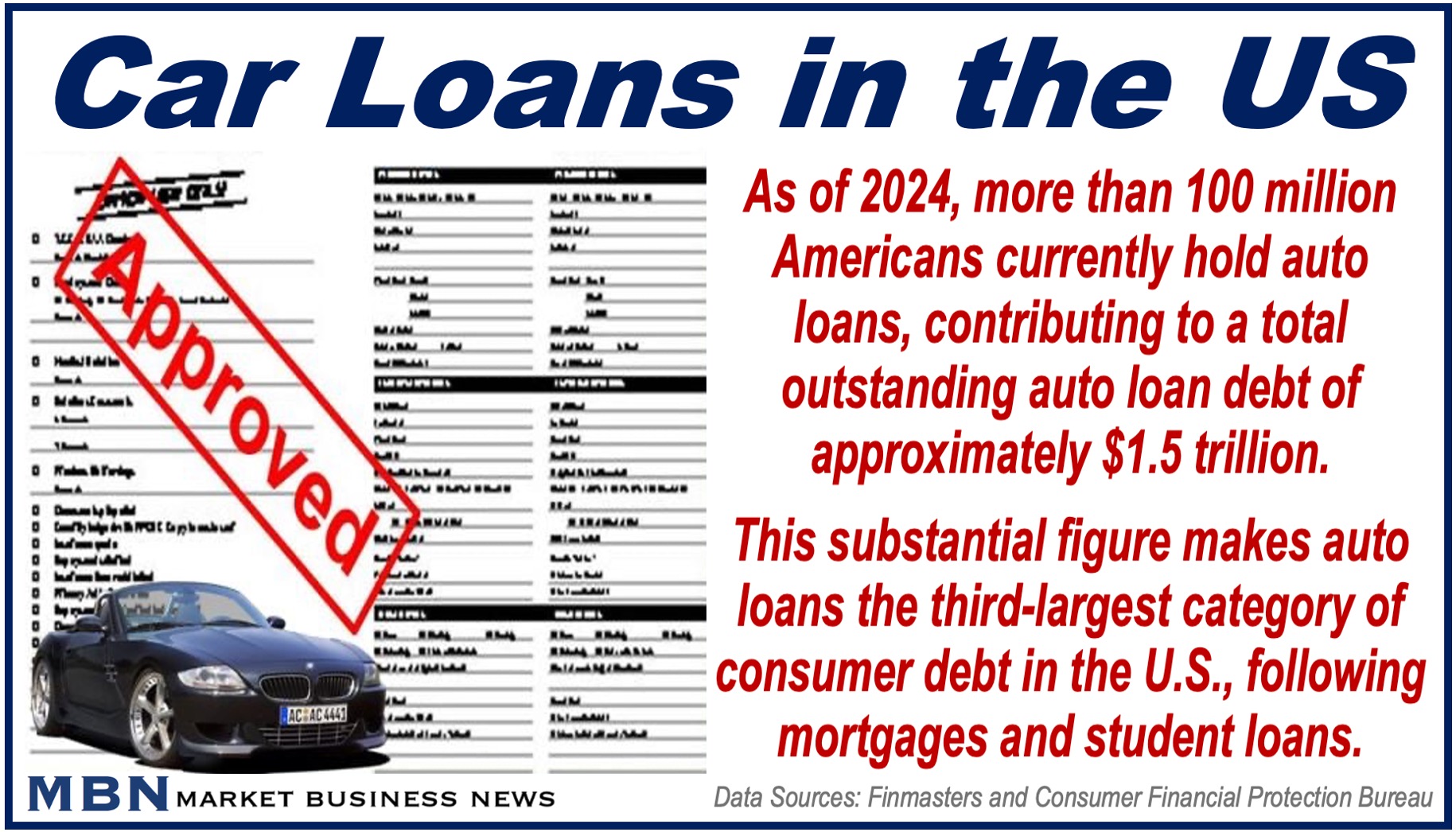

What is an Auto Loan? Definition and Examples

Whenever we purchase a new or second-hand car, most of us do so on credit, that is, we take out an Auto Loan or Car Loan.

