The OECD (Organization for Economic Co-operation and Development) projects global growth falling from 3.4% in 2025 to 2.8% in 2026, and then recovering to 3.1% in 2027.

The conflict involving Iran and the blocking of the Strait of Hormuz, through which 20% of the world’s oil supply is transported, have shaken global energy markets. Most economists have become increasingly pessimistic about global economic growth prospects.

US GDP is forecast to fall from 2% in 2026 to 1.8% in 2027, while the European Union (EU) is expected to remain at 0.8% this year and then climb to 1.2% in 2027.

China’s economy is projected to grow by 4.5% in 2026 and slow down slightly to 4.3% in 2027. Germany, whose economy has been struggling, is forecast to grow by 0.7% in 2026 and 1.1% in 2027.

The OECD has two projected scenarios: 1. A time-limited scenario, in which the economic environment returns to pre-conflict levels in 2026. 2. A prolonged disruption scenario, in which the economy doesn’t return to pre-conflict levels until late 2027. The figures quoted above refer to the OECD’s ‘time-limited scenario.’

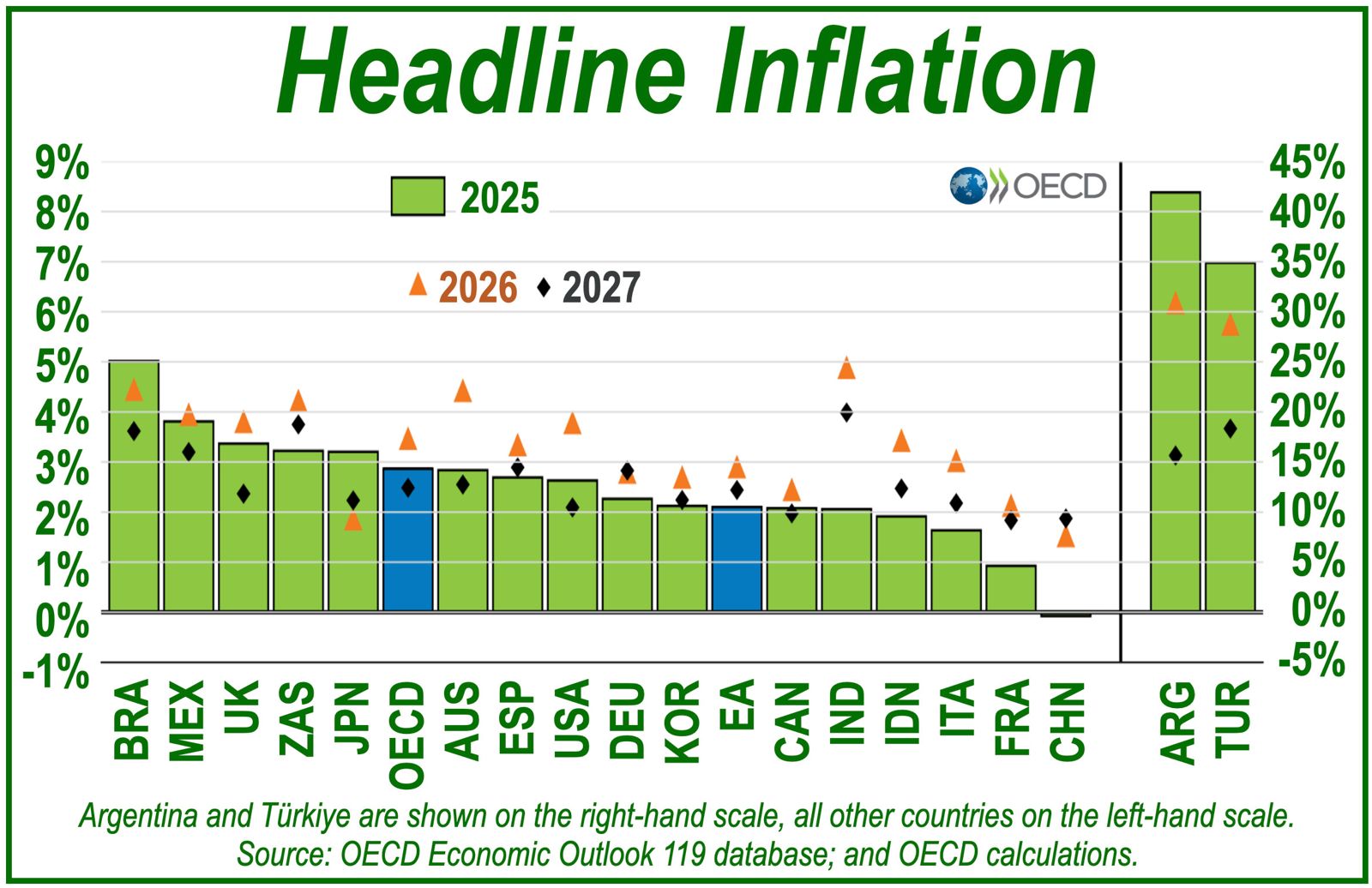

Inflation

In both emerging and advanced economies, inflationary pressures have risen significantly since the Iran conflict began. The increase in the price of energy has led to higher commodity prices. Other goods which are indirectly affected by petroleum prices, such as food and some agricultural products, have also become more expensive.

According to an OECD press release, the G20 economies are collectively expecting inflation to rise to 4% this year compared to 3.4% in 2025. The US Federal Reserve (Fed), the Bank of England, the European Central Bank, and most other central banks have an annual inflation rate target of 2%. As inflation is currently averaging double that amount, economists, lawmakers, business leaders, and other stakeholders are increasingly discussing the possibility of further interest rate hikes.

The OECD says the following about central banks:

“Throughout this uncertain period, central banks must remain vigilant, but the supply-driven rise in prices need not trigger a policy response, as long as inflation expectations remain well anchored.”

“However, a monetary policy response may become necessary if broader price pressures intensify, or if growth weakens significantly.”

The OECD’s time-limited scenario forecast predicts G20 inflation will ease to 3.1% in 2027 as energy and grocery price pressures subside. However, in the prolonged disruption scenario, inflation will increase significantly more and stay high for much longer.