Lloyds Banking Group, the UK’s largest retail bank, announced that it is accelerating cost cutting plans amid an economic slowdown following last month’s Brexit vote.

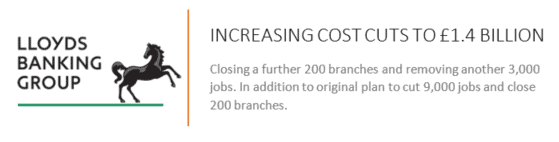

The bank said in a statement that it will be axing a further 3,000 jobs and closing an additional 200 branches by the end of 2017 in a bid to save an extra £400 million by the end of next year.

The cuts and closures announced on Thursday are in addition to the cost-cutting plan the bank announced two years ago, which includes 9,000 job cuts and 200 branch closures as part of an effort to save £1 billion by the end of 2017.

“Following the EU referendum the outlook for the UK economy is uncertain and, while the precise impact is dependent upon a number of factors including EU negotiations and political and economic events, a deceleration of growth seems likely,” said António Horta-Osório, Group Chief Executive.

“The UK enters this slowdown from a position of strength due to the sustainable nature of the economic recovery in recent years, where the UK has been growing at about 2pc with reducing levels of debt.”

The additional cost-cutting measures should help offset lower-for-longer interest rates following the UK’s vote to leave the EU.

The branch closures also reflect a shift in consumer behaviour, with branch transactions declining by 10% a year, according to Lloyds.

Ian Gordon, an analyst at Investec, told Rueters. “Lloyds remains a no growth bank. Its revenue outlook is flattish, hence its costs need to fall faster.”

Impressive half-year profits

Lloyds reported better-than-expected first-half pretax profit of £2.45 billion, more than double the amount in the same period last year.

Underlying profits fell to £4.2bn from £4.4bn last year, but managed to beat analyst expectations of £4 billion.

Income was just below the last year’s figure, at £8.9 billion, mainly due to a rise in bad debts and a decline in “other income”.