Auto loans break up the cost of a vehicle into manageable monthly installments, allowing us to pay back over time.

If you’re considering an auto loan, it’s essential to understand how these loans work and what factors influence their terms and costs.

What Is an Auto Loan or Car Loan?

An auto loan is a type of financing used to purchase a vehicle. It is classified as a secured loan, meaning that the car serves as *collateral.

* Collateral is a possession (asset) that a borrower offers as security on a loan.

If you, the borrower, default on the loan, the lender has the right to repossess the vehicle to recover their loss.

Because of this security, auto loans typically come with lower interest rates compared to unsecured loans, such as personal loans.

Experian, one of the world’s ‘big-three’ credit reporting agencies (along with Equifax and TransUnion), says the following about auto loans:

“An auto loan is a form of credit that you can use to buy a car or another type of vehicle. When you buy a car with an auto loan, the lender pays the auto seller the full amount once the loan is issued. Then, you make monthly payments to the lender for a set period of time.”

Types of Lenders

There are many types of auto finance lenders, including banks, credit unions, online lenders, and dealerships.

Once you get approval for a loan, the lender pays the seller the full purchase price of the vehicle. In return, you make monthly payments to the lender over a specified period, including interest on the loan.

The lender holds onto the car’s title (ownership documents) as collateral until the loan is fully repaid.

Several factors influence how an auto loan works and what it costs. Understanding these key terms will help you make informed decisions when shopping for a loan.

