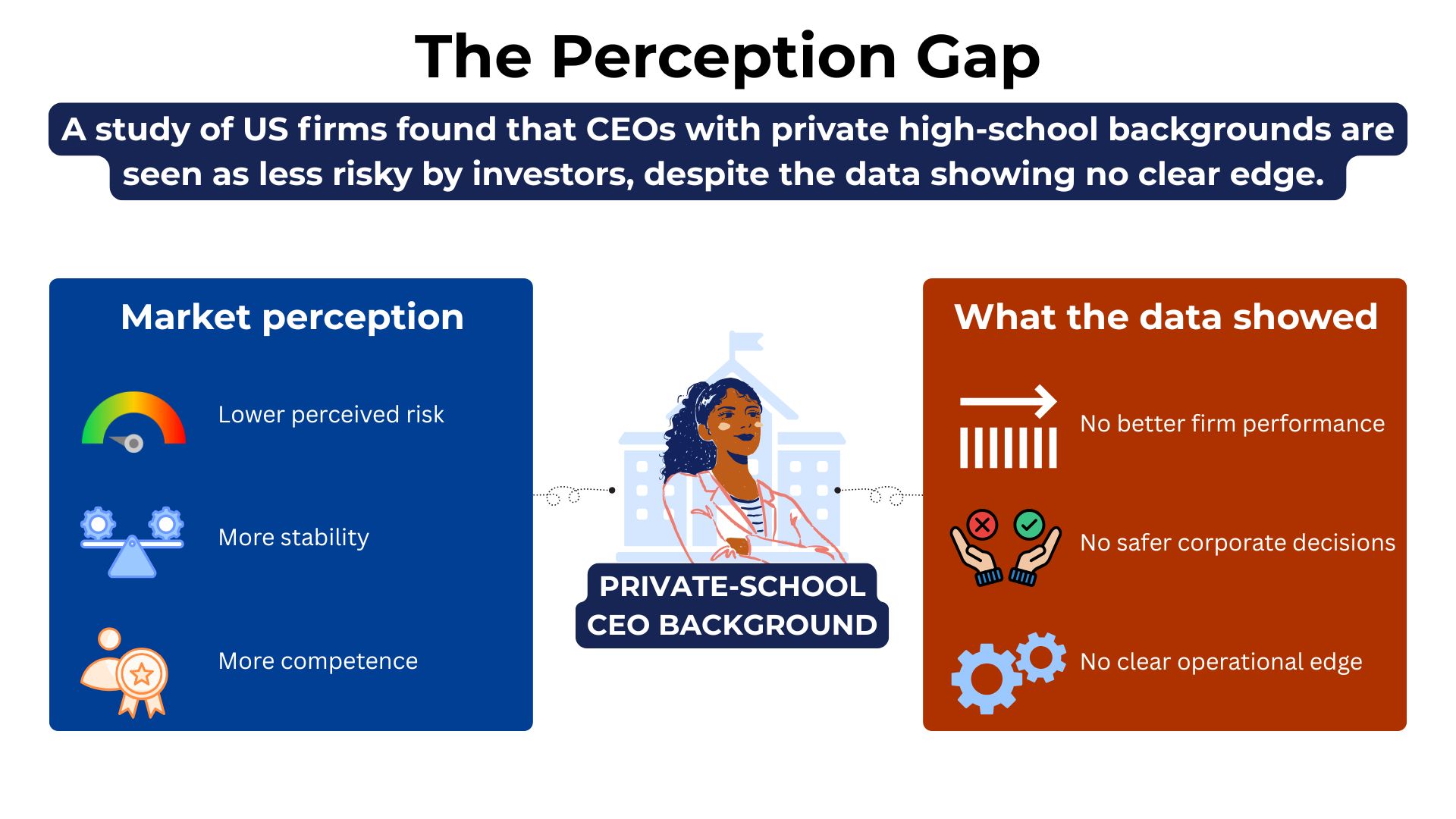

A new study, published in European Financial Management, has found that US firms led by CEOs who attended private high schools are treated as less risky by the market, even though the researchers found no clear evidence that those executives perform better, make safer decisions, or manage crises more effectively than their peers.

The study found that firms run by CEOs from private-school backgrounds had around 5% lower stock-market volatility on average.

However, the researchers argue this difference does not appear to be driven by how the companies are run. Instead, investors may be interpreting a CEO’s privileged background as a signal of competence and stability, particularly when there is uncertainty around the firm or its leadership.

How the research was conducted, in a nutshell

To conduct the study, the researchers analyzed CEOs of S&P 1500 non-financial and non-utility firms in the United States between 1992 and 2021. They manually collected reliable high-school information for 393 CEOs, classified each school as public or private, and then matched those records with stock-market volatility, accounting and CEO data from sources including ExecuComp and Compustat. After removing observations with missing data, the final sample included 2,157 firm-year observations, covering 272 CEOs from 226 firms.

The authors used private high-school attendance as a stand-in for childhood privilege. Their reasoning is that where someone goes to high school is usually shaped by their family’s money and background, whereas university can also reflect grades, scholarships, or achievements later in life.

The perception gap

The researchers found no meaningful evidence that CEOs from private-school backgrounds took fewer risks, used different incentives, produced stronger firm performance, or handled major shocks such as the 2008 financial crisis and the COVID-19 pandemic more effectively.

Rather, the study points to a perception gap. Investors may be giving executives from privileged backgrounds more benefit of the doubt, especially when there is less information available about the CEO or the company’s future direction.

That effect was found to be weaker when CEOs had been in the role longer, when companies had more analyst coverage, and when institutional ownership was higher. In other words, the private-school signal appeared to matter less when investors had more information to work with.

Dr Christos Mavrovitis, co-author of the study and Senior Lecturer in Finance and Accounting at the University of Surrey, said: “People like to think markets are purely rational, but our findings show that perception still plays a powerful role. A CEO’s background can shape how investors feel about a company, even when it has no real impact on how that company is run.”

All in all, the study suggests that markets may sometimes treat social background as useful information even when the underlying evidence does not support that assumption.

Reference:

Bi, Y., C. Mavrovitis, and C. Yang. 2025. “Rich Dad Poor Dad? CEO Private School Background and Firm Risk.” European Financial Management 0: 1–20. https://doi.org/10.1111/eufm.70043.