An increasing-cost industry is an industry whose costs for production go up as more companies compete. When there are just a few players in that industry, the costs for production are low. However, when many newcomers enter the scene, demand for resources rises. In this industry, resources are limited, i.e., finite. Subsequently, the costs of these resources rise. This situation creates an increasing-cost industry.

Put simply; an increasing-cost industry is one that results from an increase in competitors. The greater number of competitors or producers pushes up the prices of the limited resources. Specifically, they push up the prices of the resources that companies need for production.

Energy generation is gradually transforming from an increasing-cost industry to a decreasing cost industry. Oil, gas, and coal are slowly making way for solar, wind, and tidal power.

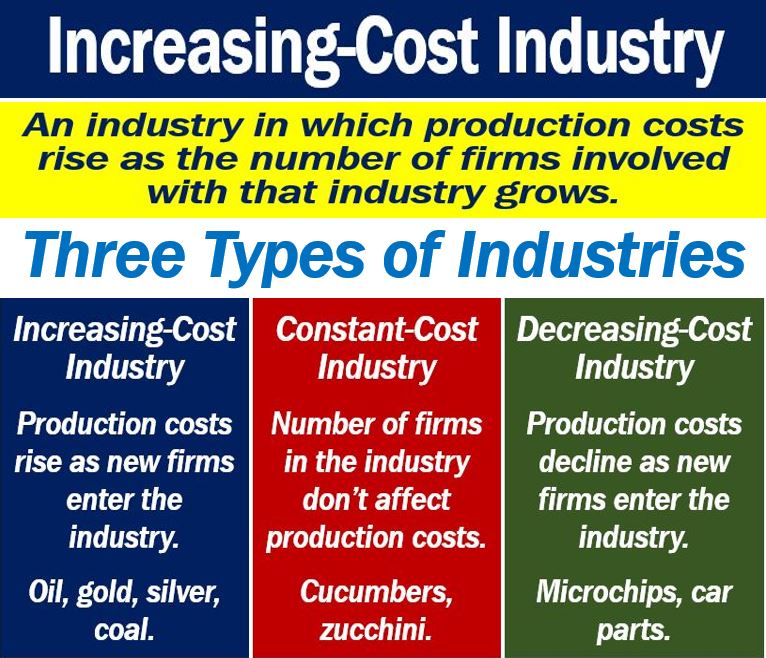

Increasing-cost industry

Any industry where supplies become scarce risks becoming an increasing-cost industry. If the number of firms in that industry rises, the cost of materials for production will rise. They will rise because more firms means greater demand. Greater demand, if supply remains constant, results in rising prices.

It is all to do with the law of supply and demand. In an economy where market forces dominate, a rise in demand results in an increase in price.

Any shortage of supplies leads to increases in prices of inputs.

Silver, oil, gold, and copper, for example, are increasing-cost industries. The supply of oil, gold, and silver is limited, i.e., they are finite resources.

The supply of materials for production in an increasing-cost industry is inelastic.

Inelastic supply refers to a market situation in which any change in the price of a product does not result in a corresponding change in its supply.

Types of industries

There are three types of industries:

Increasing-cost Industry

In an increasing-cost industry, costs for producers increase as new producers enter the industry.

In this type of industry, the supply of materials that companies use for production is limited.

Constant-cost industry

In a constant-cost Industry, the costs of materials for producers do not change if the total number of producers increases or declines.

Decreasing-cost Industry

In a decreasing-cost industry, production costs decline as more companies emerge within the industry.

Decreasing-cost industries tend to be those that depend on supplies that benefit from economies of scale. The materials that the producer requires for production are no finite, i.e., supply can match demand.

For example, economies of scale in the production of computer chips allow computer manufacturers to make more products at lower costs as the prices of chips decline. The supply of computer chips, unlike gold or oil, has no limit.

‘Economies of scale‘ refers to the overall unit costs of production – when production increases costs go down.