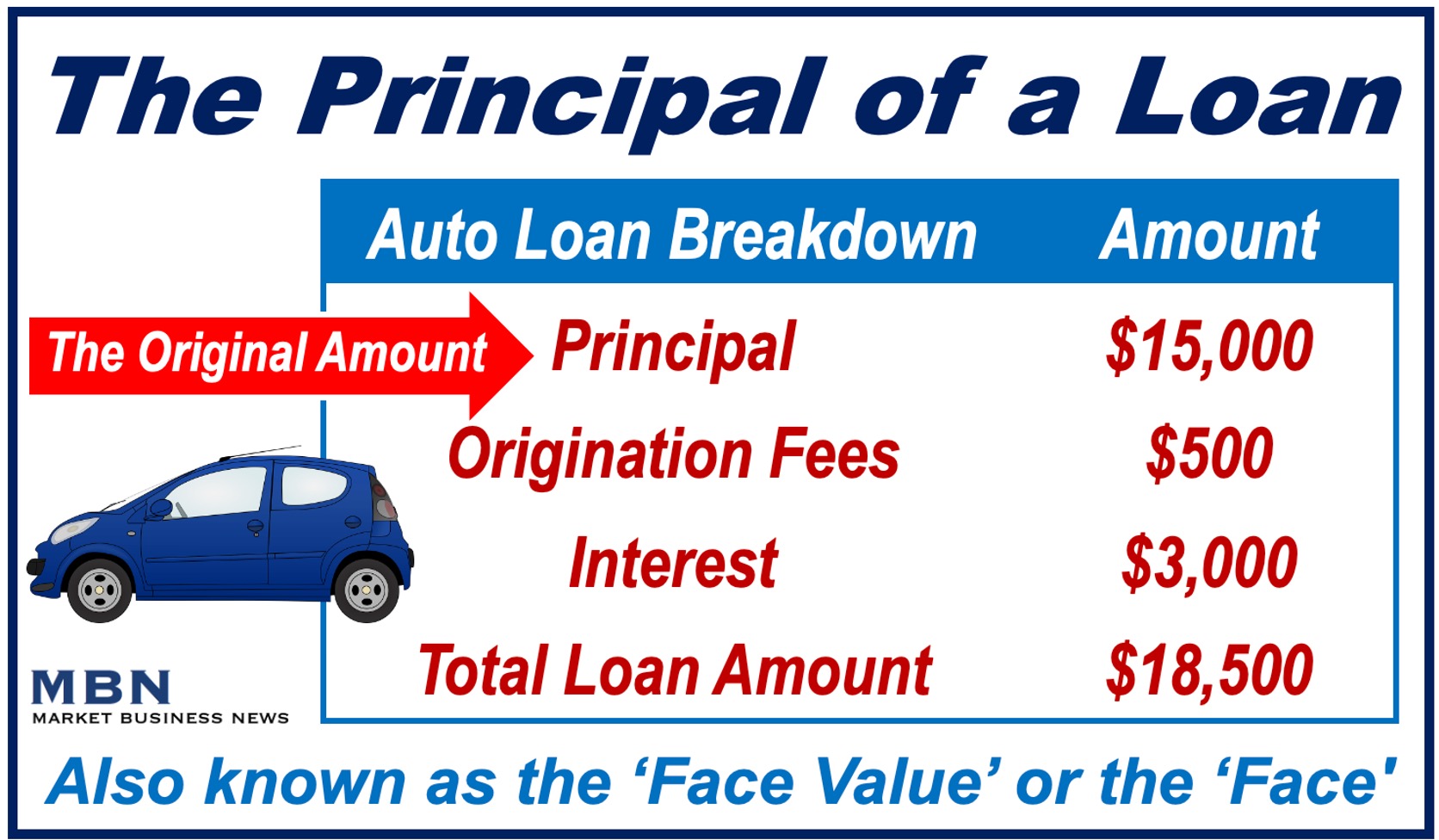

The principal, also known as the ‘face value’ or ‘face,’ is the amount of money you borrow from the lender, before interest, fees, and other charges are added. It represents the vehicle’s purchase price minus any down payment or trade-in credit you apply toward the purchase.

The size of your principal will directly impact your monthly payments and the total interest you pay over the life of the loan.

The interest rate is the cost of borrowing money, usually expressed as an annual percentage of the principal.

It can either be fixed or variable. Fixed interest rates remain the same throughout the life of the loan, while variable rates may change depending on market conditions. The higher your interest rate, the more you’ll pay in total loan costs.

Interest rates are influenced by several factors, including your credit score, the loan term, the type of vehicle you’re purchasing, and broader economic conditions. Key influences include the central bank’s interest rate (or prime rate), inflation, and the lender’s internal cost of borrowing.

Economic policy and market fluctuations can also impact the rates lenders offer. Generally, borrowers with better credit scores qualify for lower interest rates.

The APR is a more comprehensive measure of the cost of borrowing. It includes the interest rate plus any additional fees charged by the lender, such as origination fees or processing fees.

The APR gives you a clearer picture of the total cost of the loan and is essential to consider when comparing loan offers.

-

Loan Term

The loan term is the length of time you have to repay the loan, typically ranging from 24 to 84 months.

Shorter loan terms often come with higher monthly payments but lower overall interest costs.

Longer loan terms, on the other hand, result in lower monthly payments but increase the total interest paid over the life of the loan.

If you buy a $20,000 car by giving the seller $8,000 of your own money and borrowing $12,000, your down payment is $8,000.

A down payment is the initial amount you pay upfront when purchasing a vehicle. A larger down payment reduces the loan amount and may help you qualify for better loan terms, including a lower interest rate.

Many lenders require a down payment, but some offer no-down-payment loans, which often come with higher interest rates.

How Auto Loans Work

If you are thinking of taking out an auto loan, you may find this step-by-step breakdown of the process useful:

-

Application

You will need to apply with a lender. They will assess your credit score, income, and debt-to-income ratio to determine your eligibility and the terms of the loan.

-

Loan Approval

Once you’re approved for a loan, the lender will provide you with the funds to buy the vehicle.

You may get pre-approved for a loan before you start shopping, which can help you negotiate better with the dealership.

-

Monthly Payments

After the loan is approved and the vehicle is purchased, you’ll begin making monthly payments (installments).

