Idiosyncratic risk, also known as unsystematic risk, is risk that is not correlated to overall market risk – it is the risk of price change caused by the unique circumstances of a particular security, or the risk that is sector-specific or firm-specific. Put simply is risk that affects just a specific company or sector, but not the whole market.

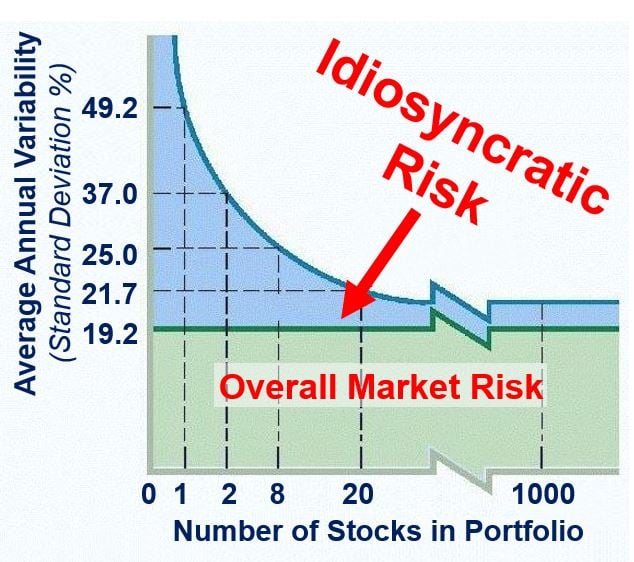

Idiosyncratic risk becomes a smaller proportion of an investment portfolio if you diversify. Diversification can get rid of idiosyncratic risk, but not systematic risk.

(Image: personal.psu.edu)

Idiosyncratic risk can be virtually eliminated from an investment portfolio through diversification – combining a variety of assets. Portfolio diversification is a risk-management strategy that includes a variety of assets to reduce the investment portfolio’s overall risk.

By pooling multiple securities the specific risks – idiosyncratic risks – cancel out.

Experts and researchers have found that idiosyncratic risk accounts for the major part of the variation of risk of an individual stock over time.

According to a Princeton University macroeconomic model including the financial sector, hedging idiosyncratic risk might be a self-defeating move because it leads to greater systemic risk, as it takes on more leverage. Princeton researchers found that while **securitization in principle does minimize the costs of idiosyncratic shocks, it ends up amplifying systemic risks in equilibrium.

** Securitization is a process of bundling up mortgages, auto loans and other types of debts into bond-like security instruments, which are sold to capital market investors.

Example of Unsystematic risk

Oil & Gas giant BP plc (British Petroleum) has historically moved mostly in tandem with the S&P500, which suggests that it has a high degree of systemic risk, i.e. it tends to move in the same direction as the overall market.

An unsystematic risk is a unique risk that stocks carry that does not affect the market as a whole. For example, the price of Microsoft shares is affected by the government’s antitrust lawsuit.

However, something happened in April 2010 that significantly affected BP’s share price, but not the overall market. An oil well in the Gulf of Mexico exploded.

On 20th April 2010, there was a tragic explosion in the Gulf of Mexico on the BP-operated Macondo Prospect. Following the massive explosion and the sinking of the Deepwater Horizon oil rig, a sea-floor oil gushed flowed for three months (87 days), until 15th July 2010, when it was capped.

BP’s stock price did nothing but fall during that period, while the overall market fluctuated normally. During that period, BP’s idiosyncratic risk had a major impact on its stock price.

As another example of risk, consider a mining exploration company that has a major part of its operations in a country where the risk of nationalization is high, i.e. there is a real possibility that country’s government might grab the mines for itself, with no guarantee that the company would be properly compensated.

If you are particularly keen on mining shares, you should consider diversifying your investment by buying shares in other mining companies that operate elsewhere in the world.

The Oil Disaster of 2010 in the Gulf of Mexico depressed BP share prices for several months, but the rest of the market continued normally – this is an example of an idiosyncratic risk.

Vasia Panousi and Dimitris Papanikolaou, of the US Federal Reserve System, made the following comment regarding investment, idiosyncratic risk and ownership:

“High-powered incentives may induce higher managerial effort, but they also expose managers to idiosyncratic risk. If managers are risk averse, they might underinvest when firm-specific uncertainty increases, leading to suboptimal investment decisions from the perspective of well-diversified shareholders.”

“…When idiosyncratic risk rises, firm investment falls, and more so when managers own a larger fraction of the firm. This negative effect of managerial risk aversion on investment is mitigated if executives are compensated with options rather than with shares or if institutional investors form a large part of the shareholder base.”

Video – Unsystematic Risk vs. Systematic Risk

This Education Unlocked video explains the difference between Systematic and Unsystematic Risk (, with clear and easy-to-understand illustrations.