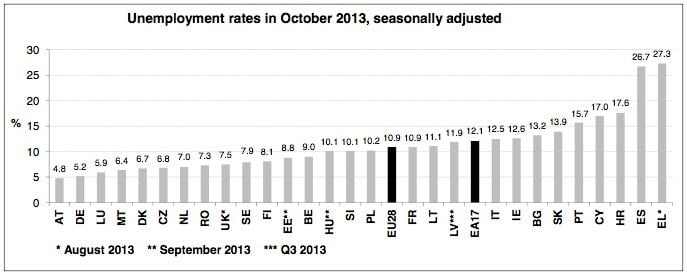

The Eurozone unemployment rate hit a 20-month low to 12.1 in October, compared to 12.2% in September, while annual inflation rose to 0.9% from 0.7% the month before, according to Eurostat.

Among young adults unemployment remains very high.

The Eurozone includes 17 countries that use the euro as their currency.

There were 19.298 million unemployed people in the Eurozone in October, 61,000 fewer than in September.

However, there were 615,000 more men and women unemployed in the region compared to October 2012.

Eurozone unemployment rate lopsided

Unemployment in the Eurozone is not uniform, its northern members enjoy much lower rates compared to their southern neighbors.

Highest and lowest unemployment rates:

- Austria – 4.8%%

- Germany – 5.2%

- Denmark – 6.7%

- The Netherlands – 7%

- Portugal – 15.7%

- Cyprus – 17%

- Spain – 26.7%

- Greece – 27.3%

Year-on-year unemployment rates rose in some and fell in other states

Compared to October 2012, unemployment rose in half the Eurozone countries and fell in the other half.

- Cyprus, rose to 17% from 13.2%

- Greece, increased from 25.5% to 27.3% (August 2012 to August 2013)

- The Netherlands, rose from 5.5% to 7%

- Latvia, fell from 14% to 11.9%

- Ireland, declined from 14.5% to 12.6%

- Lithuania, dropped from 13% to 11.1%

Unemployment in the USA in October was 7.3%, in the UK 7.5%, Canada 6.9%, Australia 5.8%, Japan 4%, and South Korea 3%.

Eurozone unemployment rate high among young people

There were 3.577 million young adults (aged under 25) unemployed in the euro area in October, i.e. 24.4%, higher than 23.7% among the whole of the European Union. In October 2012, youth unemployment stood at 23.3% in the whole of the EU and 23.7 in the Eurozone.

Below is a list of youth unemployment in some euro area countries:

- Germany – 7.8%

- Austria – 9.4%

- The Netherlands – 11.6%

- Croatia – 52.4%

- Spain – 57.4%

- Greece – 58%

The Eurozone is currently awash with diverging economic data, making it difficult for economists to forecasts the region’s short-, medium- and long-term prospects.

Earlier this week, the Economic Sentiment Indicator surprised analysts by rising 0.8 to 98.5 points; its highest reading in over two years.

On November 7th, the European Central Bank (ECB) cut its benchmark interest rates to 0.25% from 0.5%, the closest it has even been to zero. According to the ECB, the prospect of jobless economic growth and a near-deflationary environment warranted a cut in interest rates.

Was the euro doomed from the start?

The euro was initially introduced into the global financial markets as an accounting currency on the first day of 1999. On January 1st, 2002, euro banknotes and coins entered circulation. The Euro replaced the national currencies of 17 EU (European Union) nations. Some European very advanced economies, including the UK, Denmark and Sweden, chose to stay out.

UK politicians and the majority of its citizens felt that giving up the British pound sterling meant relinquishing too much sovereign control over national and economic matters.

Margaret Thatcher predicted in the 1990s that if the euro included countries from northern and southern Europe it would not work. She said that unless they had identical fiscal systems, cultures and laws, plus perfectly synchronized economies, just their diverging inflation rates would cause serious economic fissures in the failing and successful countries.

Today Germany has an enormous trade surplus and cannot appreciate its currency, while Spain, Greece and Portugal, among others, struggle desperately, wondering how to cope – none of them can devalue their currency, because they have relinquished that control.

Many economists in the UK and Scandinavia at the beginning of the millennium wondered how Eurozone countries would respond to economic crises without being able to devalue their currency.

Although most of those market analysts have generally kept quiet in 2013, partly for fear of causing further turmoil in an economically unpredictable and fragile region, there is a growing feeling within the Eurozone and outside that the euro was not set up properly.

As a Spaniard (who wished to remain anonymous) wrote in a letter to Market Business News, “How would Mexico cope today if it had been tied into the US dollar for the last ten years with double US inflation rates for the whole period without being able to devalue the peso?”

Alan Greenspan, former chairman of the US Federal Reserve, said earlier this week at a CNBC interview2 that the Eurozone is doomed to fail because the northern and southern European economies are too different.

Greenspan said:

“At the outset of the creation of the euro in 1999, it was expected that the southern eurozone economies would behave like those in the north; the Italians would behave like Germans. They didn’t. Instead, northern Europe fell into subsidizing southern Europe’s excess consumption, that is, its current account deficits.”

Greenspan predicts that as southern Europe’s fiscal crisis gets worse, the flow of goods from the north will dry up and southern Europe will get poorer.

Greenspan added “The effect of the divergent cultures in the Eurozone has been grossly underestimated. The only way to have several currencies from divergent nations lumped together is if they are culturally close, such as Germany, the Netherlands and Austria. If they aren’t, it simply can’t continue to work.”

There is a surprising similarity between what Greenspan is saying today and what Margaret Thatcher said over two decades ago.

In an interview with Forbes in 1991, Thatcher said:

“Every single fixed exchange rate has cracked in the end. We’re all at different levels of development of our economies. Some countries simply couldn’t live up to a single currency… We should each of us be proud to be separate countries cooperating together.”

(A fixed exchange rate is one that is pegged to a currency or basked of currencies.)

I believe the Eurozone has two stark choices, otherwise the whole euro dream will fail:

- Total political, legislative, and economic integration of all 17 Eurozone member states.

- Narrow the euro – allow the southern countries to regain their economic independence, i.e. help Spain get its peseta back, plus Greece’s drachma, Portugal’s escudo, and Italy’s lira. Put simply, help them leave the Euro and regain their economic independence.