These payments will include both the principal and interest. Over time, the principal decreases, and a larger portion of your payment goes toward paying off the loan balance rather than interest.

-

Ownership

While you’re making payments, the lender holds a lien on the vehicle, meaning they have legal ownership until the loan is paid off.

Once you’ve made all the required payments, the lender releases the lien, and the car title is transferred to you.

Types of Auto Loans

Auto loans come in various forms, depending on the type of vehicle you’re purchasing and your financial situation. Some common types of auto loans include:

-

New Car Loans

These are designed for purchasing brand-new vehicles. They often come with lower interest rates because new cars have a higher resale value and are considered less risky for lenders.

-

Used Car Loans

Since used cars have already depreciated and may require more maintenance than new vehicles, loans for them typically come with higher interest rates.

-

Refinancing Loans

If you already have an auto loan, refinancing allows you to replace your current loan with a new one, potentially with a lower interest rate or better terms.

-

Lease Buyout Loans

If you’re leasing a vehicle and decide you want to own it at the end of the lease term, a lease buyout loan helps you finance the remaining balance and transition from leasing to owning.

Factors Affecting Auto Loan Rates

Several factors influence the interest rate and terms you’re offered on an auto loan. Understanding these factors can help you secure the best possible deal.

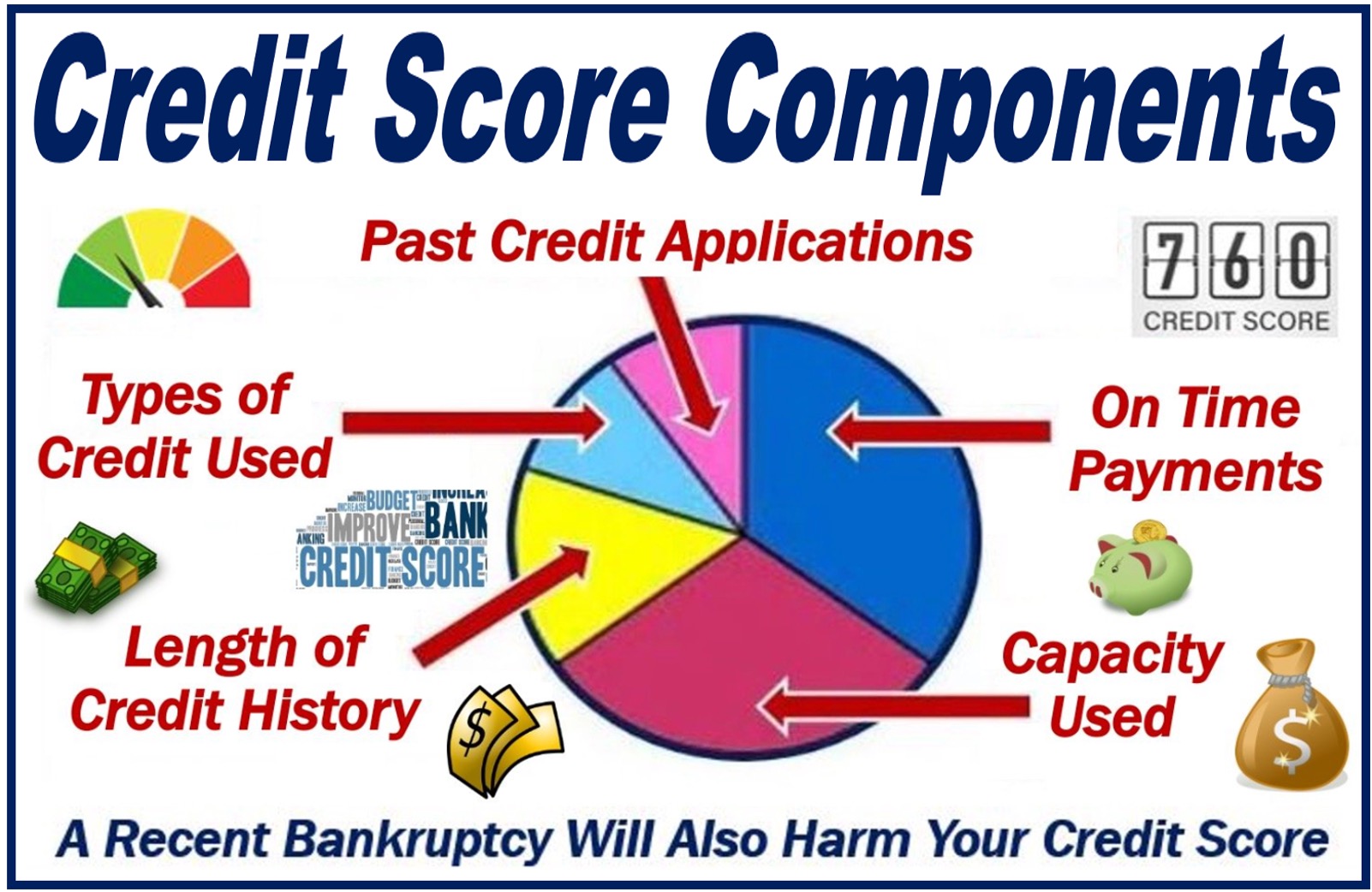

Your credit score is one of the most critical factors in determining the interest rate on your loan.

Borrowers with higher credit scores are considered less risky and are more likely to receive favorable terms.

If you have a lower credit score, you may still qualify for a loan, but with higher interest rates.

