We live in a world that revolves around Money. We use it to buy or rent our homes, pay for tuition, travel, and communicate using our mobile phones. People also use it to buy a car, have fun, and for hundreds of different things. But, what is money exactly?

We use it as a means of paying for goods and services. It is, by definition, any object that we can store and has a unit of value. It is also something we use as a medium of exchange.

Cryptocurrency

The most modern type of money today is cryptocurrency. A cryptocurrency is a digital currency, i.e., it exists only electronically. Cryptocurrencies, such as ethereum and bitcoin have become extremely popular.

Whether their popularity continues over the long term is anybody’s guess. Currencies like bitcoin operate without any central banks.

Users are anonymous, which makes cryptocurrencies extremely popular with criminals.

Cryptocurrencies, by virtue of their digital nature, present unique opportunities for microtransactions and financial inclusivity, potentially transforming economic participation on a global scale.

Digital currencies also open avenues for decentralized finance, where financial systems operate without traditional intermediaries, thereby reshaping the landscape of international commerce.

Commodity money

In the past, people would use commodities that had a value in themselves.

Examples of commodity money that people have used as a means of making exchanges include:

- gold

- copper

- silver

- salt

- peppercorns

- precious stones

- alcohol

- and even cigarettes.

However, modern-day monetary systems are primarily based on fiat money. It does not have any intrinsic value, but governments declare it as legal tender. In other words, people can use it to pay ‘all debts, public, and private.’

The term stems from the Latin word ‘Fiat,’ which means ‘let it become,’ ‘let it be done,’ or ‘it shall be.’

The history of money

Bernard Lietar, a Belgian economist, civil engineer, author, and professor wrote the following in one of his books:

“Money, like certain other essential elements in civilization, is a far more ancient institution than we were taught to believe some few years ago.”

“Its origins are lost in the mists when the ice was melting, and may well stretch into the paradisiac intervals in human history of the inter-glacial periods, when the weather was delightful and the mind free to be fertile of new ideas – in the islands of the Hesperides or Atlantis or some Eden of Central Asia”

Many early cultures and societies used commodity money as a means of paying for goods.

The first known coin currency dates back to Mesopotamia (circa 3000 BC). At that time, people used shekels as a medium of exchange. The Sumerian bronze shekel represented one bushel of wheat in value.

-

Gold and silver coins

Historians believe that the Lydians first started using gold and silver coins as currency. They say that these coins first went into circulation more than two thousand years ago, i.e., 650-600 BC. The Lydians came from Lydia, which was in the modern western Turkish provinces of Izmir, Manisa, and Uşak.

Economies then started using systems of representative money. This began with banks or gold merchants issuing redeemable receipts. They issued the receipts to collect commodity money that people had deposited.

Eventually, people began accepting these receipts as currency that could be traded.

-

Banknotes

Banknotes were first used in China during the Song dynasty. At the time, people called paper money ‘jiaozi.’

The functions of money

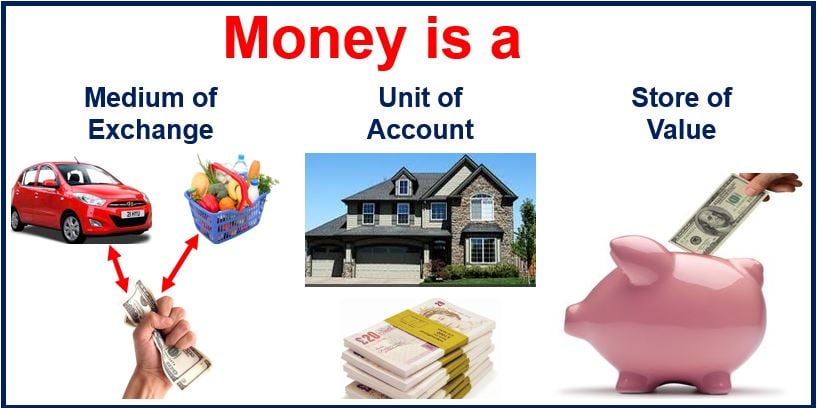

Money has three main functions:

- First, it is a medium of exchange.

- Second, it is a unit of account.

- And third, it acts as a store of value.

Every element of society uses money as a medium of making exchanges. For example, producers sell their goods to wholesalers (in exchange for money). Subsequently, wholesalers go on to sell their goods to consumers.

Put simply; money facilitates exchanges in the economy.

It also acts a unit of account. In other words, we use it to measure the value of various goods and services in an economy. It essentially serves as a standard of value.

Before money existed (when bartering was the main means in which people traded), it was difficult to store a surplus of value. Today, however, people can store surplus purchasing power and use it at any time.

If money did not exist

If money did not exist, the world as we know it would be completely different. We would all be living in a barter economy.

Every time any of us wanted to buy something, we would have to exchange it for something else. Specifically, we would have to find something that the seller would want.

For example, what if I specialized in fixing cars and wanted to purchase food? I would have to find a farmer who had a broken down car. I could then offer to fix the car in exchange for food.

What would I do if I could not find any farmer with a broken down car? What would I do if I found a farmer who just sold eggs, and I was looking for vegetables.

It is likely that millions of people would starve to death. Humans cannot survive for weeks or months without food while they try to find the right person with whom to trade.

As we continue to evolve into an increasingly digital and interconnected global economy, the role of money, whether physical or digital, remains fundamental in shaping both our everyday transactions and broader economic policies.

Words that mean “money”

There are many words in the English language that mean “money,” (or whose meanings are similar). Let’s have a look at some of them and how they can be used in a sentence:

-

Currency

Has the same meaning as money. It refers to the type of money used in a country.

Example: “When traveling abroad, you need to exchange your currency for the local tender.”

-

Cash

Refers to money in the form of physical notes and coins, as opposed to credit.

Example: “I prefer to pay with cash for small daily purchases.”

-

Funds

Refers to a reserve of money set aside for a particular purpose or available for spending. Example: “We have enough funds to cover the costs of the project.”

-

Capital

Often refers to money that is used to invest or start a business, implying a larger sum than just cash-in-hand.

Example: “They raised the capital needed to start their new company.”

-

Finances

Generally refers to money matters or management of money, but can also be used to denote the money itself.

Example: “She managed her finances well, ensuring she had savings for the future.”

-

Banknotes

Has the same meaning as money, specifically referring to paper money.

Example: “He had a wallet full of banknotes from various countries.”

-

Coinage

Refers to metallic forms of money.

Example: “The ancient coinage was discovered in the shipwreck.”

-

Liquidity

Refers to the ease with which an asset, or security, can be converted into ready money without affecting its market price. The term is often used in a broader financial context than just money but can imply ‘ready to use cash.’

Example: “The company’s strong liquidity position meant it could capitalize on new investment opportunities quickly.”

Famous quotes about money:

- Benjamin Franklin:

“Money has never made man happy, nor will it, there is nothing in its nature to produce happiness. The more of it one has the more one wants.” - Nelson Mandela:

“Money won’t create success, the freedom to make it will.” - George Bernard Shaw:

“Lack of money is the root of all evil.” - John Maynard Keynes:

“The importance of money flows from it being a link between the present and the future.” - Margaret Thatcher:

“Pennies do not come from heaven. They have to be earned here on earth.” - Woody Allen:

“Money is better than poverty, if only for financial reasons.” - Barack Obama:

“Money is not the only answer, but it makes a difference.” - Voltaire:

“When it is a question of money, everybody is of the same religion.”