This interesting quote, from the University of Wisconsin-Madison in the US, explains what the difference between ‘credit score’ and ‘credit report’ is:

“Many people use the terms ‘credit report’ and ‘credit score’ interchangeably, but they are not the same.”

“Your credit report is a detailed account of your credit history, while your credit score is a three-digit number signifying your credit-worthiness. You are entitled to three free credit reports per year, but you generally have to pay to view your score.”

-

Loan Term

The length of the loan term also affects your interest rate. As mentioned earlier, shorter loan terms typically have lower interest rates, while longer terms may come with higher rates.

You need to weigh the benefits of lower monthly payments against the total cost of the loan over time.

-

Vehicle Type

New cars generally come with lower interest rates compared to used cars because of their higher value and lower risk of depreciation.

However, new vehicles also tend to cost more, which could result in larger loan amounts and higher monthly payments.

Advantages of Auto Loans

-

Immediate Access to a Vehicle

They allow you to buy a car without needing the full purchase price upfront.

-

Flexible Terms

You can choose a loan term that fits your budget, whether you prefer lower monthly payments or paying it all off more quickly.

-

Potential to Build Credit

Making timely payments on your auto loan can improve your credit score over time.

Disadvantages of Auto Loans

-

Interest Costs

Even with a low-interest rate, you’ll pay more for the vehicle over time compared to buying it outright.

-

Depreciation

Cars lose value quickly, and you may owe more on the loan than the vehicle is worth, known as negative equity.

-

Risk of Repossession

If you fail to make payments, the lender can repossess your car, leaving you without transportation and damaging your credit.

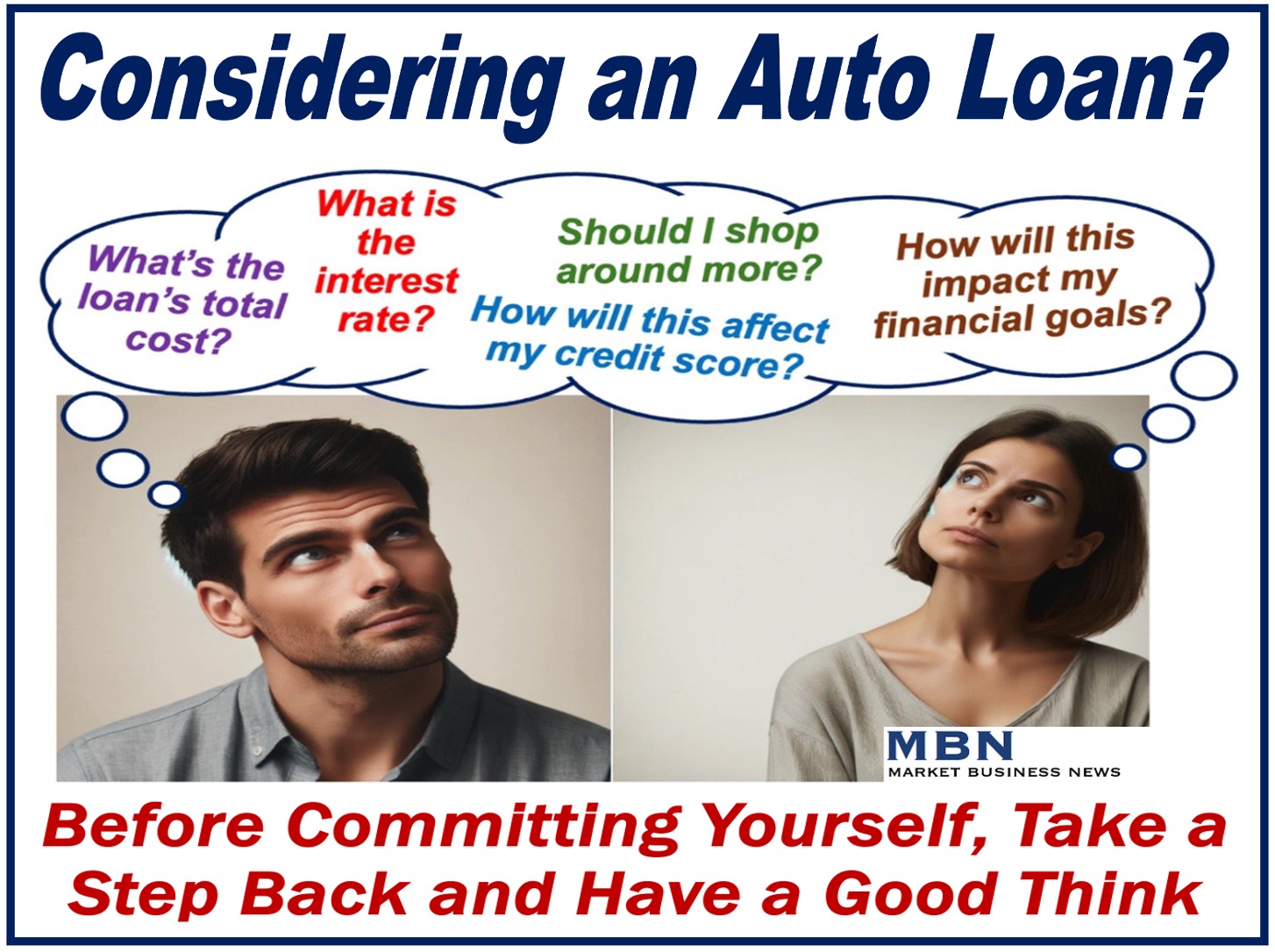

Important Questions to Ask Yourself

Before committing to a loan, consider giving yourself time for reflection. Ask yourself these questions:

- Should I shop around to see whether there are better deals?

- Have I considered all other financing options, such as borrowing from a family member or digging into my savings?

- Am I satisfied with the interest rate?

- What are the loan fees, admin costs, and other hidden costs?

- What is the total cost of the loan, including interest, over the entire loan term?

- Do I really need a new car now? Could I keep my current vehicle for another year?

- How will this decision impact my financial goals?

- Can I afford the monthly payments?

- What happens if my financial or employment situation changes?

- Can I repay the loan early without being penalized?

Auto Loan Calculator

Final Thoughts

An auto loan can make buying a vehicle more affordable by breaking up the cost into manageable payments.

However, it’s essential to understand the terms of the loan, including interest rates, repayment periods, and the total cost.

By shopping around and comparing offers from different lenders, you can find an auto loan that fits your budget and financial situation.